According to the US Small Business Administration (SBA), California had 4 million small businesses as of 2019. While small businesses accounted for 99.8 percent of all businesses in the state.

If you are one of these business owners in California, you will agree that mistakes are unavoidable. Even with the best practices, some errors can still happen. Sadly, these errors frequently result in difficult situations with clients or customers who have suffered harm and may wish to sue you and your company.

Fortunately, errors and omissions (E&O) insurance provide a safety net for businesses that provide services to others. The policy covers costs associated with lawsuits due to the business’s mistakes while completing work.

This guide will outline the top 6 E&O insurance providers in the market in California. We will also discuss some key information regarding E&O policies and how they work in California.

- The best 6 E&O insurance companies in California

- What does E&O insurance cover in California?

- Is E&O insurance required in California?

- Who needs E&O insurance in California?

- What is the cost of E&O insurance in California?

- How to reduce the E&O insurance cost in California?

The best 6 E&O insurance companies in California

Hundreds of carriers offer E&O insurance in California. It can be confusing trying to find the best one for you. We have studied 25+ companies and here are the 6 best companies that we recommend:

- CoverWallet: Best for companies seeking affordable insurance

- Simply Business: Best for easy access

- Hiscox: Best for customizable policies

- The Hartford: Best if you prefer an established and reputable carrier and don’t mind working with an agent

- Thimble: Best for flexible, short-term or temporary coverage

- NEXT: Best user experience and affordable rates

CoverWallet: Best for companies seeking affordable insurance

CoverWallet is a broker that uses its proprietary technology to guide customers through the insurance application process and compare prices offered by the industry’s leading providers. CoverWallet works with several leading insurance companies and they get several quotes for you to compare in the same place.

CoverWallet is also among our top picks due to the number of carriers it works with, how easy it is to use, and how much assistance it offers.

Pros

- Online quotes in minutes

- Multiple carriers offer results from an application.

- Live chat and online policy and claims management

Cons

- If you want to get quote from a particular carrier that they don’t work with, you are out of luck

- Multiple carriers mean different claims and policy management processes

Simply Business: Best for easy access

Insurance doesn’t have to be complicated. Simply Business simplifies small business insurance shopping so you can save time and money and focus on your business.

Simply Business has been in business since 2005 and offers policies from top insurers. Simply Business specializes in small businesses, so if you’re a sole proprietor or have a few employees, it can help.

Simply Business simplifies and makes affordable business insurance. You don’t need to talk to agents for hours to get quotes and coverage. Start by entering basic business info or calling a licensed agent.

The following is a sample quote obtained from Simply Business for a financial advisor in San Diego.

Pros

- Simple quote process

- Easy to buy other coverage for your business and earn discount

- They work with several leading insurance companies

Cons

- Only focus on small businesses and the primary policies such as general liability, E&O, workers comp, and commercial auto insurance

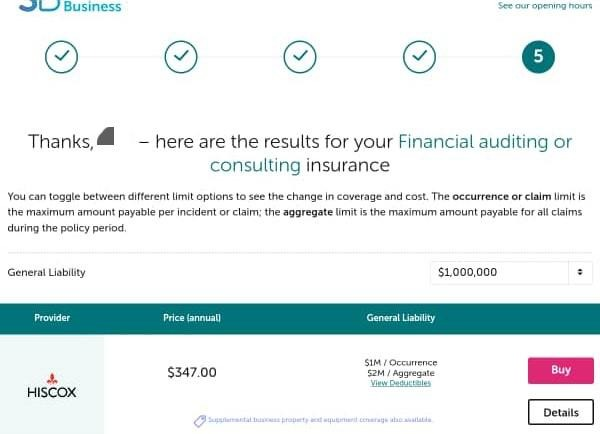

Hiscox: Best for customizable policies

When customizing a professional liability policy to meet the specific requirements of your business, Hiscox is by far the best insurance company to work with.

Most businesses develop products with a single size to accommodate what they consider to be the most important covered risks and supplemental coverages necessary for a specific line of work.

This practice reduces the amount of room for customization. However, Hiscox will write E&O policies for various businesses, allowing them to tailor their coverage to their specific risks.

Pros

- Various deductible options and coverage features are available.

- Insurance is available for full-time, temporary, and independent employees.

- Online quotes, chat, policy management, claims to report

- Will write about hard-to-place professions like healthcare, therapy, or contracting.

- A.M. Best’s A grade

Cons

- Hiscox doesn’t cover fraud or false advertising, which other carriers do.

- Narrow coverage definitions

The Hartford: Best if you prefer an established and reputable carrier and don’t mind working with an agent

The Hartford is an excellent carrier for small businesses. It has gained an excellent reputation and insuring more than million small businesses in the past 200+ years. Whatever coverage small businesses need, they can count on the Hartford providing one of the best policies.

The Hartford is capable of providing professional liability insurance for a large number of professional service firms.

Pros

- Professional liability endorsements and standalone policies are available.

- Many professions have $5 million coverage, and IT has $10 million.

- Prior acts coverage included claims for events before the policy start date.

- Bill payment, claims reporting, policy management, and quoting are online.

- A.M. Best’s A+ rating

Cons

- No chat support

- The rates can be higher than others

Thimble: Best for flexible, short-term or temporary coverage

Thimble lowers the cost of purchasing E&O insurance by offering monthly and on-demand plans that customers are free to begin, pause, and cancel at any time.

Over time, Thimble expanded its coverage to include 100 different small business professions and other products, including E&O. Thimble does not require a deposit, and there are no hidden fees or other costs involved.

Pros

- Coverage is available per day, week, or per job

- Quotes are generated in about 30 seconds

- Insurance is available for over 100 small businesses

- Instant insurance certificates

Cons

- They’re working on expanding to more states

- Complicated industries may not find coverage

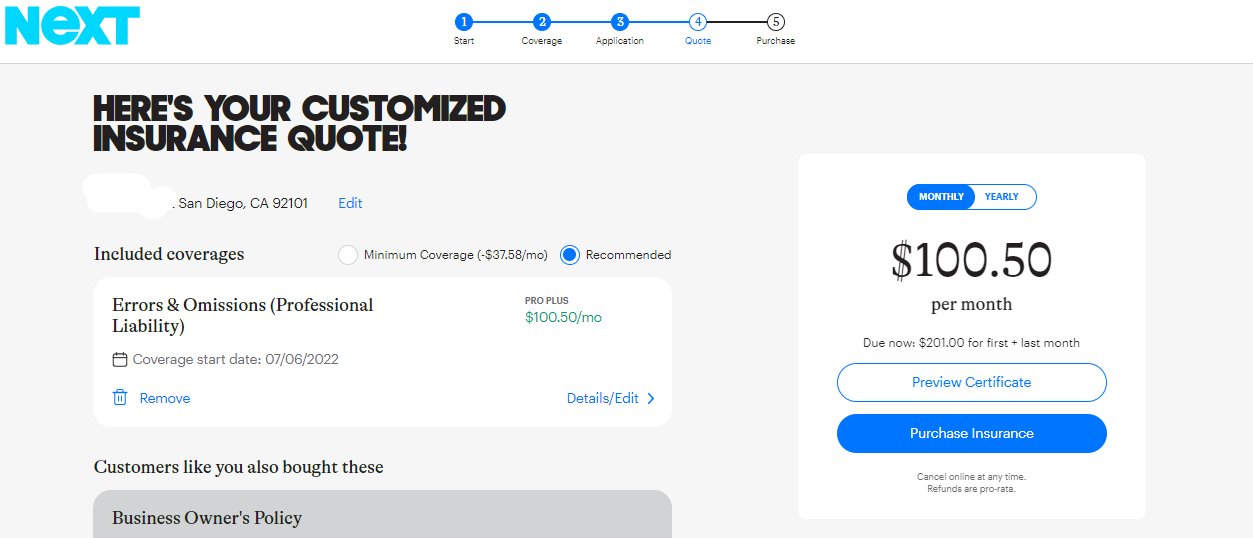

NEXT: Best user experience and affordable rates

Next’s streamlined shopping process and affordable policies make it a good choice for many businesses. Next’s errors & omissions coverage can be added to a general liability insurance policy. So if you are a contractor and you just want one primary policy, which should be general liability policy. You can easily add E&O coverage to that policy with some small additional cost.

Next tailors its E&O policies to each business’s needs. They have customized products for more than 1,000 U.S. businesses. This customization is helpful for E&O coverage, where risks vary by industry and state.

Next online quoting and shopping systems are great. Small business customers can get a quote and buy coverage online from Next in just a few minutes. Next online tools manage policies and submit claims. Online portals allow policyholders to make payments, update their policy, file claims, and track progress.

The following is a sample quote obtained from Next Insurance for a financial advisor in San Diego.

Pros

- Affordable, industry-specific policies

- Online shopping and policy management tools

- Award-wining company with AM best Excellent rating

Cons

- Larger businesses or those with complex insurance needs should look elsewhere.

E&O insurance in Los Angeles, San Diego, San Francisco, San Jose, Sacramento, Long Beach, Oakland, Bakersfield

The 6 best companies we recommend above offer E&O insurance in all cities in California. Whether you are in Los Angeles, San Diego, or San Jose or Oakland, you can consider these companies to find the best E&O policy for your business.

Keep in mind that the cost of E&O insurance depends on several factors that we are discussing below, one of which is location. The exact same financial advisor who used to locate in Bakersfield, CA just moved to Los Angeles will receive a different quote with a different rate, even from the same insurance company. So, if you happen to move from one city to another city in the same state of California, make sure that you shop around for your E&O insurance again to find the cheapest one. A different insurance company may offer you a cheaper rate than the one you had in the previous city.

What is E&O insurance?

E&O (Errors and Omissions) insurance, or professional liability insurance, is a type of insurance that protects businesses that provide services and advice from claims of negligence and other claims. This type of insurance is known as “errors and omissions” insurance because the harm a claimant alleges is usually the result of an error or omission in the service provided.

Because it is designed for businesses that provide specific types of professional services, not every business requires errors and omissions insurance. E&O insurance provides specific coverages for financial losses caused by work in fields such as real estate, architecture, and engineering. The insurance policy typically protects against claims from such professional services and advice.

What does E&O insurance cover in California?

Error and Omissions Insurance in California cover expenses up to the specified limit in your insurance contract. It will assist you in covering claims that may arise from any of the following:

Negligence

Errors and omissions insurance covers negligent claims. Negligence means a party (in this case, a policyholder) failed to exercise due care. A plaintiff must prove that the defendant had a duty to exercise care, failed to do so, caused harm and that the harm was reasonably foreseeable.

For instance, architects and engineers can be held negligent because they must create safe and sound designs to minimize harm. If a firm is negligent and liable, its professional liability policy could cover a lawsuit and damages. Negligence is a common claim under contractors’ E&O policies, especially for artisan contractors like electricians and plumbers who can cause severe damage by not taking care.

Misinformation

Inaccurate advice is a common liability claim. If a client follows a company’s advice and suffers a loss, the client could sue. Say a real estate broker researched comparable properties to help their client determine what to bid for a project site and recommended bidding far above market value. If the client sues the broker for compensation after receiving inaccurate property advice, the claim might be covered by the broker’s errors and omissions policy.

Misrepresentation

Misrepresentations are false or misleading claims made during contract negotiations. Misrepresentation can arise in professional liability claims if the party who suffered a loss believes they could have avoided it. For instance, if an architect recommends a design element to improve a building’s energy efficiency. A professional liability policy may cover such claims if the client later discovers that the design increased their energy costs.

Mistakes

Errors and omissions in client work are the most common basis for errors and omissions insurance claims. Error and omission types vary. In professional liability cases, mistakes can include issues like:

- A construction manager failing to approve a change order.

- A home inspector missing foundation cracks,

- A surveyor misidentifying property boundaries,

- An engineer miscalculating key design components,

For contractors’ E&O policies, mistakes could include issues like:

- A plumber forgetting to seal a pipe could be considered an error or omission.

- An electrician incorrectly wiring a circuit that causes a fire

Is E&O required in California?

Errors and omissions insurance is recommended for businesses that provide services but are not required in California. A business’s requirements depend on its industry and state laws, but there are other situations where it may need E&O insurance.

Law and medicine often require minimum liability coverage, but real estate, home inspections, architecture, and engineering have state-specific requirements.

If you are handling a federal project, you may need E&O insurance. Federal Acquisition Regulations require contractors to have insurance for “perils to which they are exposed.” If your company plans to bid on federal contracts, talk to an insurer about E&O coverage.

Also, some clients may require E&O coverage even if not required by state or federal law. Contracts may require a contractor to carry certain liability insurance to compensate a client for a mistake or negligence. Review bids and contracts to ensure you meet client requirements.

Who needs E&O insurance in California?

Errors and Omissions Insurance is for businesses and professionals who advise clients, make recommendations, design solutions, or represent others’ needs.

Generally speaking, these professions need Errors and Omissions insurance:

- Advertising and marketing firms could be sued if they create an ad or digital experience with a mistake that costs their client money

- Accountants are often taken to court if they make calculation errors that result in financial losses for their clients. Learn more at best E&O insurance companies for accountants and CPAs

- Consultants are often sued if the recommendations they make to their clients cause harm to their businesses. Learn more at best professional liability insurance for consultants

- Educators could be sued because students think they taught them something wrong and it caused harm. Learn more at the best professional liability insurance for teachers

- Engineers could be held liable if they misinterpret architectural plans and make a construction error that keeps a structure from being approved for use. Learn more at the best professional liability insurance for engineers and architects

- Florists and wedding planners may be held legally responsible for not delivering flowers, a cake, the right photographer, or any other contractually required service. Learn more at the best insurance for wedding planners

- Hair stylists are often sued if they cut, burn or otherwise harm a customer while trimming, styling, or coloring hair. Learn more at the best business insurance for hair stylists and hairdressers

- Lawyers and law firms are often held legally liable if they provide advice to clients that’s wrong, incomplete, or in any way makes their legal situation worse. Learn more at the best legal malpractice insurance companies

- Medical and healthcare professionals are frequently sued for malpractice if the service they provide does not help a patient get better or makes their condition worse. Learn more at the best medical malpractice insurance companies

- Printing and publishing companies are taken to court for things like making a mistake in a book they publish or forgetting to print invitations on time

- Veterinarians can be sued for providing care to animals that doesn’t improve their health or makes it worse.

What is the cost of E&O insurance in California?

The average cost of E&O insurance in California is $773 per year, or $64 per month. However, the actual cost of the policy depends on your business. As with other insurances, businesses with more risks tend to pay higher premiums.

Keep in mind that this is just the average rate from more than 1 million E&O insurance policies that small businesses in California have. Your rates will be different, can be lower or higher. Be sure to shop around with a few companies or work with a top broker like CoverWallet or Simply Business to compare several quotes to find the cheapest one for you.

Factors that affect the price of E&O insurance in California

Insurers will consider your business’s factors when setting E&O rates and terms. Here are some rate-affecting factors.

Industry

The industry is the biggest factor affecting E&O costs. Insurers charge more to cover businesses with a higher risk of costly claims. In construction and related fields like architecture or real estate, companies face different rates based on their services or specialization. Due to the potentially catastrophic consequences of a design error, architects and engineers have some of the most expensive liability insurance.

Size and revenue of the business

As a company’s employees, clients, or revenue grows, so does its risk. Having more employees or clients increases the likelihood of something going wrong and leads to a liability claim. Revenue is often a function of a company’s size. Still, earnings bring additional risk because a party may be more likely to bring a liability claim if they believe the company can pay for a suit.

Experience

Established businesses in California are safer to insure due to their track record and expertise. Therefore, companies with more industry experience pay less for insurance than newer ones.

Coverage limits and deductibles

While many factors that affect insurance costs are out of a business’s control, policyholders can usually choose errors and omissions coverage terms that increase or lower their premiums. The most important among these terms are the coverage limits and deductibles. Coverage limits increase premiums because the insurer could pay out more. Deductibles reduce premiums because policyholders retain more risk.

History of claims

When setting rates, insurers consider a business’s liability claims history. High-claims businesses are riskier to insure because their claim history may indicate poor or faulty work. Fewer claims mean lower premiums for businesses.

How to reduce the cost of E&O insurance in California?

E&O insurance can be affordable if you know your way around it. The following are some practical steps that might help you.

Improve business practices

First, improve your agency’s practices to reduce E&O claims. When you have fewer claims, your insurance costs are lower. Suggested practices include:

- Clear client communication, hearing their needs, and setting expectations

- Quality control to reduce errors in the workplace.

- Safety practices to avoid sharing private information or being hacked

Compare insurance rates.

You can check multiple insurers to find the best and most affordable coverage.

Bundle policies

Some insurers allow you to combine policies to save money. If you can, consider buying your E&O insurance with other policies to save cash.

Consider professional discounts.

Some companies may have different rates for new clients. Insurers may also offer discounts for people making electronic payments. If you want a discount, sometimes it’s best to ask.

What is excluded from E&O insurance in California?

E&O insurance covers many liability risks, but not all. Bodily injury, property damage, employment, and vehicle-related liability are generally excluded from errors and omissions insurance. E&O policies do not cover illegal acts, customer deception, or intentional harm.