Owners of Limited Liability Companies (LLCs) often have the mistaken impression that the legal structure protects them from lawsuits and other business threats and risks. The truth is that it may protect your personal assets from business lawsuits, but your LLC still faces the same risks as corporations and other types of businesses. That’s why LLCs need general liability insurance.

A general liability policy, also known as business liability insurance or commercial liability coverage, can help protect you from claims alleging you or the employees of your LLC caused bodily injury or property damage or reputational harm. If you run an LLC, you will need to have LLC general liability insurance coverage.

Let’s see how much an LLC general liability insurance policy costs and everything else you should know while buying a general liability insurance policy for your LLC.

- How much does general liability insurance for LLCs cost?

- Factors impacting LLC general liability insurance cost

- How to find cheap general liability insurance for LLCs

- How to get general liability insurance quotes online for LLCs

- Why should LLCs have general liability insurance?

- Are LLCs required to carry general liability insurance?

- What does general liability insurance for LLCs cover?

- What other coverages do LLCs typically buy?

How much does general liability insurance for LLCs cost?

The average cost of a $1MM general liability insurance policy for LLCs is about $55 per month, or $660 per year.

The price of general liability coverage can vary more than almost any other type of business insurance. It’s dependent on many factors, including the type of business, size of the operation, condition of business property, number of locations, and the specific risks faced by the business. The cost of this coverage can range from several hundred to many thousands of dollars a year.

The best way to ensure you’re paying a fair price for your general liability coverage is to get quotes from multiple providers. That way, you can compare coverages and costs to find the best combination for you. If you have any doubts, speak with an experienced insurance agent. We recommend you getting quotes from InsurePro, Simply Business, CoverWallet, NEXT, and Thimble. It should take 5-10 minutes to get quotes from them and you should have up to 10 quotes to compare and select the cheapest one for your LLC.

Factors impacting LLC general liability insurance cost

Several factors impact the cost of general liability insurance for LLCs. Below are some of the most important ones:

The type of your business

The type of business plays a significant role in the cost of general liability insurance for LLCs. For example, a LLC specializing in construction or roofing will pay several times more than an accounting service LLC or an IT consulting LLC.

The size of your business

The bigger your business is, the more expensive your general liability insurance is. The more stores and office locations, the more customers, and the more revenue that your business has, the more you have to pay for your general liability policy. This is simply because the bigger businesses with more locations and more customers increase the likelihood of their customers get bodily injured or property damaged and they will get sued.

Your business location

If your business is located in a state with historically higher number of lawsuits or your business locations are located in a higher risk area, insurance companies will charge more for the general liability insurance policy.

The policy details

The policy terms and details play a big role in its costs too. For example, policies with more exclusions will cost less than a more comprehensive policy. Policies with higher coverage limits and/or lower deductible will be cheaper than policies with higher coverage limits and/or lower deductible. Be sure to check your policy’s details carefully to understand its inclusions, exclusions, and other limits.

Your business’s historical claims

Last but not least, if your LLC has a clean record of claims, your premiums will be a lot less than a record of many violations and claims. In addition, an LLC with a steady record of having insurance also enjoys lower premiums that an LLC with inconsistent record of having insurance or not having general liability coverage at all.

How to find cheap general liability insurance for LLCs

LLC owners can use some of the tips below to find the cheapest general liability insurance policy:

Always ask for discounts

Remember to ask about discounts. If you buy more than one type of insurance, if you have a membership in a professional organization, or paying in full will often earn you a discount. It doesn’t even have to be business insurance. You can bundle home or auto insurance to get a discount if the company offers those types of policies.

Consider increasing your deductible.

The lower the deductible of the policy is, the higher the premiums are. So if you increase the deductible, you will reduce the cost. This will save you some money, but make sure you can cover the costs if you need to file a claim.

Don’t get more insurance than you need

You want to buy enough coverage in case of a claim but buying too much is just a waste of money. Choose an amount that offers protection without over-insuring. The lower the policy’s coverage limit is, the less the policy will cost.

Make sure you promote safety in your workspace

Post a safety plan, encourage safe behaviors and don’t leave things lying on the floor for someone to trip over.

Shop around and compare quotes

One of the best ways to save money on insurance is to compare prices from at least two or three companies. You might be surprised at how much rates can vary for the same amount of insurance coverage from different companies.

Learn more at the cheapest general liability insurance companies.

How to get general liability insurance quotes online for LLCs

There are three ways you can get general liability insurance:

- Through digital brokers and marketplaces

- Through traditional insurers

- Through insuretech startups

Here’s an overview of each, examples of insurers, and the pros and cons of them.

Getting LLC general liability insurance quotes online from digital brokers and marketplaces

If you prefer to do things online, a digital broker or marketplace could be ideal for you. Examples include:

- CoverWallet: A top online insurer that can get you competitive quotes in minutes.

- Simply Business: Another top digital broker specializing in small business and focused on finding low-cost coverage from their carriers partners for you

- InsurePro: A national brokerage specializes in finding on-demand and pay-per-day coverage for small businesses at the lowest cost

- Commercialinsurance.net: Provides quotes from local agencies so you can compare coverages and prices

Pros of digital brokers and marketplaces:

- Relatively low coverage costs because of limited infrastructure.

- Simplest way to see multiple quotes at once.

- Quick way to get coverage. Can provide you with a certificate of insurance in minutes.

Cons of digital brokers and marketplaces:

- Can sometimes be difficult to customize coverage.

- May need to complete more complex insurance transactions over the phone.

- Not all insurers are represented on every marketplace.

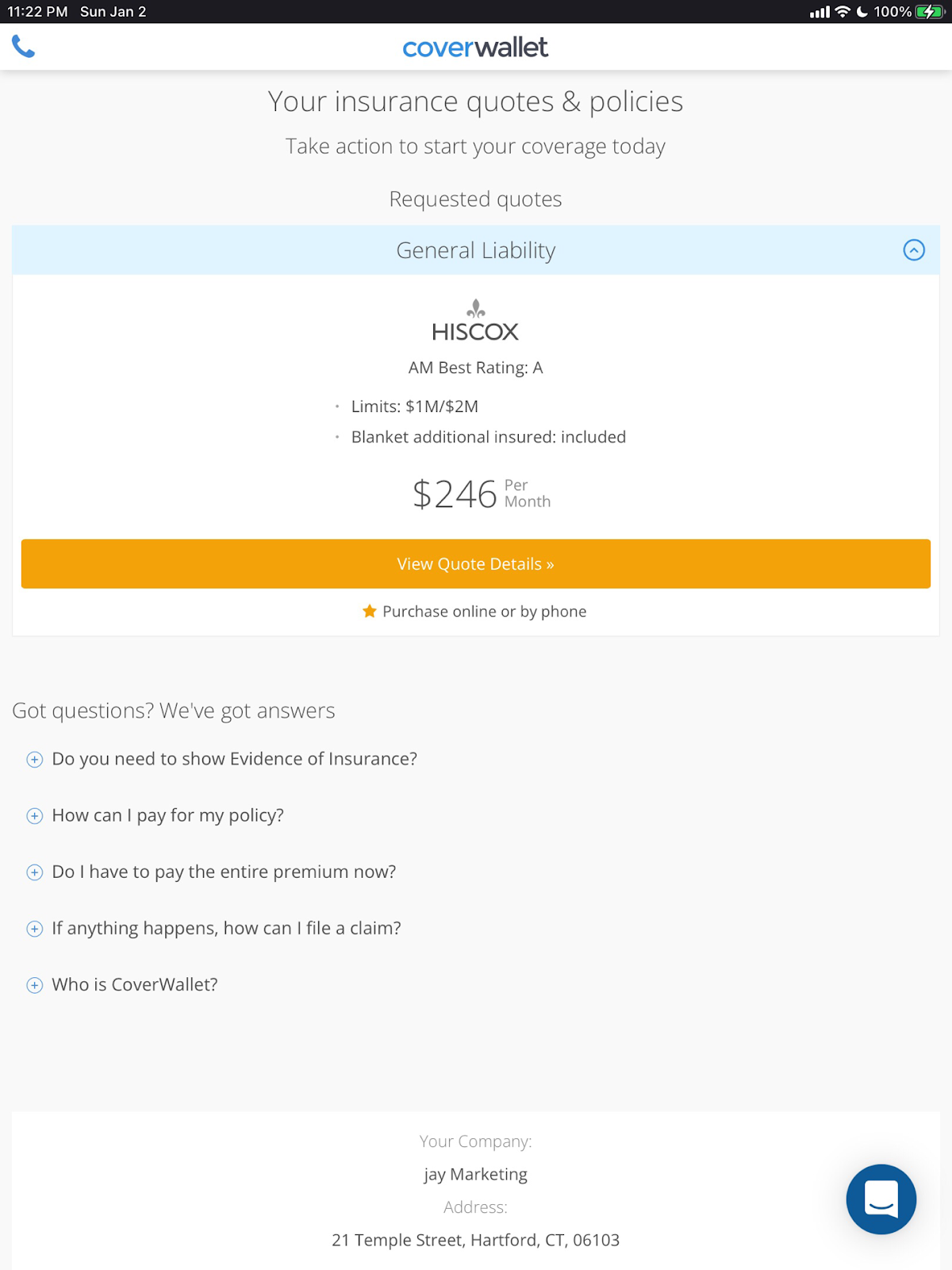

Here is a sample LLC general liability quote from CoverWallet.

Getting LLC general liability insurance quotes online from insurers

If you have more complex business insurance needs, or don’t feel comfortable buying coverage online, it might make sense for you to get protection from a traditional insurance company. Examples include:

- NEXT: A leading insuretech providing the best digital experience, focused on providing low-cost general liability insurance for all types of contractors and local businesses

- Thimble: Another insuretech specializing in newer LLCs which may not need a traditional policy covering the entire year, instead they can get short-term coverage with Thimble to save money

- Hiscox: A leading and respected multinational business insurer.

Pros of traditional insurers:

- Easy to get professional support when purchasing general liability and other LLC coverage.

- Generally committed to preventing work related risks.

- Usually financially strong and stable and able to pay claims.

Cons of traditional insurers:

- More difficult to get multiple quotes and compare them than marketplaces and digital brokers.

- Typically more expensive to get coverage than from digital insurers.

- May take longer to get coverage than from online insurance companies.

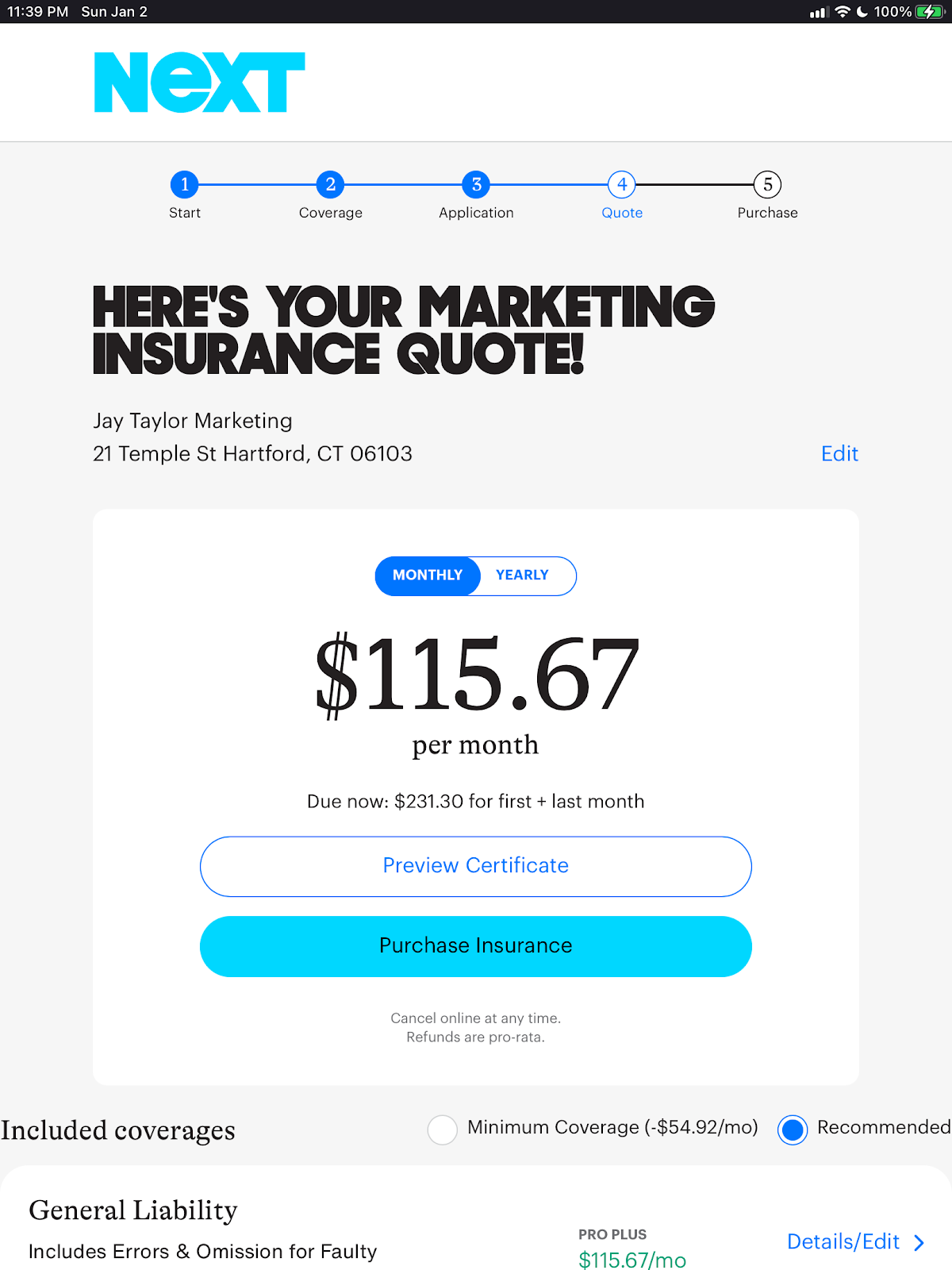

Here is a sample quote from Next.

>>MORE: The Best General Liability Insurance for LLCs

Why should LLCs have general liability insurance?

General liability insurance for limited liability companies helps protect against claims of damage to other people’s property, bodily injury, and other issues. This coverage is sometimes referred to as business liability insurance or commercial general liability insurance.

Businesses of all types, including LLCs, need this coverage because accidents, injuries, and other types of incidents often happen during the normal process of conducting business.

Some examples of covered incidents include:

- A customer at your shop trips over a wire, breaks a leg, and sues your business for medical costs.

- An electrician unintentionally causes a power surge while fixing wiring at a client’s home, damaging thousands of dollars worth of computers, televisions, and other electronic equipment.

- An employee breaks a client’s valuable vase while making a delivery to their home.

- A worker forgets to place warning cones and post a sign after washing a floor at a client’s business. Because of it, someone slips, falls, and injures her hip when walking over to the copy machine. This results in tens of thousands of dollars in medical and recovery costs.

In all these cases, general liability insurance would help pay replacement, repair, medical, legal and settlement costs resulting from the incident.

Are LLCs required to carry general liability insurance?

In most cases, your LLC is not required by law to carry general liability insurance. (The one coverage that’s typically required by states is workers’ compensation insurance, especially if you have employees.) Some employers or clients might require you to carry a certain amount of general liability coverage before you can work for them. Most landlords will require that you secure the coverage before they’ll rent business space to you. Businesses in certain industries, such as electricians, plumbers, and contractors get coverage so they can use “Licensed and Insured” as a marketing tag line.

In any case, it’s a good idea for businesses to have it. In the situations outlined in the previous section, general liability insurance would likely cover the expenses related to the incidents. If the business owner didn’t have coverage, he or she would have to pay for the damages out of pocket. Even LLCs aren’t immune to business lawsuits.

Could a lawsuit impact my personal or business assets?

Possibly. LLCs are not necessarily foolproof or impenetrable entities. The answer to this question is more of a legal issue than an insurance related one. You should consult with a legal expert to find out for sure. The good news is that the impact on your business assets could be less if you have general liability coverage.

What does general liability insurance for LLCs cover?

General liability insurance helps pay for property and other types of damage that occur as a part of doing business. It also helps cover injuries that happen on your business property. Typically, general liability insurance can help pay claims related to:

- Third party property damage caused by you or an employee while conducting business

- Medical costs if your customer or client gets hurt when visiting your business

- Reputational harm resulting from malicious slander, libel, violating a person’s privacy, and more

- Advertising issues, such as copyright infringement and mistakes on your website.

What does general liability insurance not cover?

General liability insurance provides very specific types of coverage. It doesn’t protect all aspects of your limited liability company or the risks it could face.

Here are some examples of things that are definitely not covered:

- Bad professional advice: If you or someone who works for you provides a client or customer with incorrect or incomplete advice, general liability won’t cover it. You’ll need to buy professional liability insurance to be protected. Learn more at the best professional liability insurance companies.

- Business property damage: General liability covers third party property damage, but it doesn’t cover damage to your business property, including buildings, equipment, or merchandise. You’ll need commercial property coverage for this. Learn more at the best commercial property insurance companies.

- Business Owners Policy: If you want to combine general liability and commercial property coverages in one policy to save money and make it simpler to manage, you can get a business owners policy (or BOP). It is also easier to add other coverages as endorsements to a BOP such as cyber security coverage or employment practices liability coverage. Learn more at the best BOP insurance companies.

- Crime or theft: If an employee commits a crime against your business or steals from it, general liability will not make your business whole. You will have to purchase employee dishonesty insurance.

- Data theft or loss: If your business data is lost, compromised, or stolen, your business general liability coverage won’t pay for related costs. Cyber security insurance covers those losses. Learn more at the best cyber insurance companies and the best data breach insurance companies.

- Employee injuries: Your general liability insurance covers injuries to clients, customers, and passers-by that happen on your business property. However, it doesn’t cover workers injured while on the job. You’ll need workers’ compensation insurance for that. Learn more at the best workers comp insurance companies and the cheapest workers comp insurance companies.

- Vehicle damage: If a business-owned truck, van, car, or other vehicle is damaged in an accident while being used for work related purposes, your general liability policy wouldn’t cover it. You’ll have to buy commercial auto insurance for that protection. Learn more at the best commercial auto insurance companies and how to find cheap commercial auto insurance.

What other coverages do LLCs typically buy?

There are additional types of insurance many small businesses purchase. These include:

- Errors and omissions: This covers businesses for mistakes, errors, forgetting to convey information, misrepresentations, and more.

- Employee dishonesty: Workers are often tempted to take tools and equipment from job sites. This coverage will help you recover losses from employee theft.

- Umbrella liability: This provides additional coverage over your policy’s limits. This is protection contractors who face costly risks should consider. Learn more at the best commercial umbrella insurance companies.