Even if you’re careful and run an utterly buttoned-up business in Texas, mistakes and unintentional errors happen. If a client or customer believes a mistake or error made by you or an employee while providing services resulted in a financial loss or other harm, they can — and likely will — sue you.

Errors and omissions insurance (also known as E&O, professional liability, or professional indemnity insurance) helps cover Texas businesses if a client or customer sues because they aren’t happy with a company’s service.

In this article, I’ll reveal the top 6 errors and omissions insurers in Texas and their pros and cons. I’ll also provide you with the information you need to get the professional liability coverage that’s right for you.

- 6 Best E&O insurance companies in Texas

- What does E&O insurance cover?

- Why errors and omissions coverage is important to have in Texas

- Who needs E&O coverage in Texas?

- The cost of errors and omissions insurance in Texas

- Ways Texas businesses can save money on errors and omissions insurance

- How to find affordable E&O insurance in Texas

6 Best E&O insurance companies in Texas

Many companies offer E&O insurance in Texas. We have studied more than 25 companies and here are the 6 best E&O insurance companies in Texas:

- CoverWallet: Best for comparing several quotes

- Simply Business: Best for finding low-cost coverage

- Hiscox: Best if you prefer a more established insurer that offers a decent digital experience

- The Hartford: Best if your prefer working with an agent

- Thimble: Best for flexible short-term or temporary coverage

- NEXT: Best for the best digital experience and affordable rates

CoverWallet: Best for comparing several quotes

Would you like to compare costs and coverages for insurance professional liability insurance and manage your policy online, all in a single place? CoverWallet makes it simple for Texas business owners to do just that!

PROS:

- With CoverWallet, you can receive quotes from several insurance providers simultaneously, making it simple to compare coverage levels and premium prices.

- CoverWallet’s cutting-edge website connects all types of small business owners with the E&O coverage they need quickly and at a reasonable price.

- Its online application process is among the easiest of any insurer.

CONS:

- If you are particularly interested in one insurance company that CoverWallet doesn’t work with, you are out of luck

- When you need to make a claim, you must do it through your insurance company and not direct through CoverWallet.

Bottom line: CoverWallet makes it simple to purchase professional liability insurance through an agent or online. When you get your E&O coverage through CoverWallet, it’s simple to manage it online, including downloading your certificate of insurance, renewing your policy, and more.

Simply Business: Best for finding low-cost coverage

Simply Business is a relatively new company, founded about 20 years ago. In that time, it’s become an insurer trusted by more than 800,000 owners of small businesses.

PROS:

- Simply Business makes it fast and simple for Texas small business owners to compare several quotes and buy errors and omissions and other business insurance in just a few minutes.

- It’s easy to apply for coverage on the Simply Business website, or you can get help from an experienced representative over the phone.

- You can make a claim 24 hours a day, seven days a week.

CONS:

- You’re less able to customize coverage with Simply Business than more established insurers.

- You may be required to complete an online application process by purchasing over the phone.

- Simply Business doesn’t have as many online ratings and reviews from Texas small business owners as other insurers.

Bottom line: If you need E&O coverage fast and value a quick and easy online application process, give Simply Business a try.

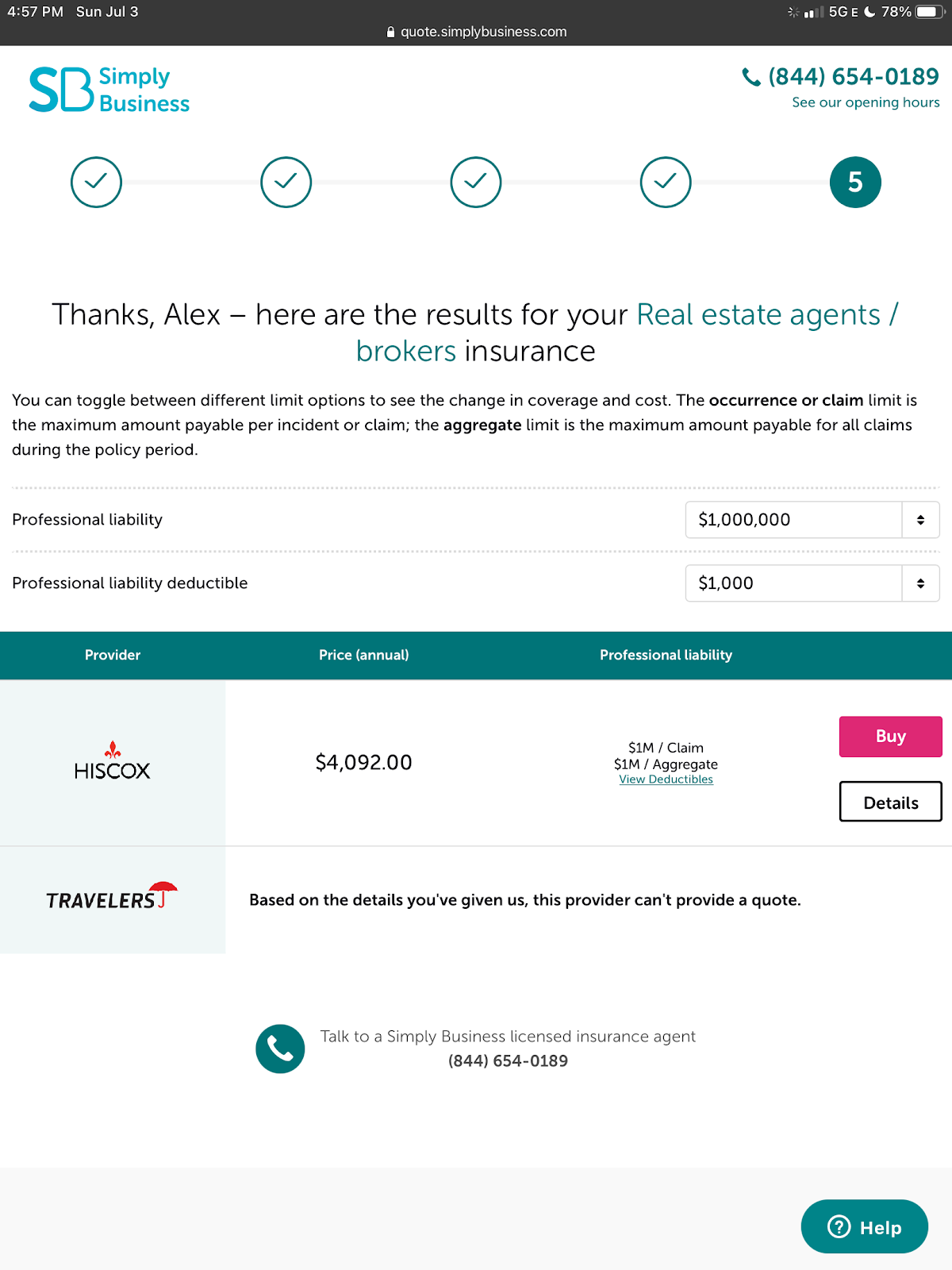

Here is a professional liability insurance quote for a small real estate business in Dallas.

Hiscox: Best if you prefer a more established insurer that offers a decent digital experience

Does your business have unique E&O and other insurance needs? Hiscox could be the perfect insurer for you. It offers a complete array of business coverages and is a leading insurer specializing in small business protection.

PROS:

- Hiscox makes it easy to purchase most business insurance online or through an experienced Hiscox representative.

- The insurer is known for its top-tier service, providing fast quotes, supplying instant coverage, and processing claims quickly.

- Hiscox is a reliable and stable company that’s been in operation since 1901. More than 400,000 companies have turned to Hiscox for their coverage.

CONS:

- Errors and Omissions coverage from Hiscox can be more expensive than other insurers.

- The company’s online systems aren’t as modern and efficient as other insurance companies.

- Not every Texas company may qualify to get professional liability protection from Hiscox.

Bottom line: You may pay more for coverage from Hiscox, but you can rest assured knowing you’re getting it from an established and respected insurance company.

The Hartford: Best if you prefer working with an agent

The Hartford is one of the oldest companies in the United States. It’s been offering insurance solutions for more than 200 years and has helped one million plus businesses with their insurance needs.

PROS:

- The Hartford has been named a World’s Most Ethical Company by the Ethisphere Institute twelve times.

- The Hartford’s longevity and focus on ethical business practices make it a company that you can feel good about getting your E&O and other business coverage from.

- The Hartford’s dedicated and highly experienced small business team is available to help company owners explore their E&O and other commercial insurance options.

CONS:

- The Hartford’s insurance prices aren’t always the lowest.

- The company’s online application process isn’t as easy and intuitive as those of online-only insurance providers.

- The Hartford has agents across the country offering its coverage, but some parts of Texas may not have local representatives.

Bottom line: The Hartford is an established insurance company known for its high level of integrity. If you find these things valuable, The Hartford could be the right insurer for you.

Thimble: Best for flexible short-term & temporary E&O coverage

Thimble is an online insurance provider that sells coverage to Texas businesses that want protection quickly or for limited periods.

PROS:

- Thimble is the best for fast or temporary business insurance.

- It’s the best choice for relatively low-cost coverage.

- Monthly, daily, and even hourly insurance is available through Thimble.

CONS:

- Thimble does not underwrite the policies it sells. Other insurers do.

- You must file claims with the company that backs your coverage.

- Thimble does not make it as easy as many other insurers to speak with someone over the phone when shopping for insurance or after purchasing a policy.

Bottom line: Thimble could be a good choice if you need limited-term business insurance coverage or to get coverage fast.

Unfortunately, when requesting a quote for this insurance from Thimble, it was not offered, so this section of the article is likely inaccurate.

NEXT: Best for the best digital experience and affordable rates

Next provides one of the best online business insurance-buying experiences of any insurer serving Texas. Its mission is to improve how small companies purchase business insurance, and it has succeeded.

PROS:

- Provides the best, most straightforward, and streamlined online insurance experience.

- Even though Next is an online insurer, you can get expert help over the phone when you need it.

- You can apply for and buy a policy, file a claim, or get a certificate of insurance anytime, 365 days a year.

CONS

- Next is a relatively new company with a limited track record.

- It has a relatively small customer base compared to other business insurers with a longer track record.

- There are relatively few online ratings and reviews when compared with other insurance companies.

Bottom line: Even though Next is a new company, you can rest assured knowing it has an excellent rating from A.M. Best, an insurance company rating agency. It has also earned a solid 4.7 customer rating. If you like shopping for things online, Next could be the ideal insurer for you.

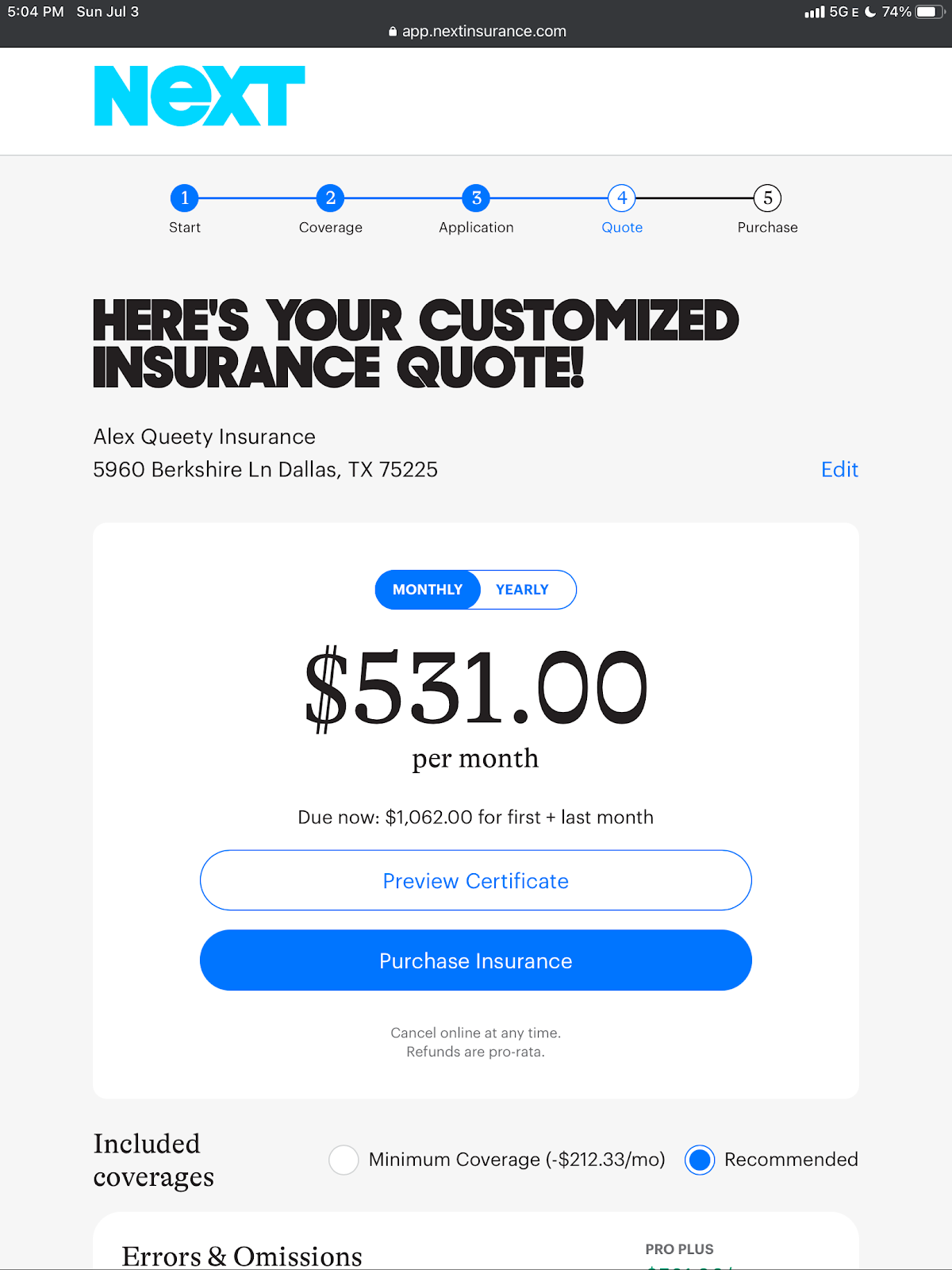

Here is a sample E&O insurance quote from Next for a small Dallas realtor

What is errors and omissions (E&O) insurance?

Errors and omissions insurance protects you and your workers against lawsuits claiming someone made a mistake when providing professional services or offered bad advice or information that caused harm. This insurance can cover legal and court costs, along with settlement expenses. These costs can add up to six figures or more, especially in risky professions like medicine and law.

What does E&O insurance cover?

Errors and omissions coverage helps protect your business from claims related to:

- Errors in services provided, including common mistakes

- Omissions, including forgetting to communicate essential things or leaving out vital information

- Negligence or irresponsibility in delivering professional services

- Misrepresentation, including saying something untrue is true

- Inaccurate advice or providing wrong recommendations

- Violation of good faith and fair dealing, including providing service that’s significantly lower quality than the profession’s norms.

If someone sues your business for making a mistake related to the services you offer, professional liability insurance helps cover your:

- Legal fees. Hiring a top-notch lawyer to represent you can easily reach five or six figures, even in a frivolous lawsuit.

- Court costs. Reserving a courtroom and hiring expert witnesses can be costly, especially in big cities like Houston or Dallas.

- Administrative costs. You could be forced to spend thousands of dollars building a defense and paying court reporters.

- Settlements and judgments. It’s not uncommon for these costs to be thousands or millions of dollars, especially for financial, medical, and legal professionals who are sued.

A business insurance specialist can explain what your E&O policy covers.

What errors and omissions insurance doesn’t cover

E&O insurance doesn’t cover claims from events that happened before your policy’s retroactive date (the first date that an issue can be covered). It also doesn’t help your business with claims filed after your policy’s extended reporting period (the period, usually three or six months after a policy ends, when a company is allowed to report an incident that took place when the policy was in effect).

Also, E&O coverage won’t help your business with claims related to:

- Illegal acts and purposeful wrongdoing, such as breaking the law with intent or lying to clients or customers.

- Bodily injury or property damage that’s caused by your business. You will need to get a general liability policy to cover these types of issues.

- Employee illnesses or injuries that are the result of work-related activities. You have to get a workers’ compensation policy to provide medical care, disability, and other benefits to employees who are injured or get sick on the job. Texas, unlike most states, doesn’t require this coverage, but it’s a good idea to secure it to protect yourself, your employees, and your business.

- Workplace discrimination or harassment that employees sue you over. Employment practices liability insurance could help cover these claims.

Why errors and omissions coverage is important to have in Texas

Think about it, would you be able to pay legal and other lawsuit-related costs out of your pocket if you or someone who works for you makes a mistake in providing work-related services and your company is sued? The answer for most Texas businesses is NO because these costs can rise into the hundreds of thousands of dollars and more. A lawsuit, even a frivolous one or one that’s dropped, often forces businesses in Texas to close their doors.

The price and likelihood of lawsuits today, especially in places like Dallas, Houston, and Austin, are the number one reason businesses need E&O insurance.

Who needs E&O coverage in Texas?

Businesses that provide services to customers should purchase errors and omissions insurance. This includes:

- Advertising and marketing firms could be sued if they create an ad or digital experience with a mistake that costs their client money

- Accountants are often taken to court if they make calculation errors that result in financial losses for their clients. Learn more at best E&O insurance companies for accountants and CPAs

- Consultants are often sued if the recommendations they make to their clients cause harm to their businesses. Learn more at best professional liability insurance for consultants

- Educators could be sued because students think they taught them something wrong and it caused harm. Learn more at the best professional liability insurance for teachers

- Engineers could be held liable if they misinterpret architectural plans and make a construction error that keeps a structure from being approved for use. Learn more at the best professional liability insurance for engineers and architects

- Florists and wedding planners may be held legally responsible for not delivering flowers, a cake, the right photographer, or any other contractually required service. Learn more at the best insurance for wedding planners

- Hair stylists are often sued if they cut, burn or otherwise harm a customer while trimming, styling, or coloring hair. Learn more at the best business insurance for hair stylists and hairdressers

- Lawyers and law firms are often held legally liable if they provide advice to clients that’s wrong, incomplete, or in any way makes their legal situation worse. Learn more at the best legal malpractice insurance companies

- Medical and healthcare professionals are frequently sued for malpractice if the service they provide does not help a patient get better or makes their condition worse. Learn more at the best medical malpractice insurance companies

- Printing and publishing companies are taken to court for things like making a mistake in a book they publish or forgetting to print invitations on time

- Veterinarians can be sued for providing care to animals that doesn’t improve their health or makes it worse.

This list isn’t a complete one. It’s meant to show the wide variety of jobs and professions that could benefit from having E&O protection.

The cost of errors and omissions insurance in Texas

Perhaps more than any other type of insurance, the price of professional liability coverage varies significantly. It will cost less for wedding planners, where the risk of a costly lawsuit is lower than for doctors who conduct complex heart surgeries.

Each professional services business has unique needs and faces different risks, so it’s impossible to benchmark the typical cost of coverage. Your errors and omissions insurance premium amount will be calculated based on the specific characteristics of your business and the unique risks it faces. However, no matter the cost, it’s a wise investment in the long-term security of the company you’ve worked so hard to build.

Having said that, on average, small businesses in Texas pay $68 per month, or $816 per year for their E&O insurance policy.

This is just the average rate that hundreds of thousands small businesses pay for their E&O policy. Your rates will be very different. Be sure to shop around with a few companies or work with a top broker like CoverWallet or Simply Business to compare several quotes to find the cheapest one for you.

Factors impacting E&O insurance in Texas

Some of the factors that impact Texas E&O insurance prices include:

- Coverage limits: Higher policy limits usually lead to higher premiums

- Deductible: The higher your deductible, the less you’ll pay for coverage

- Business risk: If you work in a high-risk industry, your premiums will be higher

- Claims history: You’ll pay more for professional liability insurance if you have a history of claims against your business

- Location: Rates are typically higher in larger cities like Dallas and Houston, where businesses are more likely to get sued than in rural areas.

Get quotes from multiple providers to ensure you’re getting the correct errors and omissions coverage at a reasonable price.

Ways Texas businesses can save money on errors and omissions insurance

You may be able to keep your professional liability insurance premium down by:

- Providing your employees with ongoing training focused on best practices in your industry. Of course, you should take advantage of the training, as well

- Hiring top talent

- Communicating with customers and clients regularly to ensure they’re satisfied with your services.

How to find affordable E&O insurance in Texas

Professional liability coverage is essential, and you shouldn’t skimp on it. Still, there are ways to find the coverage you need at a fair price:

- Shop around for the best value. Get quotes from a few companies and compare coverages and costs to find the best combination.

- Never stop shopping around. Get new quotes when it’s time to renew your policy.

- Take advantage of discounts. If they’re not offered to you when requesting an insurance quote, ask about them, whether you’re buying online or through an agent.

These steps will help ensure you’re not paying too much for your E&O and other business coverage.