Colorado is a very business-friendly state, ranking 8th on CNBC’s list of the top states for business. Denver, in particular, is becoming a competitor to Silicon Valley in California. The quality of life is excellent, with tons of green space, a thriving arts scene, and a great education system. However, while not labeled a judicial hellhole just yet, Colorado is on the watch list, and the judicial branch expanded the liability of businesses that operate within the state. What does this mean for you? It means if you provide advice or services in any professional capacity in Colorado, you will definitely want professional liability insurance.

- 5 best professional liability insurance companies in Colorado

- Who needs professional liability insurance in Colorado?

- What does professional liability insurance cover?

- How much is professional liability insurance in Colorado?

- How can I find cheap professional liability insurance?

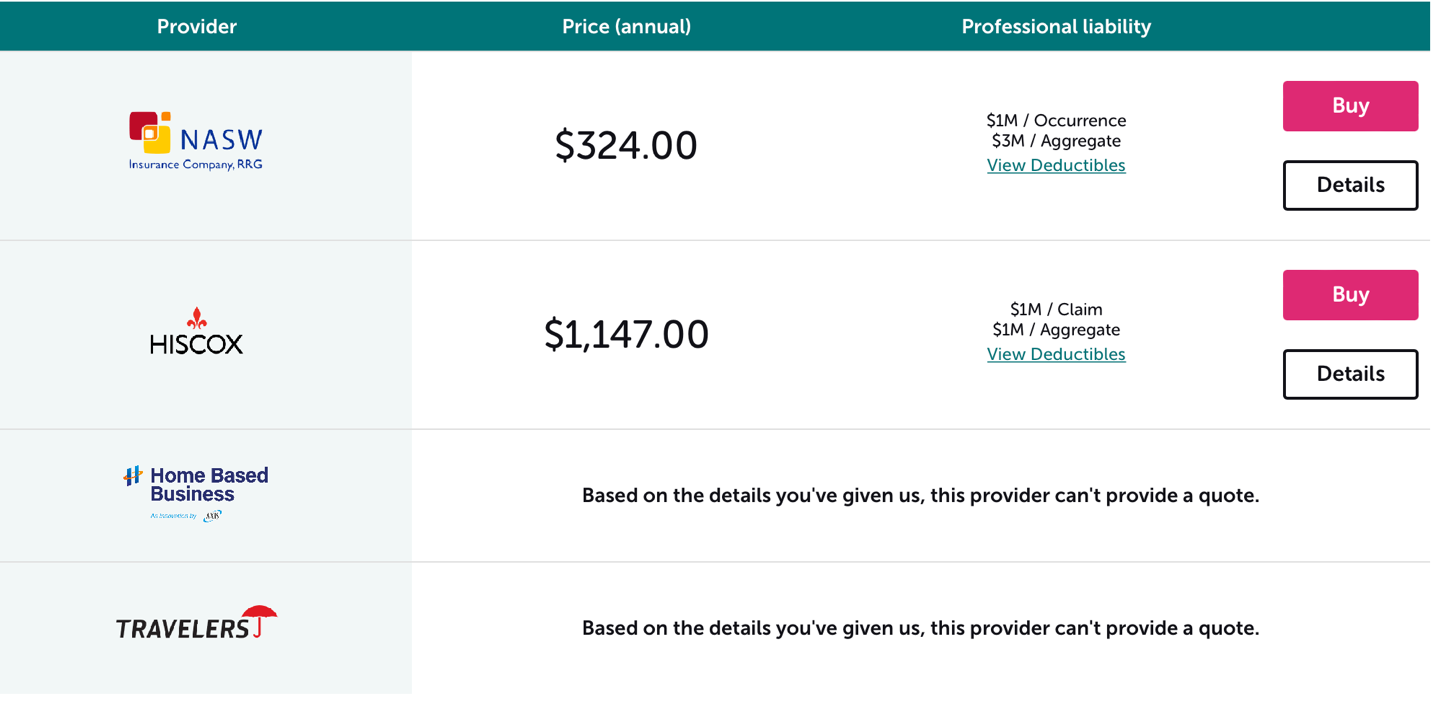

5 best professional liability insurance companies in Colorado

Hundreds, if not thousands, of companies offer professional liability insurance in Colorado. Here are the top five companies we recommend.

- CoverWallet: Best for digital experience

- Simply Business: Best for comparing several online quotes

- CNA: Best Overall

- The Hartford: Best for IT

- NEXT: Best for freelancers

CoverWallet: Best for digital experience

CoverWallet is an online insurance broker. By filling out one form, you can get quotes from three or four companies. CoverWallet partners with 20 insurance companies, including Liberty Mutual, CNA, Hiscox, Chubb, and many more.

You can usually get several quotes online fast. Comparing several quotes online is often easy with CoverWallet. However, in some cases, you have to leave an email address and quotes will be sent directly to you. Quotes are not always instant, and they can’t give you a quote from anyone they are not partnered with. You can switch insurance if, for some reason, you’re not happy with your current provider. You can file claims, pay your bill, and manage your policies online.

CoverWallet also has a great consumer satisfaction rating and is trusted by hundreds of thousands of small business owners and professionals.

Simply Business: Best for comparing several online quotes

Simply Business works like CoverWallet, in that they are an online insurance broker that pulls quotes from partner companies. Simply Business works with a few different companies that CoverWallet does, so it might be worthwhile to try both. You do have to agree to receive marketing emails and calls, however.

CNA: Best Overall

CNA offers professional liability insurance for a wide variety of professions. You can get professional liability insurance by itself or bundle it with other policies. CNA can offer you general liability, cyber insurance, workers comp, commercial auto, or umbrella insurance. You can get up to $5 million in coverage. CNA doesn’t do online quotes, however, and you’ll have to contact an agent to buy insurance.

The Hartford: Best for IT

If you work in IT, the Hartford is worth a look. You can get up to $5 million in coverage for most professions and up to $10 million for IT. They also offer many other business policies, so you can get all your insurance in one place. Policies are flexible and customizable for specific industries. You’ll have to work through an agent to purchase a policy, however.

NEXT: Best for freelancers

NEXT is great for freelancers because prices are reasonable. You can also combine professional and general liability coverages in one policy to save money. You can pay the premiums monthly or in one lump sum. The online application process is very quick and easy, and you can be covered and on your way in minutes. After buying a policy online from them, it is super easy and convenient to manage the policy with their mobile app, including filing a claim.

One negative is that NEXT is a relatively new company, they don’t have a record of years of experience yet. However, they are backed by the biggest name in the insurance and venture capital industries.

Who needs professional liability insurance in Colorado?

The simple rule is that if you are in the business of providing clients with service or advice, it is very likely that you need professional liability insurance to protect yourself and your career from lawsuits.

Colorado law doesn’t require you to have professional liability insurance. However, many employers that you work for may require this before they can employ you. Many clients would inquire you to have professional liability coverage before hiring you for your service.

Below are some professionals that are very likely to need professional liability insurance:

- Healthcare workers – Learn more at the best professional liability insurance companies for healthcare workers

- Real estate agents – Learn more at the best E&O insurance companies for real estate agents

- Insurance agents – Learn more at the best E&O insurance companies for insurance agents

- Home inspectors – Learn more at the best E&O insurance companies for home inspectors

- Financial advisors and investment advisers – Learn more at the best professional liability insurance for financial and investment advisors

- Accountants and CPAs – Learn more at the best professional liability insurance for accounts and CPAs

- Tax preparers – Learn more at the best professional liability insurance for tax preparers

- Engineers and architects – Learn more at the best professional liability insurance for engineers and architects

- Federal workers – Learn more at the best professional liability insurance for federal workers

- Private investigators – Learn more at the best professional liability insurance for private investigators

- Policemen – Learn more at the best professional liability insurance for policemen

- Teachers – Learn more at the best professional liability insurance for teachers

What does professional liability insurance cover?

Professional liability insurance covers you for any mistakes you make or anything you neglect to do in a professional capacity. For example, if you are a wedding photographer and you accidentally delete some photos, the couple could sue you for this error. That’s why it’s sometimes called Errors and Omissions insurance, and if you work in healthcare, it’s called malpractice insurance, but it all covers the same things. PLI covers:

- Mistakes or negligence: any services you provided or neglected to provide to your client that isn’t what they expected

- Misrepresentation: making claims that are not true

- Incorrect advice: providing advice to a client that causes harm (especially financial harm)

- Personal injury: any injury incurred by the client when you provide a service

- Copyright infringement: using someone’s work or likeness without permission

Keep in mind you don’t have to actually be at fault to have a lawsuit filed against you, but you will still incur legal fees and court costs before the case is dismissed. Professional liability insurance will help with these.

Professional liability insurance will not cover you for fraud, intentional acts, false advertising, or any claims made outside your policy period.

How much professional liability insurance do I need in Colorado?

Many small business owners and professionals purchase a $1 million/$1 million aggregate policy. This means you are covered for up to $1 million dollars for any single claim, and up to $1 million dollars a year in combined claims. Some professions may need more, such as lawyers, doctors, accountants, and real estate agents, as these as the professions most likely to get sued.

How much is professional liability insurance in Colorado?

Most small businesses and professionals in Colorado pay between $500 and $1,000 a year for their professional liability insurance policy.

Keep in mind that this is a wide range. To make sure you are not overpaying for your professional liability insurance coverage in Colorado, you have to shop around with a few companies or work with a broker like Simply Business, Smart Financial, and CoverWallet to get and compare several quotes in one place so that you can find the cheapest one for you.

What affects the professional liability insurance cost in Colorado?

How much you pay for professional liability insurance depends on several factors, such as:

- Revenue

- Location

- Deductible

- Claim history

- Profession

- Level of risk

Obstetricians and gynecologists pay the most for liability insurance because the chances of causing irreparable harm are higher than for most professions.

How can I find cheap professional liability insurance?

The most important thing to do is shop around. You might be surprised at how much the cost of a policy varies depending on the insurance company. For the investment of just a few hours, you can save hundreds of dollars.

Make sure you have continuous coverage so that you don’t run the risk of getting sued when your policy is inactive.

Look for discounts as well. Many insurance companies offer professional association discounts. You can also find discounts like pay-in-full, paperless billing, bundling policies, and more.

Consider raising your deductible, but make sure you can cover the deductible if the worst should happen, and you get sued.

Finally, always use a written contract. For one thing, when you go to get quotes, there will be a question about always providing a contract. If you check “sometimes” or “never” many companies won’t provide you with a quote at all. Also, a contract clearly states what you can and cannot provide and what the client can expect. Communication can eliminate many lawsuits.