Have you heard of E&O insurance? It’s also known by the term errors and omissions or professional liability or sometimes malpractice insurance. If you are running a technology consulting or an IT consulting business, or if you are an independent IT consultant, you’re wondering if you need E&O insurance, or you would just like a little more information, please continue reading.

We’ve compiled a guide to help you better understand E&O insurance and to discuss the five best tech E&O insurance companies.

- 5 best tech E&O insurance companies

- What does tech E&O insurance cover?

- Who needs E&O insurance?

- How much does tech E&O insurance cost?

- How can you save on your tech E&O insurance?

5 best tech E&O insurance companies

We researched E&O insurance companies and narrowed the offerings down to the five companies we thought were the best choices. Those five are:

- CoverWallet: Best for comparing several quotes online

- Simply Business: Best for finding low-cost coverage

- Hiscox: Best if you prefer a more established carrier

- Thimble: Best for part-time tech consultants who only need coverage for a short-term

- NEXT: Best for affordable bundled policy: general liability and E&O coverage

For each of the five companies, we reached out for a quote for E&O insurance for a small IT consulting firm based in Los Angeles, California. The quotes and an overview of each company are in the following section.

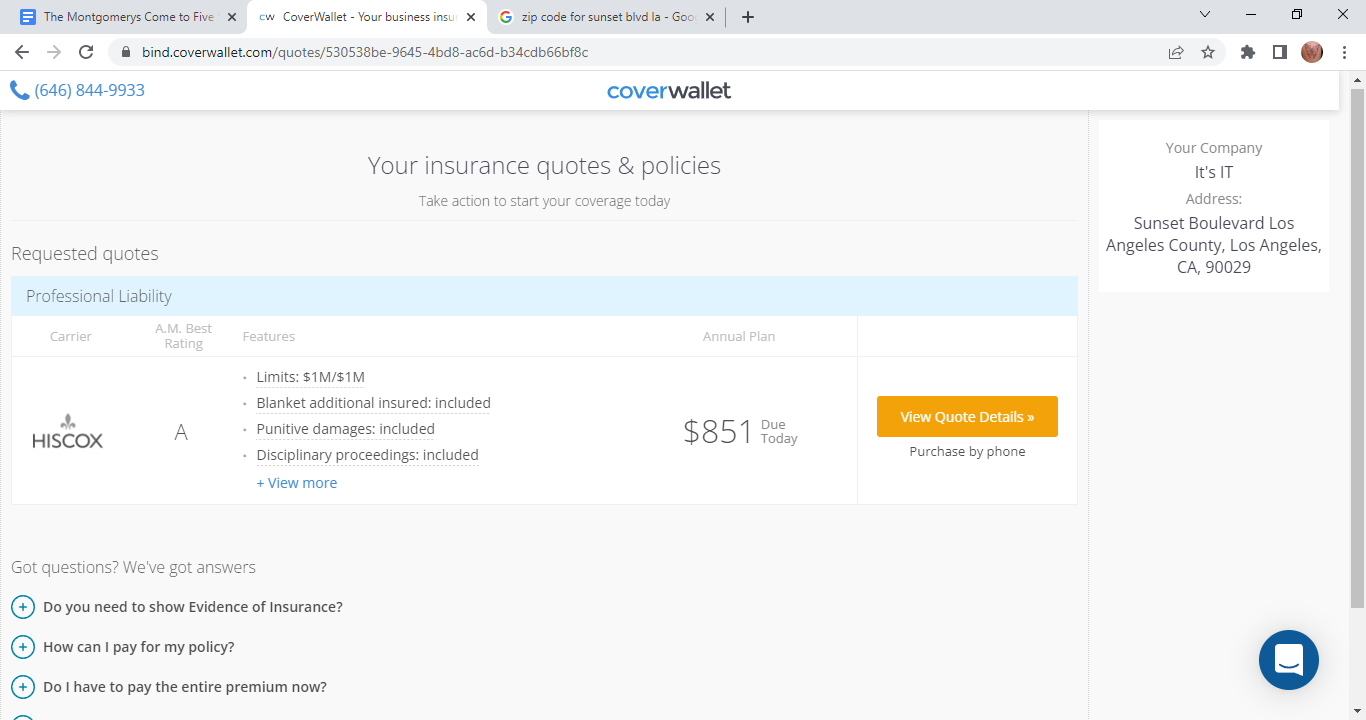

CoverWallet: Best for comparing several quotes online

CoverWallet is an online insurance broker specializing in business insurance. It takes approximately ten minutes to complete the questionnaire provided to request coverage. CoverWallet will process your data and return up to three quotes based on your provided information. CoverWallet doesn’t offer insurance for you, but the company does locate multiple quotes to help you compare costs.

If you choose to purchase coverage through CoverWallet, their online tools are available for you to pay premiums, download certificates of insurance, or file claims. They offer these tools to business owners who purchase coverage elsewhere for an annual fee.

Pros

- Use one application to get several quotes.

- Offer a wide variety of coverages.

- Manage your policies through their online dashboard.

Cons

- All coverage is provided through a third party.

- You sometimes have to call to complete the process.

Simply Business: Best for finding low-cost coverage

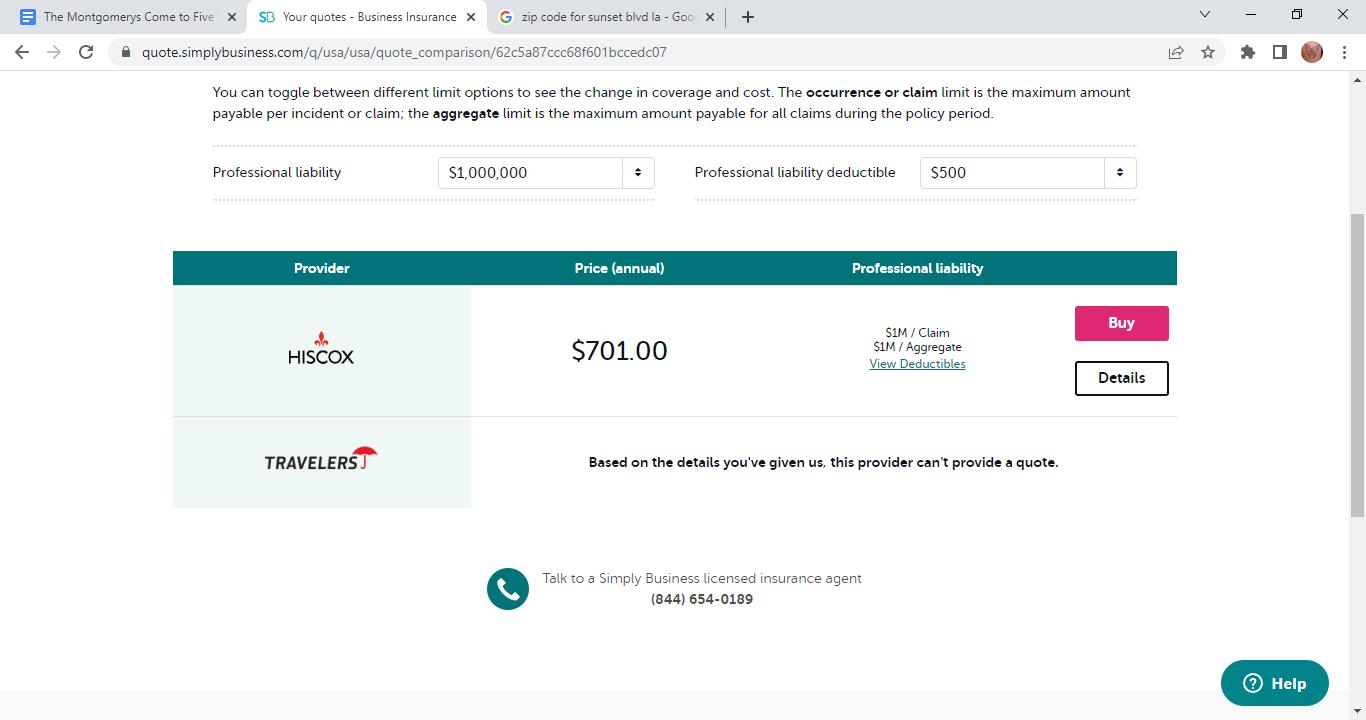

Simply Business is an insurance broker providing small business owners with quotes for coverage from their partner companies. Travelers own them, so you will almost certainly get a response from Travelers regarding coverage. Simply Business does the legwork to find the quotes, but that is where their services end. Third-party insurers handle everything else policy related.

Simply Business focuses on making it simple to buy a small business insurance policy and finding low-cost coverage for its customers. They partner with several insurance companies, which enables them to find the lowest cost for their customers.

Pros

- Use one website to get quotes from multiple providers

- Easy to find low-cost coverage and simple to buy a policy

- Operate a resource library that helps you understand the business coverages you need

Cons

- All insurance policies are handled through third-party companies.

- Cannot file a claim with Simply Business.

Hiscox: Best if you prefer an established carrier

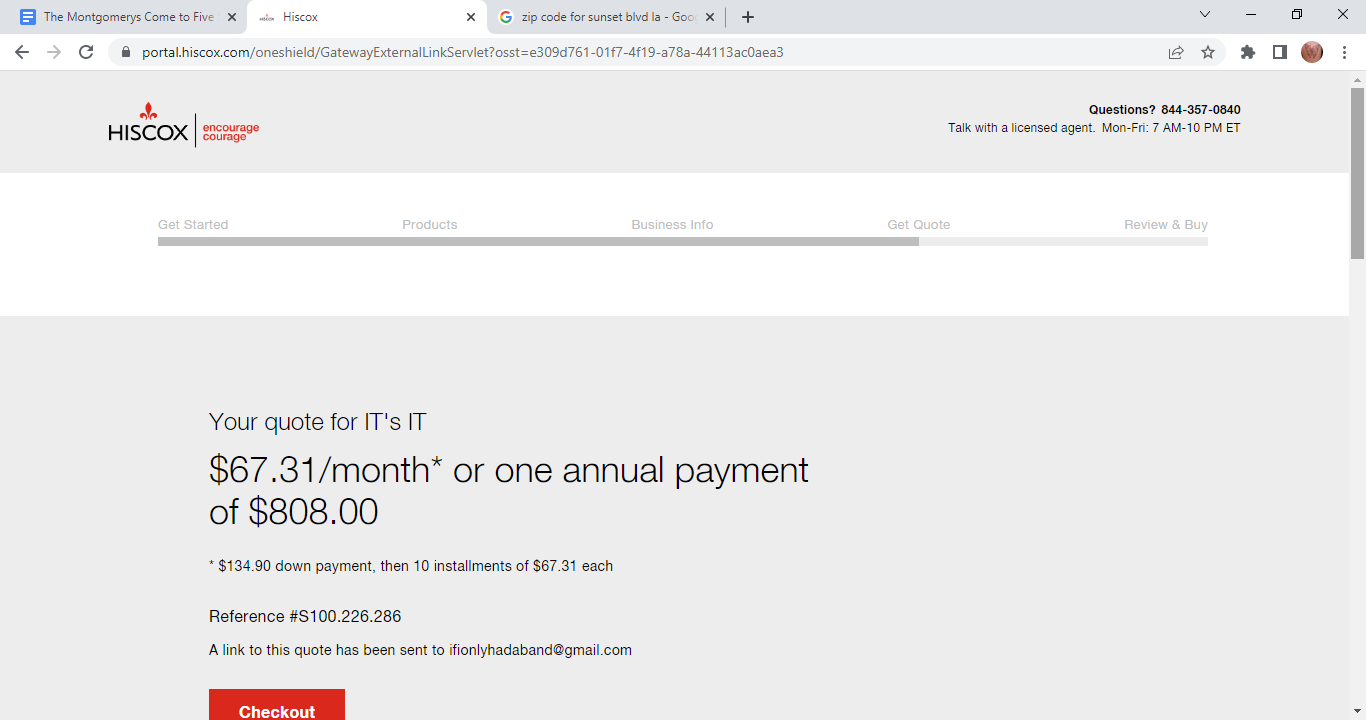

Hiscox is a pioneer to sell small business insurance completely online. They have done that for 100+ years and accumulate significant experience. Their small business coverages are designed primarily for professional services companies—accountants, consultants—they also offer coverages for other industries like fitness, health, and beauty. They offer quotes online for liability policies but refer you elsewhere for coverages like commercial auto or worker’s compensation. Hiscox may not work for you if you want one company to handle all of your policies.

This quote is for professional liability (E&O) insurance. The company offered general liability, business owners, and property insurance quotes.

Pros

- Get your quote and purchase your policy online

- 14-day money-back refund policy

- Professional liability policies cover your work anywhere

- Discounts are available if you buy multiple Hiscox products.

Cons

- Might not be able to purchase all your coverage from Hiscox

- No coverage is available in Alaska.

- Business owner’s policies unavailable in several states

- Business owners’ policies are only available to those with ten or fewer employees.

Thimble: Best for part-time tech consultants who only need coverage for a short term

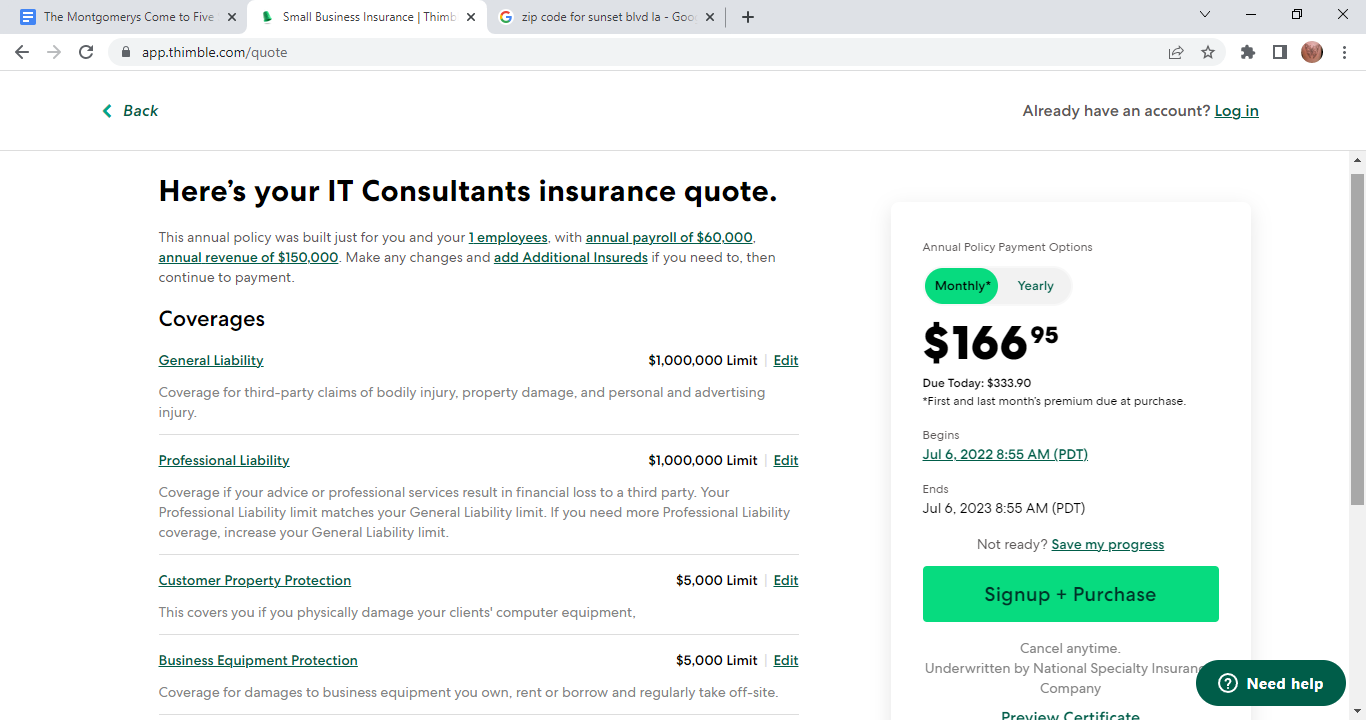

Thimble is an online insurance company that offers coverages based on the length of time you need them. You can purchase coverage by the job, by the day, by the month, or annually. If you need to get coverage quickly or temporarily, Thimble is an option to consider. The policies you purchase through Thimble are underwritten elsewhere, and any claims must be filed with someone else.

As you can see, Thimble includes general liability, professional liability, coverage for client property, and coverage for business equipment in their quote. This quote is a monthly premium, and they require the first and last month’s premium when you purchase a policy.

Pros

- From quote to online purchase in minutes.

- Certificate Manager to help verify contractor insurance coverages

- Coverage based on how long you need it

Cons

- Must file claims with the underwriting company by email or phone.

- All customer support is online.

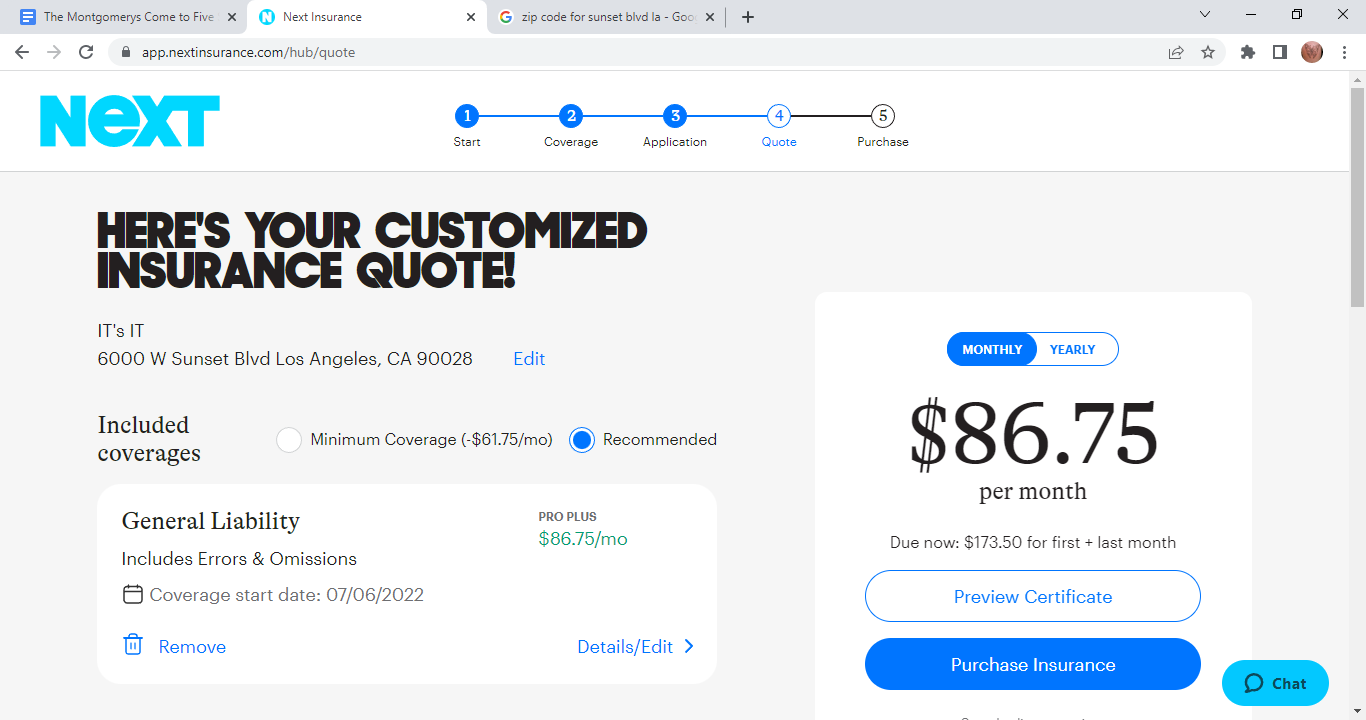

NEXT: Best for affordable bundled policy: general liability and E&O coverage

NEXT is an insurance startup founded in 2016 that sells policies online. Their policies are available individually or as bundled coverages tailored to a specific industry. They don’t offer a wide variety of specialized coverages, but they are suitable for some basic coverages. If you purchase from NEXT, you can access your certificate of insurance and share it digitally, and you can manage claims online.

The unique advantage of getting a tech E&O insurance policy from NEXT is that you will have both general liability and E&O coverage in one bundled policy, which makes it convenient and affordable for you to have proper coverage to protect your business.

Below is a quote sample from NEXT. As you can see, they provide us with a general liability insurance quote with E&O coverage included.

Pros

- Easy online application that can be completed in minutes.

- Get a discount with bundled policies.

- Online access to certificate of insurance and ability to share it digitally.

Cons

- Paperless claims process may be off-putting to more traditional business owners.

- Doesn’t offer some specialized insurance coverages.

What is E&O insurance?

E&O insurance is also known as error and omission insurance. It’s sometimes called professional liability insurance. It protects your company against claims of negligence or inadequate work. This insurance covers you if a client claims you misled them or left out critical information that impacted their financial well-being.

An errors and omissions policy will likely cover court costs and any settlement below the amount specified by your insurance company. Without this insurance, a company could be held liable for millions of dollars in damages plus the fees from hiring a legal team and going to court. An E&O policy can help mitigate, if not eliminate, the costs associated with these liability claims.

What does tech E&O insurance cover?

Tech E&O insurance covers you from the claims related to the following:

- Negligence: Errors and omissions insurance covers negligent claims. Negligence means a party (in this case, a policyholder) failed to exercise due care. A plaintiff must prove that the defendant had a duty to exercise care, failed to do so, caused harm and that the harm was reasonably foreseeable.

- Misinformation: Inaccurate advice is a common liability claim. If a client follows your advice and suffers a loss, the client could sue.

- Misrepresentation: Misrepresentations are false or misleading claims made during contract negotiations. Misrepresentation can arise in professional liability claims if the party who suffered a loss believes they could have avoided it.

- Mistake: Errors and omissions in client work are the most common basis for errors and omissions insurance claims. If you make a mistake in your advising your client, they could sue. Tech E&O insurance policy will cover you in this case.

Who needs E&O insurance?

Professionals in finance industries such as accounting or investments need E&O insurance. Any company that provides a service or advice to clients can benefit from having an E&O policy. Some regulatory bodies that govern the practices of professionals will require the purchase of an E&O policy either independently or through your employer.

Clients can sue if they suffer a loss from your advice. This is true even if they knew the risks involved and whatever caused the loss fell within the parameters you stated when offering the advice. If your client believes you made a mistake that cost them, they can sue you. Your insurance policy would cover your legal fees, court costs, and likely any damages awarded to your client, which would save your business a substantial financial difficulty—possibly even bankruptcy.

Below are some typical industries that need E&O insurance coverage:

- Advertising and marketing firms could be sued if they create an ad or digital experience with a mistake that costs their client money

- Accountants are often taken to court if they make calculation errors that result in financial losses for their clients. Learn more at best E&O insurance companies for accountants and CPAs

- Consultants are often sued if the recommendations they make to their clients cause harm to their businesses. Learn more at best professional liability insurance for consultants

- Educators could be sued because students think they taught them something wrong and it caused harm. Learn more at the best professional liability insurance for teachers

- Engineers could be held liable if they misinterpret architectural plans and make a construction error that keeps a structure from being approved for use. Learn more at the best professional liability insurance for engineers and architects

- Florists and wedding planners may be held legally responsible for not delivering flowers, a cake, the right photographer, or any other contractually required service. Learn more at the best insurance for wedding planners

- Hair stylists are often sued if they cut, burn or otherwise harm a customer while trimming, styling, or coloring hair. Learn more at the best business insurance for hair stylists and hairdressers

- Lawyers and law firms are often held legally liable if they provide advice to clients that’s wrong, incomplete, or in any way makes their legal situation worse. Learn more at the best legal malpractice insurance companies

- Medical and healthcare professionals are frequently sued for malpractice if the service they provide does not help a patient get better or makes their condition worse. Learn more at the best medical malpractice insurance companies

- Printing and publishing companies are taken to court for things like making a mistake in a book they publish or forgetting to print invitations on time

- Veterinarians can be sued for providing care to animals that doesn’t improve their health or makes it worse.

How much does tech E&O insurance cost?

The average cost of a tech E&O insurance policy is around $82 per month, or $984 per year. This is for one tech or IT consultant.

If you buy tech E&O insurance policy for your tech consulting firm, it may cost more. A small tech consulting firm pays on average $320 per month for their tech E&O insurance policy. You will pay more or less depending on several factors, which we are discussing in details below.

Keep in mind that these are just the averages. Your rates will be different. Be sure to shop around with a few companies or work with a top broker CoverWallet or Simply Business to compare several quotes to find the cheapest one for you.

Factors impacting tech E&O insurance cost

The cost of an E&O policy varies depending on several factors. Those factors include:

- The kind of business you have

- The nature of your IT or tech consulting service

- The size of your business

- Where your business is located

- The experience of your business, ie. how long it has been around

- Any claims that have been paid on your behalf in the past.

You will be considered at higher risk if you or your company have several claims against you before taking out your E&O policy. This means that your insurance will be more expensive, and the terms of the policy could be less beneficial.

How can you save on tech E&O insurance?

Errors and omissions insurance can cost between $500 and $1,000 per employee annually. You need to verify that any policy you purchase will fulfill legal, contractual, or governing body requirements you may have to meet. However, you don’t want to be financially responsible for a policy with too much coverage or insufficient coverage. In these financial times, you also likely want to save as much money as possible while still having the coverage you need; here are four ways to save on E&O insurance.

Compare quotes from multiple companies

Some companies may specialize in covering your industry. Using a broker can help you compare rates from various companies at once. Don’t necessarily go for the cheapest based on dollar amount alone. Make sure you are getting the appropriate coverage you need as well.

Choose an agent who knows your business

An agent familiar with your industry and the risks involved can help you find a policy that covers the risks while adhering to your budgetary needs. They can also often find discounts you might not know to exist.

Maintain a clean claims history

As with other insurance policies, your rates go up when you have a claim against your policy. Also, it may be difficult to secure appropriate insurance if you have a record of claims against you.

Choose a higher deductible

The deductible is the amount you pay out of pocket before your insurance company pays any benefits. Choosing a higher deductible can make your premiums lower, but you must be prepared to pay that deductible should you need to make a claim.

Wrapping it up

E&O insurance is insurance professionals need to help protect them against claims that they made a mistake that cost a client financially. It’s also known as professional liability insurance. Contact an insurance professional to determine if you need to purchase an errors and omissions policy.