Illinois law requires that all firms with employees have workers’ compensation insurance, with a few exceptions. This coverage covers workers who are injured on the job with medical benefits.

While the laws are clear for most companies in Illinois, Workers’ comp insurance for Contractors can be difficult to understand sometimes. Therefore, we are here to guide you through choosing the correct coverage from the right carrier.

This guide will show you all you need to know about Illinois worker’s compensation insurance.

- 6 best workers comp insurance companies for contractors in Illinois

- What does workers comp insurance cover in Illinois?

- Workers comp insurance requirements for contractors in Illinois

- Who is considered as an independent contractors in Illinois?

- Workers comp insurance cost for contractors in Illinois

- What factors affect the cost of workers’ comp insurance for contractors in Illinois?

- How to reduce worker’s compensation insurance costs for Illinois contractors?

6 best workers comp insurance companies for contractors in Illinois

- CoverWallet: Best for comparing quotes online

- Pie: Best for an excellent digital experience

- Employers: Best for contractors with unstable payroll

- Chubb: Best for assistance program

- The Hartford: Best for mobile contractors

- Thimble: Best for gig economy contractors

CoverWallet: Best for comparing quotes online

CoverWallet is a leading digital broker specializing in small business insurance. They work with many leading insurance companies. They have invested in their technology platform to automate much of the insurance buying process. Their online application takes less than 10 minutes for any business to complete.

Thanks to their advanced technology platform, it is super easy to buy small business insurance with CoverWallet. After you complete their quote application, they are able to pull several quotes from their partners to present to you in one single simple screen for you to compare and select the best one for you.

The following picture shows a sample quote generated from the website for an HVAC contractor based in Chicago, Illinois.

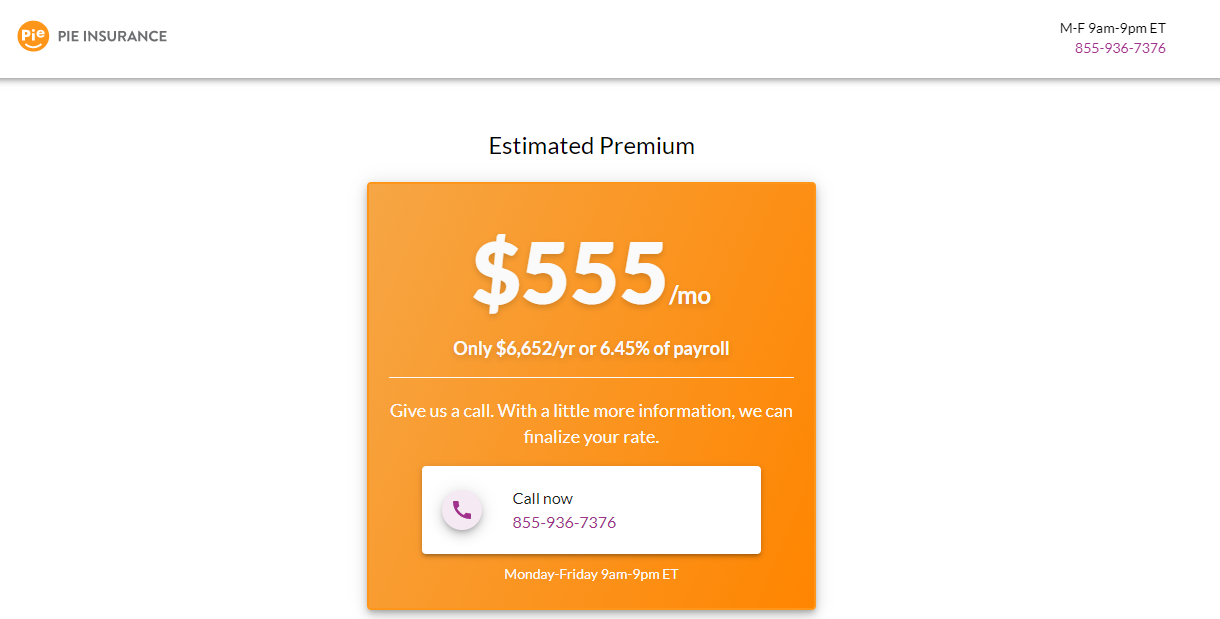

Pie: Best for an excellent digital experience

Pie is a relatively new insurance company trying to help small business owners find the right coverage options. Due to size and limited resources, small businesses require affordable workers’ comp. Pie solves these problems as the company claims that they help their clients save up to 30% on workers’ comp insurance.

The application process for their worker’s comp insurance is done entirely online. The process is easy and takes about 3 minutes. Being a new company, it’s interesting to note that Pie has an excellent rating on Trust Pilot.

The following is a sample quote generated on Pie’s website for an HVAC contractor in Chicago.

Employers: Best for contractors with unstable payroll

Unstable payroll can be a common problem for contractors since they may have to hire subcontractors to do their job sometimes. Employers is one insurance company that helps contractors with this peculiar issue properly manage their workers’ comp costs through their pay-as-you-go insurance plans.

The small business insurance firm specializes in making workers’ compensation plans reasonable and simple to get for contractors. Plus, they provide workers’ compensation insurance in 46 states and the District of Columbia, where commercial insurers can sell workers’ compensation.

The only problem with Employers insurance is that they do not generate quotes online. To get a quote, you have to fill out an online form, after which they will pair you with one of their agents around you.

Chubb: Best for assistance programs

Chubb is a significant national insurer that provides personal and business insurance. The organization provides a great return-to-work support program, assisting small business owners in managing medical and disability benefits for their injured employees returning to work. The program helps contractors track and manage the absence of their employees.

Chubb can issue policies for almost any business size, but it is recognized for treating all accounts the same for customer care and claims.

The company used to have a small business insurance webpage with online quotations. However, that option is currently unavailable. At the moment, you can only obtain quotes through their agents.

The Hartford: Best for mobile contractors

One of the problems of being an independent contractor is that you might have to travel often to meet your clients. Suppose you are a contractor that moves your workers around. Whether it is outside of Illinois or you travel internationally, the Hartford might be the ideal choice for your workers’ compensation insurance.

The Hartford is the leading small business insurance provider who has been around for 200+ years and have insured more than 1 million small businesses and continue to grow. They are proud to be one of the most ethical insurance companies and have built their stellar reputation around being ethical in their business operations.

With their significant presence across the country and abroad, you know that you are in good hands when you are insured by them. Whenever your business takes you, you can rest assured that the Hartford is there when you need them.

Thimble: Best for gig economy contractors

Contractors in the gig economy usually have issues finding the right insurance company. Some insurers do not know how to categorize these companies correctly, so they avoid them outrightly, while others might give them outrageous bills.

Thimble solves this problem for gig economy workers and microbusiness owners. With Thimble, people in this category can buy workers’ compensation policies even if they have only one part-time employee, and the coverage can start immediately. You can even combine workers’ compensation insurance with professional or general liability coverage if you want.

Quotes are generated online through the website in most cases. However, if the artificial intelligence on the website cannot decide based on the information you provide, you may have to speak with their representative on the phone.

What does workers’ comp insurance cover in Illinois?

Workers’ compensation insurance supports company owners by providing coverage up to your policy maximum for medical expenditures incurred from job-related injuries or diseases on employees.

Usually, the policy may cover specific incidents, including:

- Any physical ailment induced by employment such as asbestosis, skin disease, work-related stress, etc.

- Injuries due to repetitive usage of a body part, e.g., focal hand dystonia, carpal tunnel syndrome, etc.

- Work-related stroke or heart attack

- Work-related aggravation of pre-existing medical problems

In Illinois, workers’ compensation income payments are only paid when an employee cannot work for more than three days due to a work-related illness or injury.

After the insurer grants the claim, payments are given based on the Illinois Department of Employment Security’s statewide average weekly salary. The payments are commonly classified into three categories depending on the specifics of the situation:

Total temporary disability

Total temporary disability is when an employee cannot work for an extended length of time due to a job-related accident or sickness. For example, if an employee who regularly performs manual labor injures his back and cannot work for three weeks.

Such employees would be considered suffering from total temporary disability until they are back to their feet. If you or one of your workers as an independent contractor has a temporary complete disability, you may be eligible for a weekly benefit of up to $1,500 in Illinois.

Partially permanent disability

Partial permeant disability occurs when a job-related injury prevents an employee from completing their obligations at the same level as before the injury.

For example, if you own a landscaping and cleaning company, one of your employees has a muscle injury in their forearm that never heals. That individual may never be able to trim overhead vegetation again, but they may be able to perform other gardening tasks.

Employees with a permanent partial disability get the maximum weekly payout of up to $670 in Illinois.

Permanent complete incapacity

Permanent complete disability is when a work-related injury or disease makes the employee unable to work due to loss or severe damage to some body parts. Permanent complete disability benefits offer a disabled employee with weekly salary compensation for 25 years or up to $500,000, whichever is larger.

Death and funeral benefits

Suppose a covered employee dies due to an on-the-job accident or injury. In that case, their spouse or children will get the same weekly income compensation as employees with permanent complete disability.

Workers’ compensation insurance requirements for contractors in Illinois

While the laws are straightforward for most industries, independent contractors might have to deal with some twists. Generally speaking, independent contractors are not required to have workers’ compensation insurance.

However, there is usually confusion about who an independent contractor is because the state determines whether a person is a regular employee or an independent contractor.

Under Illinois Workers’ Compensation legislation, the criteria for determining whether an injured worker is an employee or an independent contractor differ from other standards for making this conclusion.

So, even if you earn a 1099 income and even if you signed an independent contractor agreement, you can still be deemed an employee under the Illinois Workers’ Compensation Act.

If you own a trucking firm, you need to be more cautious. A recent Illinois Supreme Court case determined that referring to a trucker as an independent contractor in a contract does not relieve the trucking company’s need to provide work comp for drivers.

Who is an independent contractor in Illinois?

To understand if you must have workers comp insurance, you need to understand who an independent contractor is. That way, you will know exactly where you belong.

Independent contractors are self-employed individuals or freelancers contracted by other firms to undertake certain work without being hired as employees. For better understanding, the IRS defines independent contractors this way (paraphrased):

An individual is considered an independent contractor if the payer has the power to control or influence only the outcome of the job, rather than what will be done and how they will do it.

Generally speaking, a person will be classified as an independent contractor if:

- They can only be fired if contract criteria are not met.

- They can work for different clients using a 1099 tax form.

- They set their schedule and hours independently.

- They may recruit additional contractors and subcontractors

- They perform services as they deem fit to accomplish the job;

- They provide their equipment, tools, materials, etc., for the job.

Learn more at the best workers comp insurance companies for independent contractors

Workers’ compensation insurance cost for contractors in Illinois

Work comp expenditures in Illinois are among the highest in the country, while improvements implemented in 2011 have been credited with lowering costs. According to the Illinois Workers’ Compensation Commission, allocated risk pool premiums can cost up to 50% more than open market rates.

The estimated employer rate for workers’ compensation is between $0.8 and $1.0 for every $100 covered payroll in Illinois. So, if you have a payroll of $100,000 as a contractor, you might pay between $800 and $1,000 annually for workers’ comp insurance.

To know your exact workers comp insurance cost, be sure to shop around with a few companies or work with a digital broker like CoverWallet or Policy Sweet or commercialinsurance.net to compare several quotes to find the cheapest one for you.

Learn more about the workers comp insurance cost and how to calculate them

What factors affect the cost of workers’ comp insurance for contractors in Illinois?

Your industry, payroll, and claims history are all important variables influencing workers’ compensation premiums. Your state’s worker compensation legislation will also influence your worker’s compensation premium.

Industry

Certain industries, such as construction, are more prone to claims and hence have higher premiums. NCCI maintains over 700 workers’ compensation class codes. These codes represent the amount of risk associated with each job type and determine how much you will pay for workers’ compensation insurance.

Payroll

The yearly payroll of a company is used to assess the cost of workers’ compensation insurance. As a result, while looking for workers’ compensation insurance, you’ll need to know your yearly payroll data.

Claims history

When setting the workers’ comp rate for your company, both the number of claims and the nature of the claims will be taken into account. If your company has had workers’ compensation claims in the past, your workers’ compensation expenses will rise.

How to reduce worker’s compensation insurance costs for Illinois contractors?

Workers’ compensation is an essential component of every independent contractor’s insurance package. Here are some suggestions for saving money on it.

Compare several quotes before buying

Similar to other types of insurance, comparison shopping is imperative to find the cheapest policy for your business. Different insurance companies will give you different quotes since they evaluate risks differently and have different pricing strategies. Be sure to shop around with a few companies or work with a broker like CoverWallet or Policy Sweet to compare several quotes before making your final decision. If you buy the first quote you receive, it is likely that you are leaving some money on the table.

Employee education

Teaching your staff how to do simple job activities might reduce accidents and injuries. For example, you may want to teach your personnel to be able to recognize and report dangers.

Regulations for safety

Educating your staff on workplace safety can help reduce slips, falls, and other mishaps. Spend some time going through safety guidelines with staff.

Maintenance of property

Providing a safe and healthy environment for your employees may help decrease accidents, injuries, and diseases. You should perform building inspections regularly, and the building’s air ducts should be kept clean. Check that the building’s upkeep is up to date.

Use of appropriate equipment.

Providing employees with the most recent personal protective equipment they require will keep them safe on the job. This will show your commitment to safety and may help you secure a discount.

Learn more at the cheapest workers comp insurance companies