According to the Small Business Association, 36-53% of small businesses face litigation which costs on average $50K-100K to resolve. For this reason, it is very important to be protected by a Business Owners Policy (BOP) Insurance, which protects businesses against client lawsuits and unforeseen expenses that could force them to close for good.

A Business Owner Policy (BOP) provides three types of coverage: property, general liability, and business interruption (or business income interruption). All are combined into one ‘master policy’, or package deal combining the most important types of coverages for small to mid-sized businesses.

- What does a Business Owners Policy (BOP) Cover

- How Much does Business Owners Policy (BOP) Cost?

- The 5 Best Providers of Business Owners Policy (BOP) Insurance

What does a Business Owners Policy (BOP) Cover?

A Business Owners Policy (BOP) includes three insurance policies in one package:

General Liability Insurance protects covers a company’s legal responsibility towards property damage or bodily injury caused to third parties that are not involved in the business. One classic example is a restaurant waiter accidentally spilling a scorching cup of coffee on a customer. General liability coverage would cover any legal fees incurred by the business, along with an award payout.

Annual premiums for general liability could fall anywhere between $300 and $1,000 for the most popular policy, a $1 million occurrence/$2 million aggregate. The next most popular choice is a $2 million occurrence/$4 million aggregate policy. Higher general liability costs depend on risk. Contracting, landscaping, and food & beverage services typically see higher premiums than photography and real estate services due to the amount of work performed on private property.

>>MORE: How Much does General Liability Insurance Cost?

Property Liability: Property liability covers all of your buildings and assets, including inventories and supplies lost to fire, theft, windstorms, and other ‘acts of God.” For example, a traditional retailer could insure its building (owned or leased), electronic equipment, and products to prevent against catastrophe.

Business Interruption Insurance helps pay for the loss of income and sales in the event of a natural disaster, such as a hurricane or fire. It protects against product loss, an inability to fulfill orders, customers lost to competitors, broken vendor contracts, and additional unforeseen expenses.

In addition to the “Big Three”, additional coverages can be bundled to meet a business’s unique needs. A Business Owner Policy (BOP) may include data breach coverage for tech companies, worker’s compensation, commercial auto, and inland marine which insures assets that moves from location to location, such as contractor’s equipment and motor truck cargo.

>>MORE: What is Professional Liability Insurance? And Its Cost?

What is an Indemnity Period?

Business Owners Policy (BOP) includes business interruption insurance policy. Indemnity Period is a critical feature in business interruption insurance.

Expenses under business interruption insurance are typically paid within the indemnity period of 6 to 24-month. Indemnity Period starts from the date when damage and loss incur and end on the date no later than the last date of the indemnity period. During this time, temporary or permanent buildings, equipment, and other assets needed to run the business are paid for by the insurer.

How Much does Business Owners Policy (BOP) Cost?

Annual premiums of a BOP package vary between $500 to $2,500 a year depending on the coverage, business size, deductible, type of industry, and claims to date.

We also compare BOP quotes from 2 digital brokers, Coverwallet and CoverHound using a fictional windows company in Florida with revenue of $<1MM.

- Coverwallet: Our quote request revealed 2 quotes from Starr Companies, with a ‘Silver’ $1M/$2M package, $500 property deductible, and contents coverage of $100K for $252 a month and a “Gold” package with the same numbers plus ‘Terrorism Coverage” for $254 a month.

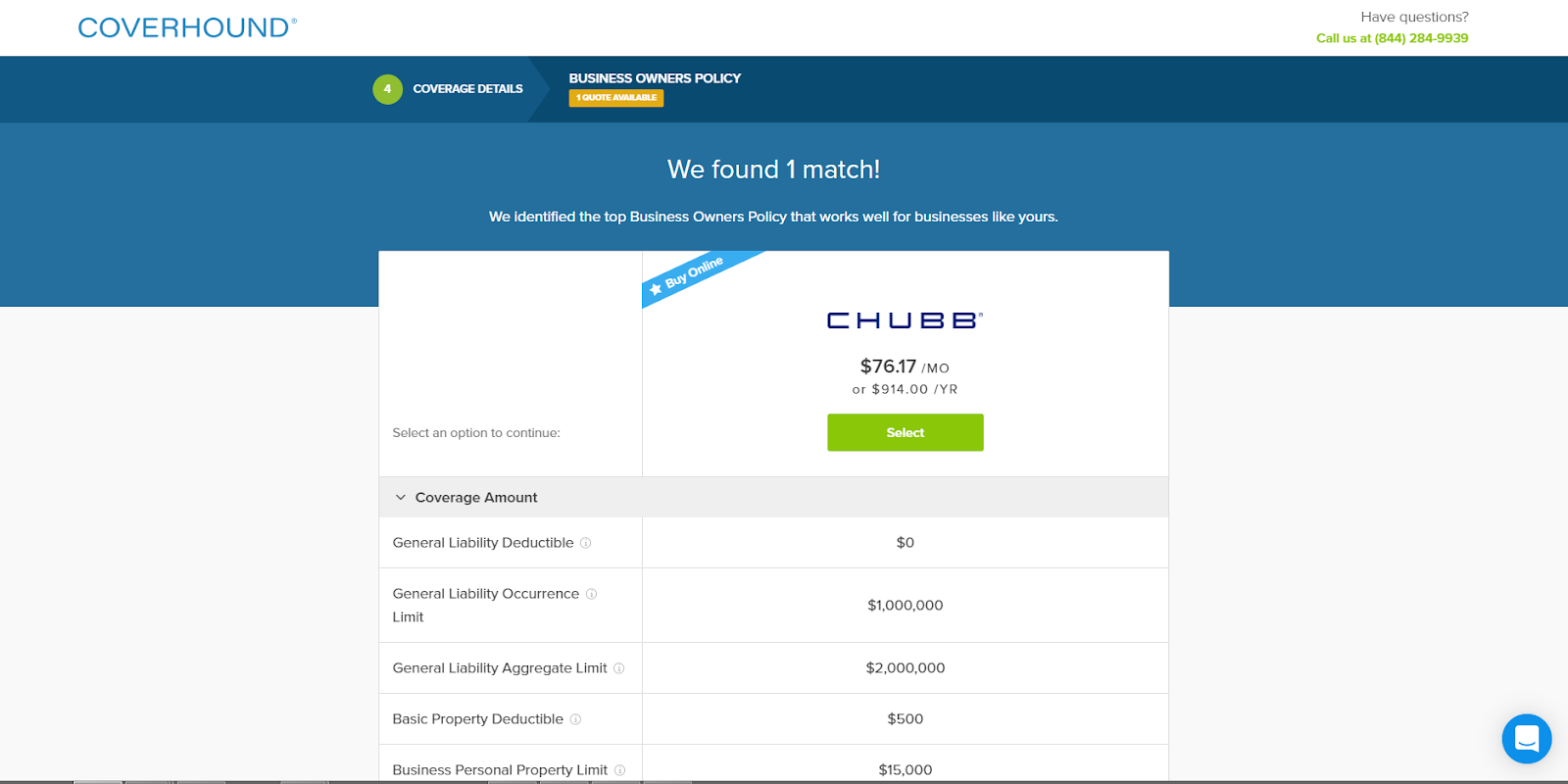

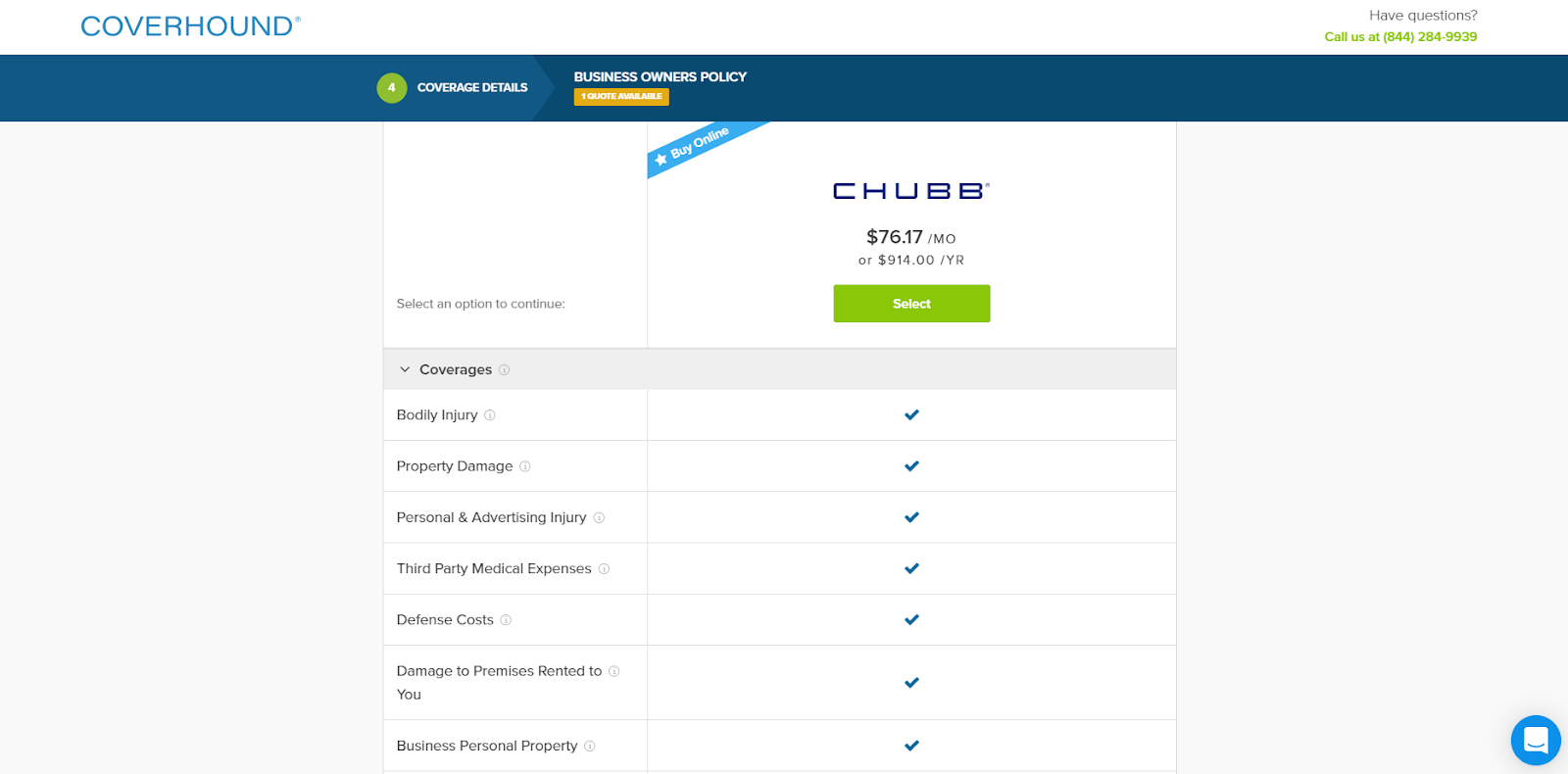

- CoverHound: Coverhound unveiled a plan from respected carrier Chubb for $76.17 a month or $914.00 a year, which covers bodily injury, property damage, business personal property, and business interruption. There is the option of monthly or annual payment plans.

The 5 Best Providers of Business Owners Policy (BOP) Insurance

We compared 12 different companies offering BOP insurance, and here are our recommendation of the 5 best business owner policy companies based on coverage quality/selection.

- CoverWallet: Best for Comparing Online Quotes

- Chubb – Best for Customized BOP Insurance

- Travelers – Best BOP Insurance for Comprehensive Coverage for All Industries

- Vouch Insurance – Best BOP Insurance for Startups

- AmTrust Financial Services – Best BOP Insurance for Small and Unpopular Industries

CoverWallet: Best for Comparing Online Quotes

CoverWallet is a digital commercial insurance broker. They work with several leading business insurance companies and have a good integration with them. Once you provide your personal information on their quote form, they will provide you with several quotes from these companies in one place to make it easy and convenient for you to compare and select the best one for your situation.

If you are new to buying business insurance for your new business, you should make some time to discuss situation with one of their agents to learn more about the types of insurance that you would need. Business insurance can be a bit more complicated than your personal insurance. A 15-minutes with a knowledgeable agent at CoverWallet will help you understand the types of risks you and your business are exposed to and make the right decision to protect you and your business.

Chubb – Best for Customized BOP Insurance

Chubb is one of the world’s largest property and casualty insurance companies, with offices in more than 50 countries. Its business owner’s policy covers small and medium-sized business owners with up to $30 million in revenue across all types of verticals, from artisans to wholesale businesses.

Its Business Owner Policy is fully customizable with additional layered options to meet each unique business’ needs, including privacy and data breach, employment practices, equipment breakdown, water back-up, and employee dishonesty coverage.

Quotes can also be obtained with a quick online form to find an independent agent within a 5+ mile radius of any zip code.

Travelers – Best BOP Insurance for Comprehensive Coverage for All Industries

Travelers offers a traditional business owner’s policy along with specialized coverages for all types of businesses, including but not limited to contractors, healthcare, pet care, and retail. It offers one of the most comprehensive resource guides we’ve seen, with a ‘Find Solutions‘ resource guide that allow users to discover insurance products by industry.

When selecting ‘Construction’ as the industry and ‘Concrete Contractor’ as the business, Travelers offers a dedicated landing page with details on its IndustryEdge product and recommended coverages, such as inland marine and contractors professional practice coverage which addresses pollution liability issues. Its ‘Insights and Expertise‘ section also has resource guides with blog titles such as “6 Top Risks for the Construction Industry” and a video on “Managing Construction Defect Risk.”

Vouch Insurance – Best BOP Insurance for Startups

San Francisco-based Vouch Insurance is a newer “fully digital” platform geared towards startups, promising “prices on average 24% cheaper” vs. competing carriers. Recently, it launched a $45M fundraising round by Y Combinator Continuity, launching in Utah before expanding to additional markets with the goal of delivering full nationwide coverage by the end of 2020.

Its Business Property and General Liability coverages are rolled up into a business owner policy that covers income interruption and off-premise business personal property. Business property coverage protects against physical assets such as computers and office chairs.

Other coverages are startup-friendly, including cyber/data breach for offer breach notification support and credit monitoring to affected customers and Management Liability insurance for litigious merger and acquisition deals.

Vouch promises applications needing only 10 minutes or less to complete. The website is very easy to use, with a live chat function connecting users to licensed insurance professionals during regular business hours, complete with thumbnails of their smiling faces. Note, Vouch is not available in all states as of the time of this writing. There is an option to join a waitlist to receive news and updates.

AmTrust Financial Services – Best BOP Insurance for Small and Unpopular Industries

AmTrust Financial Services offers insurance packages to small businesses using 9500+ agents in over 30 countries. Its business owners policy packages underwriting 350+ class codes that span all types of verticals including retail, offices, restaurants, and wholesalers. They do have a long list of exclusions, including all businesses located in Florida.

Business owners can also become eligible for discounts when a Business Owner Policy is paired with a worker’s compensation package.

Like Travelers, AmTrust also has an extensive resource library with industry news and small business titles such as “Risks, Dangers of Being Underinsured.”

Which businesses are eligible for BOP Insurance?

Typically, a Business Owners’ Policy (or BOP Insurance) is suitable for businesses with up to 100 employees or less than $1 million in revenue. When a business has more than 100 employees or $1 million in revenue, they are not eligible for BOP insurance. They have to buy separate policies for each coverage: general liability, commercial property, and business interruption insurance.

Which businesses are not eligible for BOP insurance?

In addition to its size (more than 100 employees or >$1 million revenue), some businesses in specific sectors are not eligible for business owners’ policy due to its higher-than-usual inherent risks such as restaurants or retail stores. Restaurants and retail stores like grocery stores have a much higher risks covered in both general liability and commercial property insurance compared to a dental office for example. It would be better for these businesses to have separate policies to protect them better.

What is the difference between BOP and Commercial Policy insurance?

BOP insurance is designed for smaller businesses with less risks vs. commercial policy insurance is mostly for larger businesses with higher risks. If you run a company with more than 100 employees and more than $1 million in revenue, and you want to have a package policy to cover general liability, commercial property, and business interruption risks, you should ask for a commercial policy insurance.

What is the difference between BOP and general liability insurance?

BOP coverage includes general liability. If you have BOP insurance, you don’t need general liability insurance anymore. If you already have general liability insurance policy and now consider adding commercial property insurance, you might want to get a BOP policy instead of adding commercial property policy separately. If you choose to do that, you will need to discontinue your general liability insurance policy. You don’t want to pay premiums for both general liability insurance and BOP insurance.

You should do the above especially when your business is relatively small, less than 100 employees or less than $1 million in revenue. Having a business owners’ policy will be cheaper than having both general liability and commercial property insurance policies separately.

What is the difference between BOP and commercial property insurance?

Similarly, BOP insurance coverage includes commercial property insurance. You don’t need both BOP and commercial property insurance. If your business is relatively small, less than 100 employees or less than $1 million in revenue, you might consider having a business owners’ policy instead of general liability and commercial property insurance policies separately. It will save you money with a BOP policy.

Final Thoughts

A business owner policy is your first line of defense with the unexpected slip & fall, lawsuit, and excess legal fees by exorbitant lawyers in battling cases. It could mean the difference between continuing your business and closing up shop. Save money on your small business insurance with the above carriers, offering business owners policies that could mean the difference between uneasiness and peace of mind in all of your business affairs.