California has the second most expensive workers compensation insurance in the country—only New York has higher rates. This is because the cost of living in California is higher than most areas of the country, so the rates for insurance are similarly high. You’ll need workers compensation insurance if you have even one employee in California. Obviously, you don’t want to spend more money than you have to, so here are the top providers of workers compensation insurance in California.

All the quoted rates assumed a café with 5 employees and $160,000 in payroll.

- Top 6 Providers of Workers Compensation Insurance in California

- Workers Compensation Laws in California

- How to Save Money on Workers Compensation Insurance

- Factors Affecting How Much You’ll Pay for Workers Compensation Insurance

- How Much does Workers Compensation Insurance Cost in California?

- How to Find Cheap Worker Compensation Insurance in California?

- What does Workers Compensation Insurance Cover?

- How is Workers Compensation Insurance Different from General Liability Insurance?

Top 6 Providers of Workers Compensation Insurance in California

We crunched the numbers and studied 12 companies offering workers compensation insurance in California. Here are the top 6 companies that we recommend:

- biBERK: Best for low-cost coverage from a reputable carrier

- Simply Business: Best brokerage firm to work with to find the cheapest coverage

- CoverWallet: Best for comparing several quotes online from top-tier carriers

- The Hartford: Best for Added Coverages and Highly Reputable Insurance Company

- Tivly: Best brokerage firm if you prefer working with experienced agents

- THREE: Best for simple and easy-to-understand policy without any insurance jargons

biBERK: Best for low-cost coverage from a reputable carrier

biBERK is a subsidiary of Berkshire Hathaway. They focused completely on selling insurance coverage to small businesses. Workers comp insurance is one of their coverage offerings. biBERK sells insurance completely online, offering a simple and fast online quoting. Within 10 minutes any small business owner should be able to buy a workers comp insurance policy on their website

Pros:

- Backed by one of the very best insurance brand names, Berkshire Hathaway, with unparalleled financial strength and reputation

- One of the best digital experiences, from getting quotes, buying a policy, and managing the policies completely online

- One of the most affordable rates in the industry. They claim that their customers save 20% on average

- Great customer support experience, including claim assistance

Cons:

- Their policies may have lower coverage, although still satisfying the minimum coverage requirements by the state. If you compare several policies, you should pay attention to the coverage limits of all policies

- If you prefer working 1:1 with an agent in-person, you may look elsewhere

Simply Business: Best brokerage firm to find the cheapest coverage

Simply Business is an insurance brokerage firm, focused 100% on serving small and medium-sized businesses. Simply Business offers all coverages that small or medium-sized businesses may need. They work with 30+ carriers with one single goal of helping small businesses find the coverage they need at the cheapest rate available. If your main goal is to find the cheapest rate quickly, you may want to work with Simply Business.

Pros:

- Easy to get and compare several quotes to find the cheapest one

- All carriers have good financial strength ratings and tend to offer low-cost coverage. These carriers may not be easily accessible outside of Simply Business platform

- Great customer satisfaction rating on trustpilot

Cons:

- In some cases, quotes may not be available online. You have to call to discuss your cheapest quote options

- If you prefer working with a particular carrier that Simply Business doesn’t work out, you may need to look elsewhere

CoverWallet: Best for comparing several quotes online

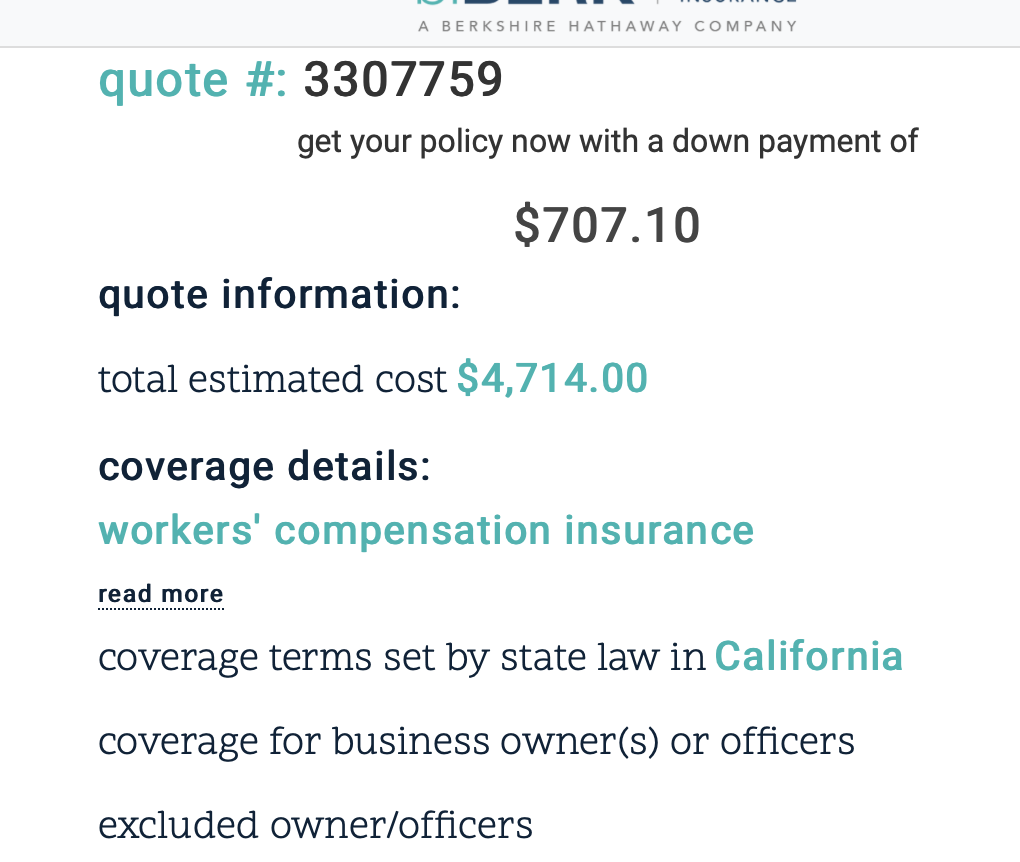

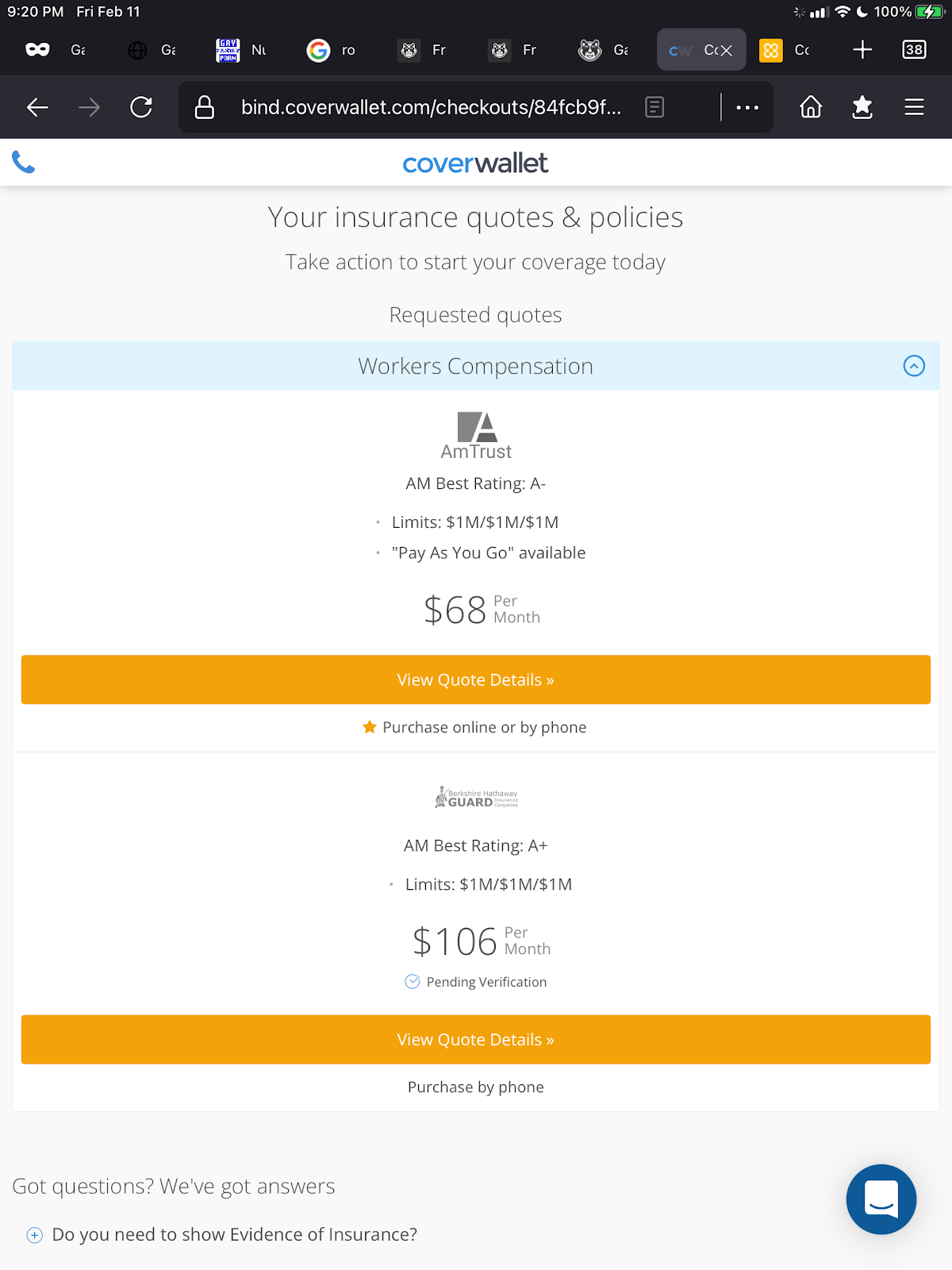

CoverWallet is a digital broker specializing in small business insurance. They work with several leading insurance companies and are able to provide you with quotes from these companies. The quote application is relatively simple and straightforward. It shouldn’t take you more than 10 minutes to get multiple quotes from multiple companies to compare.

If you want to compare several quotes online to choose the cheapest one for your company, you may want to start with CoverWallet. After buying a policy from CoverWallet, you will be able to manage all of your small business insurance through its digital platform as well.

CoverWallet has a good rating from its customers, earning a A rating on BBB. Here is a quote sample from CoverWallet:

The Hartford: Best for Added Coverages and Highly Reputable Insurance Company

The Hartford specializes in small business insurance and has over 5,000 positive reviews. They also have six added coverages to their basic workers compensation insurance, such as extended deadline stop gap coverage and voluntary compensation. You can also choose pay-as-you-go insurance, which makes budgeting easier. Should you need other types of business insurance, The Hartford can do that.

We couldn’t get a quote from The Hartford. After we put in all of our information, they told us to call them. You’ll need your FEIN to get insurance.

Tivly: Best brokerage firm if you prefer working 1:1 with an experienced agent

Tivly is another brokerage firm specializing in serving small businesses. They partner with 50+ carriers and offer all coverages small businesses may need, including workers comp insurance. One unique aspect of Tivly is they believe that small business insurance is quite complex and small business owners should work closely with an experienced agent to make sure they understand the right coverages that they need. That’s the reason why Tivly’s main focus is to match small business owners with an agent who has significant experience in the same industry and niche.

Pros:

- A large network of agents who are very knowledgeable and experienced in all industries and niches

- A large network of carriers ensures that small businesses have access to the right coverages at affordable prices

- Simple and fast experience to match small business owners and agents

Cons:

- Limited digital capabilities, ie. no online quotes

- If you prefer doing everything online, you may need to look elsewhere

THREE: Best for simple and easy-to-understand policies without any insurance jargon

THREE is another direct-to-consumer carrier belonging to the Berkshire Hathaway family. THREE was founded with a belief that all business insurance policies should be less than 3 pages and free of insurance jargon.

Pros:

- Great digital experience. Easy to get quotes, buy a policy, and manage a policy online

- Simple and extremely easy-to-understand policies

- No exclusions buried in the policy’s fine print

- Comprehensive coverage

Cons:

- Rates may not be as competitive, but reasonable for a comprehensive coverage

- Online quotes may not be consistent. Sometimes you have to call to get quotes

Workers Compensation Laws in California

You have to have workers compensation insurance even if you have only one employee. You must provide workers compensation insurance to a California employee even if your business is in another state. Sole proprietors don’t have to have workers compensation, unless you’re a roofer. If you have only part-time employees, you still need workers compensation insurance.

Businesses that use independent contractors only don’t have to have workers compensation insurance, but you may want to require them to get their own workers compensation insurance. You also need to be careful in how you classify employees, as many people falsely believe they are independent contractors when they are actually employees. The IRS can tell you about this.

There are penalties for not having workers compensation insurance, which include either a $10,000 fine or imprisonment for up to a year, or both. If a worker files a claim that goes to the Workers Compensation Appeals Board, you can be fined up to $10,000 per employee if the injury was found to be compensable and $2,000 per employee if it’s not, for a maximum of $100,000.

AB5 reclassified some employees from gig economy workers to employees, so now you have to insure them, too.

How to buy workers comp insurance in California?

Small businesses have several options to buy workers comp insurance:

- Buy it from a digital broker

- Buy it from a traditional insurance company

- Buy it from an insuretech

- Apply for self-insurance

- Buy it from the State Fund

Each option has its pros and cons. The important factor is to find options that you can compare several quotes and buy online easily. Learn more at California Workers Comp Insurance: How to Compare Quotes and Buy Online.

How to Save Money on Workers Compensation Insurance

- Opt for pay-as-you-go workers comp. The insurance is the same, but since it there are no up-front costs and it’s based on payroll, you get more accurate payments.

- Check professional organizations or trade associations for group rates

- Have a documented safety program. Actually, this is a requirement in California, so having one won’t save you money, but you still need one.

- Consider drug testing to insure a substance-free workplace.

- Check to make sure classification codes are accurate.

- Shop around and compare quotes.

Factors Affecting How Much You’ll Pay for Workers Compensation Insurance

Many things go into how much you pay in workers compensation insurance, but the biggest one is what industry you work in and how much risk is involved. People who work in roofing or construction are exposed to more risk, and therefore pay more. Other things affecting rates include:

- Amount of payroll

- Number of employees

- Claim history

- Size of business

- State laws

Some states, such as California, charge more for insurance because the overall cost of living is higher. And some, such as California, just have stricter laws. This is why California has high rates for workers compensation insurance.

How Much does Workers Compensation Insurance Cost in California?

California requires workers compensation insurance if you have even one employee, even if they’re part-time. California workers compensation insurance costs $1.56 per $100 of payroll. This is multiplied by the class code of the employee and then multiplied by how many employees you have. Some examples of how much different class codes will cost you:

- Clerical: $.040

- Restaurant/Bar staff: $4.34

- Plumbing: $7.01

- Masonry: $14.63

- Laborer: $33.57

Clerical is the cheapest classification, and laborers are the most expensive, at $33.57. So if you are employees many laborers at your company, workers compensation insurance can become very expensive, almost 1/3 of your total payroll. Be sure to shop around with a few companies or a digital broker like CoverWallet so that you can compare several quotes to decide on the cheapest one for your company.

Below is a summary of workers comp insurance costs for a small cafe in Culver City, California from several insurance companies that we are able to get quotes from.

| Carriers | Monthly workers comp insurance costs |

| Guard (through CoverWallet) | $297 |

| Pie | $378 |

| California State Compensation Insurance Fund | $303 |

| biBERK | $393 |

| Huckleberry | Not final quote ($159 – $185) |

This illustrates that workers comp insurance costs vary by provider. Be sure to shop around to compare several quotes before making your final decision.

>>MORE: How Much does Workers’ Compensation Insurance Cost?

How to Find Cheap Workers Compensation Insurance in California?

California is in the top 3 states with the most expensive workers compensation insurance. It can be a significant expense to your business, that is legally required. Finding the cheapest workers comp insurance for your business in California is important to keep the operating costs of your business low. Make sure you follow the tips below to find the cheapest workers comp insurance for your company in California.

Always compare several quotes:

Make sure you shop around with a few insurance companies or a digital broker to compare several quotes to get the cheapest workers compensation insurance quote for your business

State programs:

Check if there is any state savings program offered by California that your business can be qualified for.

Group insurance:

If your company is a member of a larger association in California, you may be able to get a group rate on your company’s workers compensation insurance.

Identify potential hazards and fix them.

Once you fix them, make sure you notify your insurance agent (if you have one) or report it to your company. Continue improving the safety standard in your company’s workplace and ask for annual reviews when you renew your company’s workers comp insurance policy.

Invest in safety education.

According to Safety and Health, for every dollar you spend on injury prevention, you’ll earn a ROI of between $2 and $6 dollars. If you’re wondering how to start a safety program, OSHA (Occupational Safety and Health Administration) is a good place to start. After having the safety program in place, you may want to ask your agent to review the workers compensation insurance quote for your company if you are qualified for any discount.

Consider drug testing.

It should come as no surprise that workers who show up under the influence of drugs or alcohol are more likely to injure themselves or others. Consider to conduct regular drug testing programs for your employees and provide relevant training and incentive programs for your employees to show up at work completely sober.

Check classification levels.

Every employee type is assigned a classification level, and each level is assigned a rate that reflects the level of risk this type of job has. Obviously, a secretary is exposed to much less risk than a construction worker, even if they work at the same company. Make sure everyone is classified accurately and regularly update this as you are hiring new employees.

What does Workers Compensation Insurance Cover?

Workers compensation insurance covers:

- Medical expenses for injured or ill employees

- Rehabilitation expenses

- Disability payments

- Employer liability (if an employee or their family sues you)

- Supplemental job displacement vouchers (these help with retraining costs if your employee becomes disabled and can’t do their original job)

- Death benefits (if your employee dies from a work-related accident or illness)

>>MORE: How to Find Cheap Workers Compensation Insurance?

>>MORE: Best 7 Workers’ Compensation Insurance Companies for Small Business

Who is exempt from workers comp insurance in California?

California is one of the strictest workers’ comp states. It only allows two exemptions to getting the coverage:

- Sole proprietors who decide they don’t want it

- Employers who are allowed to self-insure.

Self-insured workers compensation insurance in California

California has the largest number of employers currently in the self-insured program. As of Jan 2021, more than 7,000 California employers are self-insured workers comp insurance, both in private and public sectors.

Employers who want to self-insure their workers comp insurance liabilities have to apply with the Office of Self-Insurance Plans (OSIP) for approval. New private employer applications usually takes 21 days from application submission to self-insured certificate of insurance issuance. The self-insurance application is evaluated on a couple of dimensions: financial strength, proposed delivery of benefits, and suitability for the self-insurance program.

Employers in the workers comp self-insurance program are required to meet annual obligations from the state.

Learn more about the California self-insured workers compensation insurance program.

Do independent contractors or 1099 employees need workers comp insurance in California?

In California, independent contractors and 1099 employees are not required to have workers’ compensation insurance. However, it is recommended that they obtain insurance coverage to protect themselves in case of on-the-job injury or illness. Employers are only required to provide workers’ compensation insurance to employees classified as such and not independent contractors.

If an uninsured independent contractor or 1099 employee is injured while working in California, they may not be able to get their employer to pay for workers’ compensation benefits because they are not considered employees under state law. In California, only employees are eligible for workers’ compensation benefits, and employers are only required to provide these benefits to employees, not independent contractors or 1099 employees.

However, if an independent contractor or 1099 employee is misclassified as an employee, they may be able to receive workers’ compensation benefits if they can prove that they were wrongly classified and that they meet the criteria for employee status. They can contact the California Division of Workers’ Compensation to learn more about their options in this situation.

Learn more details about workers comp insurance for contractors and 1099 employees here.

Workers comp insurance in San Diego, CA

Workers com insurance is required in San Diego, CA, the same as in the rest of California. Small businesses employ 59% San Diego workforce, about 697,000 employees. The median salary of San Diego workers is $80K and major industries are defense, tourism, and technology. These small businesses are required to have workers comp insurance for their employees.

If you are looking for affordable workers comp insurance in San Diego, consider the 6 companies we recommend above.

Workers comp insurance in San Francisco, CA

Similar to their counterparts in San Diego, small businesses in San Francisco, CA are required to have workers comp insurance. Small businesses in San Francisco should expect to pay a bit higher than those in San Diego because the median employees’ salary is San Francisco is $103K, more than 25% higher than that in San Diego. Workers comp insurance cost depends on employees’ payroll. Without higher payroll, small businesses should expect to pay more for their workers comp insurance coverage.

To find cheap workers comp insurance for your small business in San Francisco, be sure to compare several quotes from the companies that we recommend above to find the cheapest one for your company.

How is Workers Compensation Insurance Different from General Liability Insurance?

General liability insurance protects your business from claims that you caused:

- Property damage (to someone else’s property, not your own)

- Bodily injuries to clients

- Advertising injuries (slander, copyright infringement, and the like)

General liability insurance does not cover your employees if they get injured on the job—that’s workers compensation insurance. General liability only covers you if a client or a customer injures themselves on your work site. Also, if an employee gets hurt at work and receives workers compensation benefits, they can’t sue and say you were negligent. They can sue you if workers compensation doesn’t cover their loss, though.

>>MORE: Cheapest General Liability Insurance for Small Businesses

Last Thoughts

Workers compensation insurance is both necessary and required in California. Don’t risk your business by skipping it. Shop around and get the best rates, and stress safety in the workplace.

>>MORE: Top 5 Providers of Professional Liability Insurance in California

>>MORE: Top 6 Providers of General Liability Insurance in California