Although Nevada is recognized for having fewer business regulations than other states, practically every private firm is still required to have workers’ compensation insurance.

Beyond the government requirements, workers’ comp insurance is a policy that will help your business avoid many issues. It is also an excellent way to show your employees that you care about them.

Even though the policy is vital for business, it can be confusing, especially if you are looking for the best insurance companies. This article will help you understand the best workers comp insurance providers in Nevada to help you make an informed decision. We also have information regarding the policy for you.

- The 6 best workers comp insurance companies in Nevada

- Nevada workers’ compensation insurance laws

- Nevada workers’ compensation insurance requirements

- Who is exempt from workers comp insurance in Nevada?

- What does workers’ compensation insurance cover in Nevada?

- How much does workers’ compensation insurance cost in Nevada?

- Factors impacting workers comp insurance costs in Nevada

- How to reduce the cost of your workers’ comp Insurance?

The 6 best workers comp insurance companies in Nevada

Hundreds of insurance companies offer workers comp insurance in Nevada. Here are the top 6 providers that we recommend for their different pros and cons.

- CoverWallet: Best for comparing several insurance quotes online

- Simply Business: Best for small businesses to find low-cost coverage

- biBERK: Best for low-cost coverage from a reputable insurer

- THREE: Best for a simple and comprehensive policy

- The Hartford: Best for comprehensive coverage

- InsurePro: Best for flexible plans

CoverWallet: Best for comparing several insurance quotes online

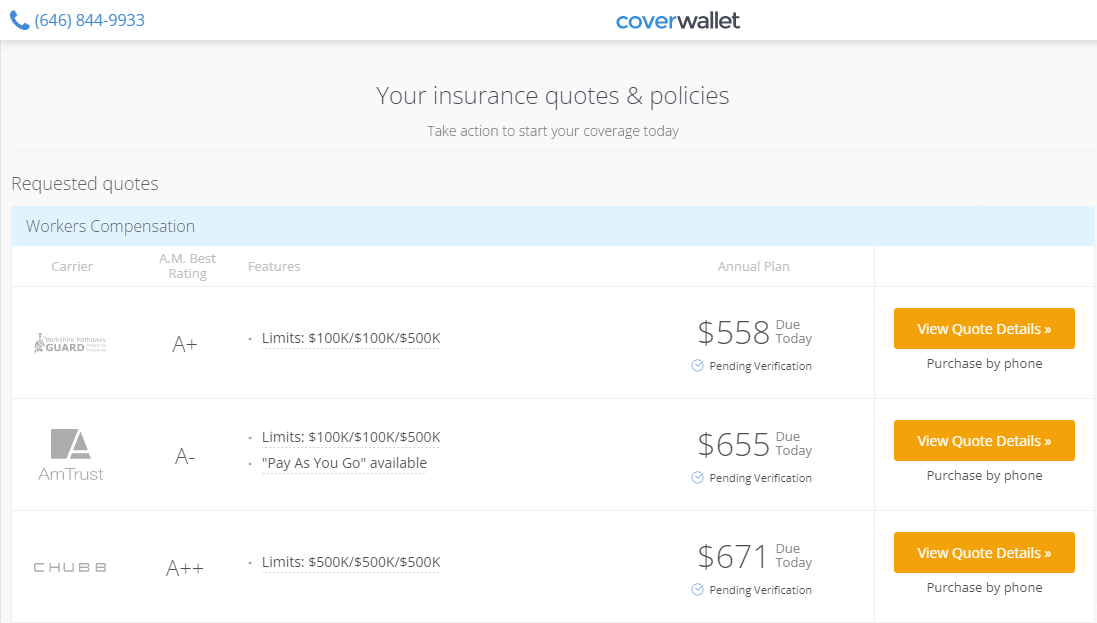

CoverWallet is a digital insurance broker for businesses. It is an online platform that allows you to compare prices for workers’ comp and other insurance policies with ease. After completing a single form, they will present you with many quotations from various prestigious insurance providers with whom they have partnered. Form completion takes around 10 minutes.

These sample quotes were generated from CoverWallet for an IT consulting business. The hypothetical company has two full-time employees, $400 000 annual revenue, and an annual payroll of $250,000.

Pros

- Get multiple quotes in minutes

- Quotes are tailored to meet your requirements

- Can help you find low rates

Cons

- Quotes are limited to their partners only

- Sometimes quotes may not be available online. They have to call you to discuss your quote options

Simply Business: Best for small businesses to find low-cost coverage

Simply Business is a marketplace for insurance policies. The company does not sell policies; instead, it helps companies find policies from leading insurance companies. It is the ideal choice for contractors and professionals that want inexpensive business insurance. In less than 10 minutes, you may also get recommendations on coverage alternatives and free quotations from the company’s insurance partners whether you require workers’ compensation or general liability coverage.

Pros

- Tailored policies to meet your needs

- Quotes available online in 10 minutes

- Generates quotes from over 20 top insurers in the US

Cons

- The number of their partners limits their quotes suggestions

- Quotes are sometimes not available online

biBERK: Best for low-cost coverage from a reputable insurer

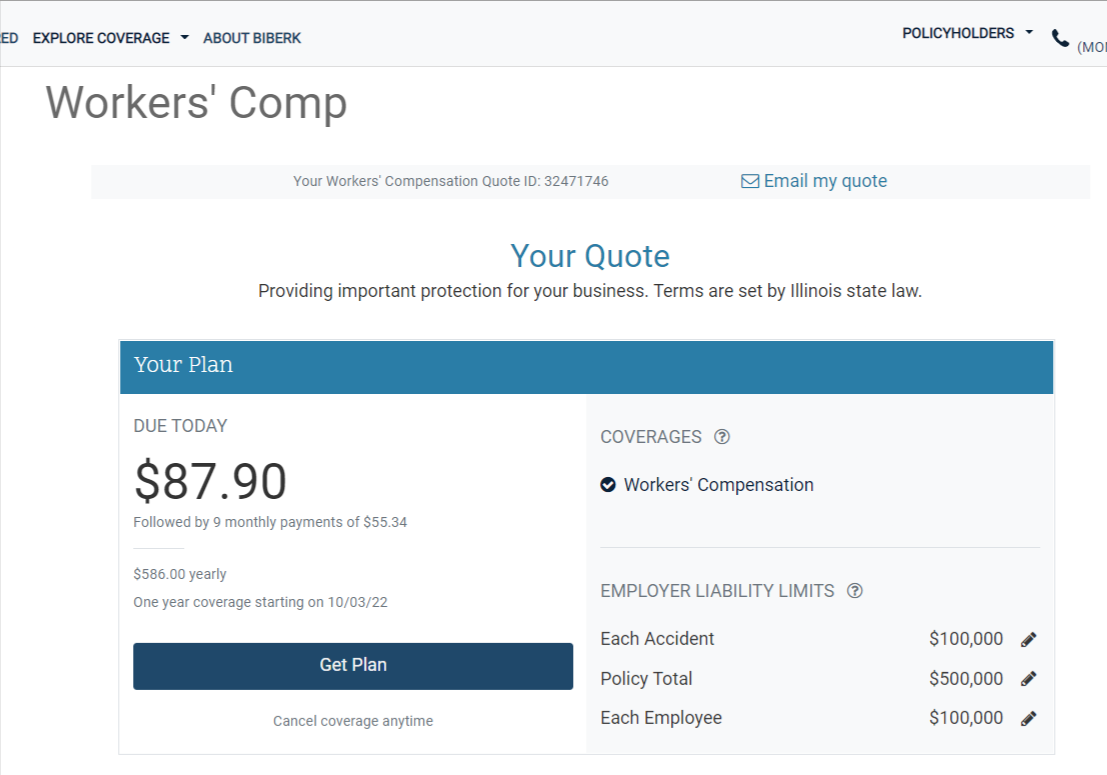

The parent business of biBERK is Berkshire Hathaway, one of the most well-known brands in the insurance industry. However, biBERK is mainly focused on small enterprises. The organization does not depend on outside insurance brokers to locate the appropriate workers’ compensation benefits for you. Instead, biBERK is a direct insurer, which often means you may get a quotation quickly and without extra fees.

The following is an example of the quote you get from biBerk. This quote is for a hypothetical IT consulting business with two full-time employees, $400 000 annual revenue, and a yearly payroll of $250,000.

Pros

- Scalable workers’ comp insurance plans

- Industry-leading experts

- Safety training available for staff

- Quotes are generated entirely online

Cons

- No special discounts

- Not being able to compare quotes with other companies easily

THREE: Best for a simple and comprehensive policy

Three is one of the business insurance brands owned by Berkshire Hathaway. THREE is a new insurance company that aims to simplify insurance for small businesses. THREE offers all the coverage that most small companies need in one comprehensive policy. Their policies are easier to understand because they only contain three pages.

Pros

- Easy-to-understand policies

- One policy covers most issues

- Online quote generation

- In-house insurance experts that can help you with issues

Cons

- The quotes process requires you to answer too many questions.

The Hartford: Best for comprehensive coverage

The Hartford stands out as of the oldest and finest insurers in the US. When you buy a plan from the company, your employees can access specialized case managers and pharmacy networks. This will assist them in receiving the treatment they need when they require it the most.

In addition, the Hartford has a calculator that you can use on the website to assess the typical price of workers’ compensation. In terms of market share, this service provider is also the second-largest workers’ compensation insurance provider.

Pros

- Pay-as-you-go pricing available

- Standard coverages are more extensive than those of the majority of rivals.

- Strong track record and business standing

- You may get discounts

Cons

- Some business owners have to buy policies offline

- If you need additional coverages, THREE may not offer it

InsurePro: Best for flexible plans

InsurePro is an insurance broker that allows you to submit your information and get quick quotations for your workers’ comp. The company works with numerous workers’ compensation insurance providers, allowing them to search for the lowest pricing and coverage for your company.

The following image shows an example of the quotes you get from Insurepro. This quote is for a hypothetical IT consulting business with two full-time employees, $400 000 annual revenue, and a yearly payroll of $250,000.

Pros

- You get quotes in 20 minutes

- Access to low rates

- You can get quotes for just when you work

- Obtain quotes from over 20 companies online

- Online chat support responds in less than 10 minutes

Cons

- You have to speak with an agent to buy policies

- You have to file claims with the insurance companies

Nevada workers’ compensation insurance laws

Workers’ compensation in Nevada is defined as a “no-fault” insurance policy that benefits employees who are injured or get ill on the job. In addition, workers’ compensation protects companies that offer their employees coverage in case of an accident or sickness.

Typically, “no-fault” systems provide coverage to the wounded or ill employee regardless of who triggered the event that resulted in the injury or sickness. Typically, this includes any non-intentional injuries and illnesses sustained on the job.

“No fault” systems are advantageous for both the employee and the company. That is because they give financial rewards for the employee’s rehabilitation and safeguard the firm if the injured employee chooses to launch a lawsuit related to their condition.

Nevada workers’ compensation insurance requirements

Employers with at least one worker in Nevada must have workers’ compensation insurance. The laws of the State of Nevada make it compulsory that all companies carry the policy.

Companies that default risk paying fines of up to $15,000 and premium penalties if caught. In extreme cases, the company might be shut down, held responsible for all injury expenses, and face criminal charges.

Who is exempt from workers’ compensation insurance in Nevada

The state of Nevada allows a few exemptions from workers’ compensation, including the following:

- Temporary employees who have workers’ compensation insurance from another state and are brought into Nevada

- Employment that lasts no more than 20 days and has a total labor cost of less than $500.

- The Nevada workers comp legislature does not govern employment in interstate commerce.

What does workers’ compensation insurance cover in Nevada?

In Nevada, workers’ compensation insurance may assist pay for essential medical care for a work-related sickness or accident. It may also reimburse a Nevada employee’s lost income if they need recovery time.

Workers’ compensation in Nevada may cover:

- Accident expenses if an employee is harmed on the job

- Lost wages if an employee takes time off for a work-related accident or sickness

- Ongoing care expenses if your employee needs additional medical treatment, such as physical therapy, after a work-related accident or sickness.

- Work-related illnesses induced by allergy or toxic chemical exposure

- Disability compensation if your employee becomes fully incapacitated due to a work-related accident or illness

- Funeral expenses if an employee dies in the line of duty

The following are some examples of scenarios where workers’ compensation insurance may cover your Nevada firm and its employees in the following situations:

- A construction worker fractures their leg after falling over a ladder

- A restaurant chef suffers a burn while cooking by mistake.

- An employee dies after being exposed to hazardous substances at work.

- An employee is hurt when a beam falls in your plant and injures them.

- An employee is involved in an accident while traveling to meet clients for your company.

How much does workers’ compensation insurance cost in Nevada?

The average cost of workers comp insurance in Nevada is $0.94 per $100 payroll. Most companies in Nevada with less than $300,000 in payroll spend an average of $70 per month on workers’ compensation insurance.

The cost of workers’ compensation insurance in Nevada varies based on the kind of small company and the degree of employee exposure to risk. We are discussing the details below.

This is the average only. Your rates will be different. Be sure to get several quotes or work with a broker like Simply Business or CoverWallet to compare several quotes to choose the cheapest one for you.

Learn more at how much does workers comp insurance cost

Factors impacting workers comp insurance costs in Nevada

The workers comp insurance cost in Nevada varies significantly depending on several factors as follows:

Employee count and payroll

The larger your workforce, the greater the expense of workers’ compensation insurance. Your company’s payroll is included in the premium calculation for workers’ compensation insurance. Your costs are computed per $100 of payroll—consequently, the more your payroll, the greater your expenses.

Work performed by employees

Greater risk jobs result in higher workers’ compensation expenditures. An accountant, for example, stands a lesser risk of harm than a carpenter and will pay less. Work that poses a greater risk of accidents, sickness, or death on the job may incur higher premiums.

Workers’ compensation class codes

The National Council on Compensation Insurance (NCCI) maintains class codes for workers’ compensation. The NCCI determines class codes based on the occupations performed by employees and assists insurers in calculating worker’s compensation premiums. A more significant high-risk class code employee may increase workers’ compensation costs.

Record of workers’ compensation claims

The more workers’ comp claims you have had in the past, the more likely your insurer will increase your premium.

How to reduce the cost of your workers’ comp Insurance?

You can do the following things to make your workers’ comp insurance more affordable.

Make safety a priority

When determining premiums, many insurance companies include how seriously firms take the safety of their employees into the equation. If you make the mitigation of risks a priority, this may work to your advantage.

Implement safety training for your staff

You may be able to bring down the cost of your insurance premiums if you provide training opportunities for your employees and formulate safety guidelines.

Bundle policies

Some insurers will offer discounts when you buy multiple policies at once. Therefore, you may consider buying your worker’s comp policy along with other policies like commercial auto. Some insurers offer this policy together with some other essential policies in a business owner’s policy. It might be helpful to ask your insurer if they have such possibilities.

Check with multiple insurers

If you feel a policy is too expensive, it might actually be. Some insurers will offer you better protection at lower prices, and the best way to know is to check. So, before you buy a policy, ensure you have done proper research and are buying the best policy at the best price.

Learn more at the cheapest workers comp insurance companies

What is not included in workers’ compensation insurance?

There are specific conditions that workers’ compensation does not cover, even though it covers many injuries sustained on the job.

- Intentional or self-inflicted injuries;

- Instances that the insurance company has reason to suspect fraud

- Injuries sustained by employees outside of work

- Client accidents

- Accidents that happened while the wounded employee was under the influence of alcohol

Beyond the above list, insurers have the right to exclude some other risks as they wish. Therefore, when making a purchase, it is usually a good idea to check what your insurance policy will and will not cover, as this may help you avoid any unpleasant surprises.