Whether you call it workers’ compensation insurance, workers’ comp, or something else – most businesses in Florida need to have it as coverage. It provides benefits to workers if they become ill or injured while on the job.

There are several methods of obtaining workers’ compensation in the state. This article will delve into each of them and their benefits and disadvantages so you can make the right choice for your unique business. We’ll also answer a few questions you might have about workers’ compensation in Florida.

- How does worker’s compensation insurance function in Florida?

- Is workers’ compensation insurance required in Florida?

- What are the benefits of Florida workers’ comp insurance?

- How can you buy workers’ comp insurance in Florida?

- What happens if I don’t have the required Florida workers’ compensation insurance?

- What should employers know about Florida’s workers’ compensation law?

- How are disputes over workers’ comp dealt with in Florida?

- How much does Florida workers comp insurance cost?

How does worker’s compensation insurance function in Florida?

In most cases, a Florida business with at least four employees will need to have a workers’ compensation insurance policy. This policy offers protection to employees when they are injured or become ill due to their job. In addition, it can provide peace of mind, and many clients want evidence that you have it before you begin work.

After an accident or incident occurs, a claim is submitted to ensure the employee’s medical rehabilitation or treatment is covered. For employers unable to work, this insurance can also provide a percentage of lost wages they would otherwise receive.

Is workers’ compensation insurance required in Florida?

In Florida, workers’ compensation insurance laws are more complex than in most states. Therefore, understanding whether workers’ compensation insurance is required for your business is crucial to avoid running afoul of the law. Below are all the individuals and companies required to have Florida workers’ compensation insurance.

- Any business in a non-construction field with a minimum of four part- or full-time employees must have workers’ compensation insurance for all workers.

- Companies in construction industries with at least one employee must also have workers’ comp for every employee. Be aware that independent contractors are not allowed in this field in Florida. Anyone working in construction is a business owner or a worker. If any construction work is done by a company, it must meet the rule listed.

- Those in construction who bring in subcontractors also must be sure the subcontractors have a valid exemption or their own workers’ compensation insurance. If not and an accident happens, the company contracting the subcontractor is considered to be the employer.

- Partners and sole proprietors in construction are employees based on Florida law and are included in the requirements for workers’ comp for the business. Therefore, exempting from coverage is not allowed. In addition, they must be covered to work within Florida.

What are the benefits of Florida workers’ comp insurance?

Many unique benefits are provided when a business has Florida workers’ compensation insurance:

- Compensation for medical treatments based on the illness or injury

- Permanent disability payments if the employee cannot recover from the injury or illness

- Temporary disability payments if the employee is unable to work while going through recovery

- Vocational rehabilitation benefits if an employee cannot return to their job and needs training in a new position

- Death benefits to a spouse, children, or dependant relatives if an employee dies due to a work-related illness or injury

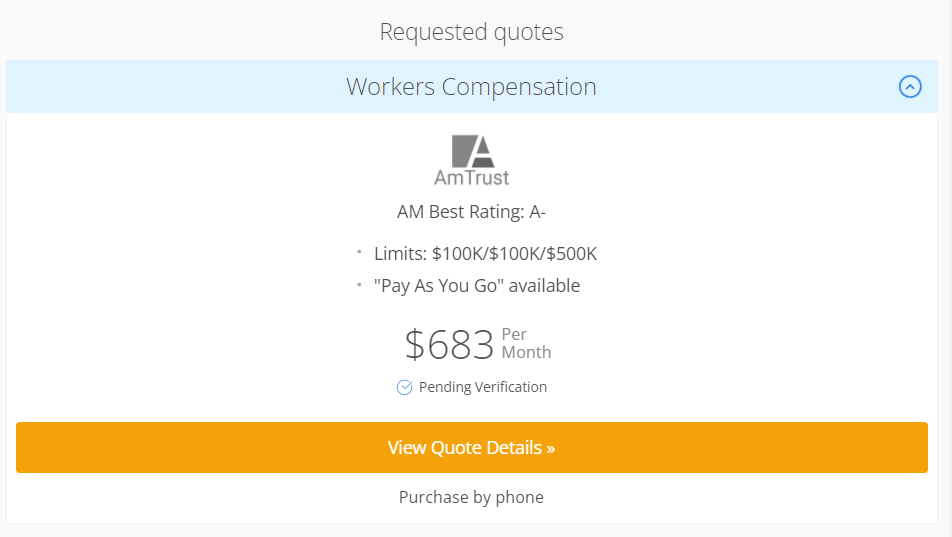

How can you buy workers’ comp insurance in Florida?

There are four major options to ensure you have the right workers’ compensation coverage in Florida. They include:

Option #1: Choose an established insurance company

Insurance providers like Employers are dedicated to offering workers’ compensation insurance to small businesses. They focus on that single product, so they are experts in the field. In most cases, these established institutions are also dependable and stable due to being insurance providers for many years.

In some cases, a specialized insurance provider will also save you money. Understanding every facet of workers’ compensation laws can equip them to avoid lawsuits and cut other costs associated with incidents that occur in your business.

However, not everything is perfect when choosing a specific workers’ compensation insurance provider in Florida. Since you are selecting a single company, you are not going to be able to compare costs. Whatever premiums are associated with the plans will be what you need to pay unless discounts come into play.

Option #2: Work with an insurtech startup

A few insurtech startups that offer workers’ compensation insurance in Florida include Pie, Cerity, and Foresight. Insurtech refers to a combination of insurance and technology. These companies provide customized premiums and plans and can be accessed through apps or on the Internet.

One benefit of these startups is that they focus on providing affordable workers’ compensation insurance for businesses. In addition, quotes are typically offered only in only a few minutes. The platform is entirely online in almost every case, which saves time and doesn’t require you to make phone calls or work with agents.

However, insurtech is still new and might not offer the same protection available through traditional policies and providers. In addition, for those who do want to speak to a human in person or by phone, there may not be a way to do so. And depending on the company, some insurtech premiums will cost more than traditional insurance.

Option #3: Try out a digital insurance broker

Another option beyond a specialized traditional insurance provider or an insurtech company is a digital broker. These include options like CoverWallet and Simply Business. An insurance broker works as an intermediary by providing various plans and premiums from several insurance providers. You can pick and choose between options to get the best plan for your business.

Some advantages of insurance brokers are that policies are available for many different types of businesses. You also aren’t forced to use policies made by one company. In addition, insurance brokers provide quick online quotes and may even allow you to make claims from their website.

On the other hand, these brokers still may not offer every policy possible. They will only show quotes and allow the purchase of policies from companies they are partnered with. In addition, there may not be an easy way to speak with an agent if you need to do so.

Option #4: Receive worker’s compensation insurance from the state fund

The state fund in Florida is administered by the Florida Workers’ Compensation Joint Underwriting Association. Policies can be written in cases where they have otherwise been declined by traditional insurance companies. As a joint underwriting association, several insurers work together to offer workers’ compensation insurance for those who have difficulty obtaining it in other ways.

If this is the method chosen to obtain insurance, it’s essential to determine whether your business is eligible. You will need to apply for coverage and provide many forms of documentation. You may be deemed qualified or be required to turn in additional information.

The primary advantage of using state funds is that these are available for any employer, even those in risky industries. However, since there is a single source, comparing quotes isn’t possible. In addition, some state funds are known for inconsistent customer service.

Learn more at the best workers comp insurance companies Florida.

What happens if I don’t have the required Florida workers’ compensation insurance?

In cases where a business does not have the appropriate workers’ compensation insurance, severe fines may be levied. The penalty for going without a policy is twice what the company would have paid in premiums while going without a policy or a minimum of $1,000, whichever is larger.

In addition, $5,000 per worker who has been incorrectly classified as an independent contractor will be required to be paid. This can easily dwarf the amount it would cost to have an inexpensive policy.

What should employers know about Florida’s workers’ compensation law?

There are three main things to remember to ensure you are meeting all laws in terms of worker’s compensation:

- You must have the appropriate amount of workers’ comp insurance for the company and workers.

- All new workers should be provided with a brochure or other material about workers’ compensation.

- A workers’ compensation notice to employees should be in every business location.

Who is responsible for paying for Florida worker’s comp?

The company pays for the insurance, and employees are not required to contribute. Therefore, there should not be a deduction seen on paychecks as there might be for Social Security, health insurance, and other benefits. In addition, since the company is paying for this insurance, generally, an employee cannot sue for becoming ill or injured on the job.

How are disputes over workers’ comp dealt with in Florida?

Disputes can occur for many reasons. For instance, a company may dispute that an injury occurred at work. But, on the other hand, an employee may feel that they aren’t receiving the benefits they are entitled to.

Rather than going to trial, many disputes result in a settlement. Two types of settlements exist for this type of situation.

Stipulated findings and award

If an employee deals with continuous medical care based on a permanent disability, they may select a stipulated findings and award settlement. The result is that the employer must pay for the medical treatments going forward.

Settlement and release

The other option involves an ill or injured employee taking a one-time payment. Accepting this amount resolves the claim, and the employee can take no further actions related to it in the future.

How are Florida workers’ comp claims made?

If an injury or illness occurs on the job in Florida, business owners must take specific steps to file a worker’s compensation claim. First, the accident or illness must be reported within 30 days (or 90 if it was an occupational exposure case). If this isn’t done, the claim may be denied.

After the report has been made, you must provide the employee with a claim form. Once this has been done, you need to give a copy to the employee, forward the form to your claims administrator or insurance company, and wait to determine eligibility based on the incident.

Florida law requires the insurance provider to quickly deny or approve benefits. If approved, the employee will start to receive benefits. If denied, the claim may be appealed.

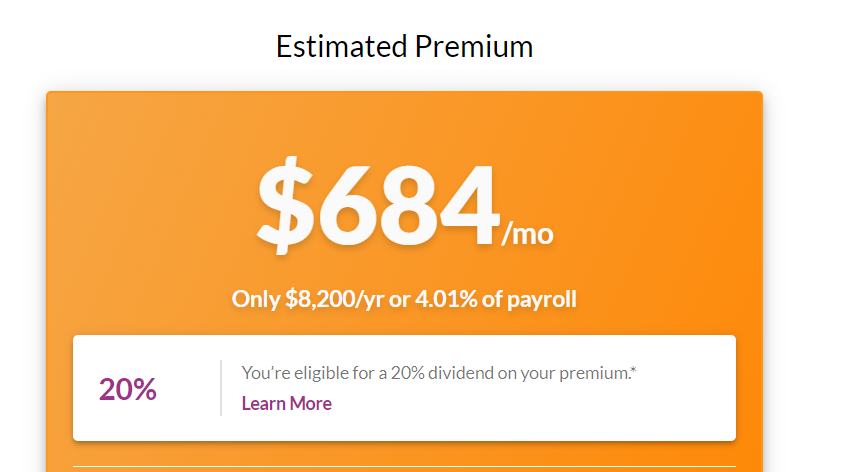

How much does Florida workers’ comp insurance cost?

Your payroll, where you are located, how many employees you have, what industry you are in, and class codes of your employees’ work will have an impact on the cost of Florida workers’ comp insurance. However, the average is $1.3 for every $100 in payroll. Learn more how to calculate workers comp insurance cost

In order to get the best price, it’s essential to shop around and get quotes from multiple companies before choosing an insurance provider.

What’s the best way to get inexpensive Florida workers’ comp insurance?

It’s also an excellent idea to shop around to see what options are available to you. Some providers will be more expensive than others, even for the same coverage. So look for the best premium price while making sure you get excellent support and claims service when it’s needed.

Establish all safety protocols at your workplace and closely monitor the safety compliance of your employees will decrease your workers comp cost over time.

Last but not least, remember to classify your business and your employees’ work in the correct class codes. Class codes plays a significant role in the cost of workers comp insurance for each business, having them right is essential.

Learn more at the cheapest workers comp insurance companies.