Business hazard insurance protects your business from natural disasters such as fire, theft, hail, and severe storms. It’s often part of commercial property insurance. If you live in an area prone to natural disasters not covered by your commercial insurance, a separate hazard insurance policy may be necessary.

- The 5 best business hazard insurance companies

- What does business hazard insurance cover?

- Business hazard insurance vs. business property insurance: Are they exactly the same?

- Types of business hazard insurance

- Small business administration loan requirements of business hazard insurance

- How much does business hazard insurance cost?

- Who is business hazard insurance for?

The 5 best business hazard insurance companies

We research more than 20 companies offering business hazard insurance and here are our recommendations of the 5 best providers:

- CoverWallet: Best for comparing online quotes easily and quickly

- Progressive Commercial: Best if you want to get business hazard insurance as an add-on

- BiBerk: Best for a fast online quote

- Travelers: Best for comprehensive hazard coverage

- The Hartford: Best if you want to have business hazard coverage included in your BOP policy

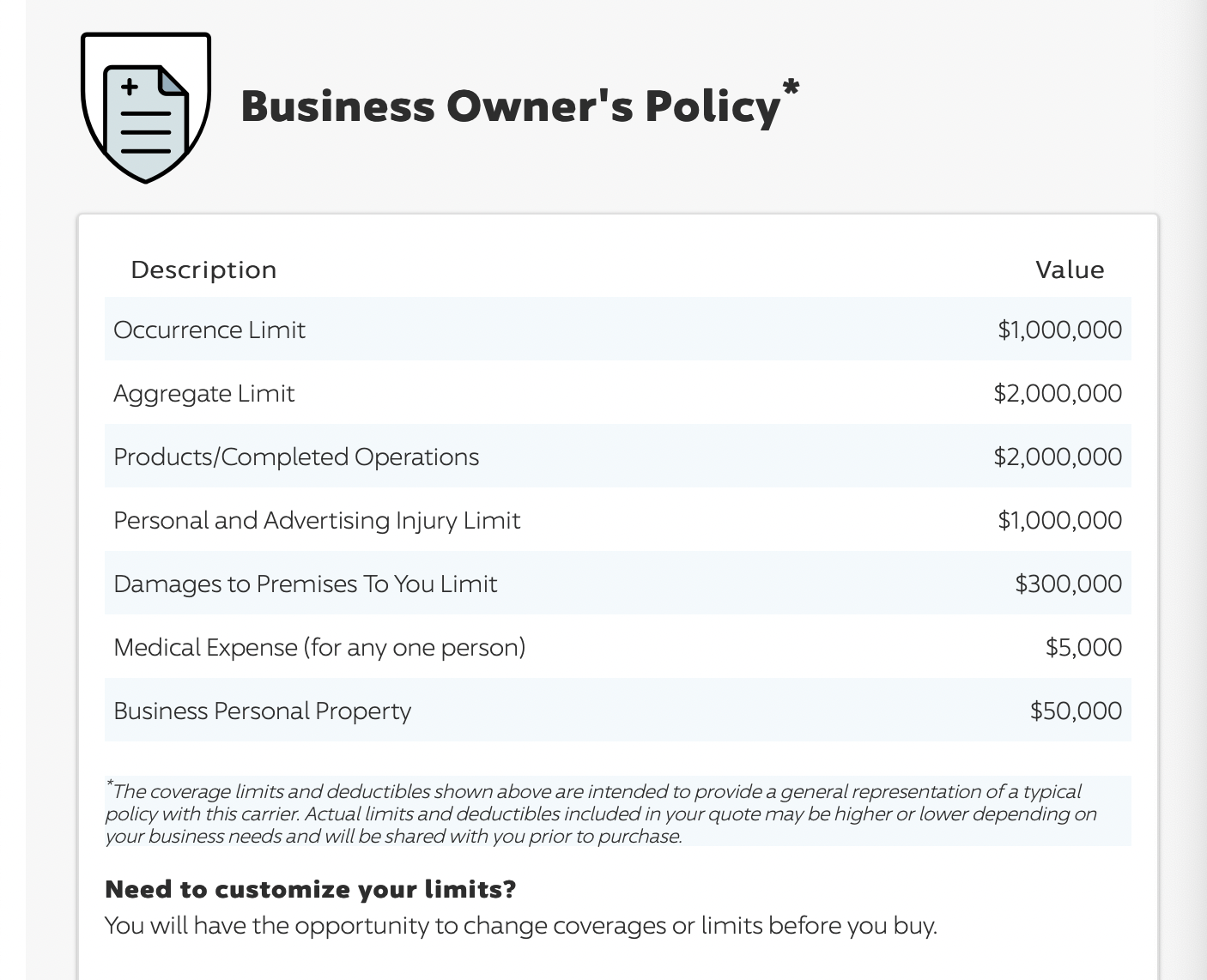

CoverWallet: Best for comparing online quotes easily and quickly

CoverWallet works with its partners to generate multiple quotes for you. Since business hazard insurance was not listed in the drop down menu and hazard insurance is often part of commercial property insurance, that’s what we asked for. This quote is for a café’ with $250,000 in revenue and three full-time employees, one-part-time. They bundled our quote with general liability, so these are business owners policies.

Progressive Commercial: Best if you want to get business hazard insurance as an add-on

Progressive has a wide range of commercial products, but they don’t offer hazard insurance as a stand-alone policy. If you want to add some type of hazard insurance to your policy, you’ll have to call to discuss those needs.

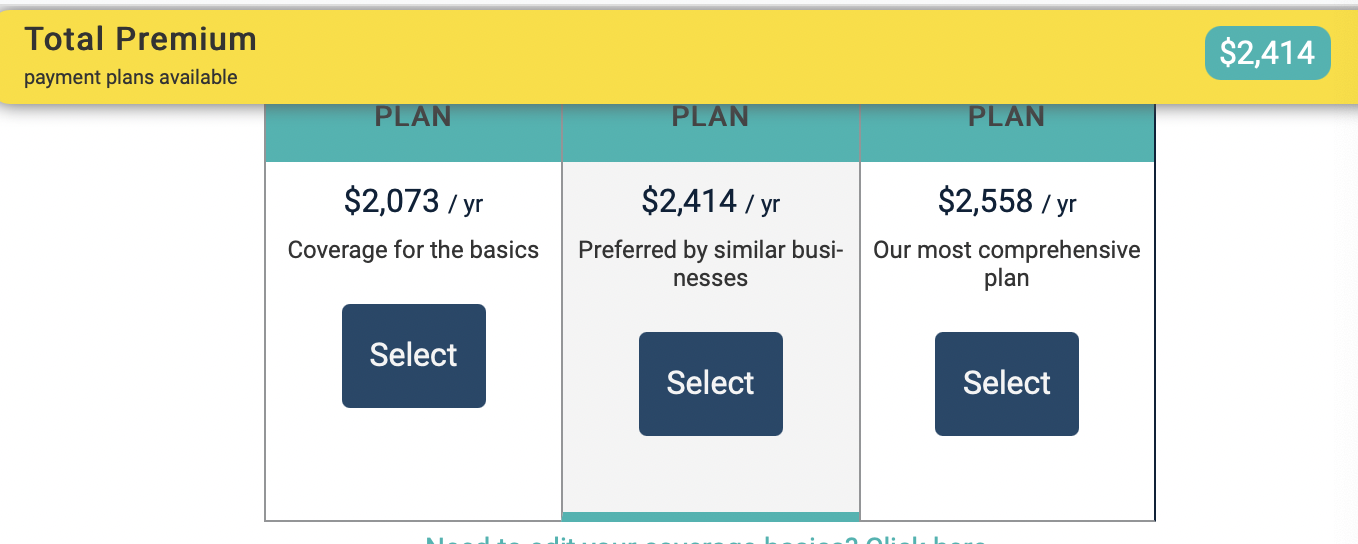

This is a quote for a business owners policy which includes commercial property insurance. The quote is for a small café that serves sandwiches and coffee in New Hampshire.

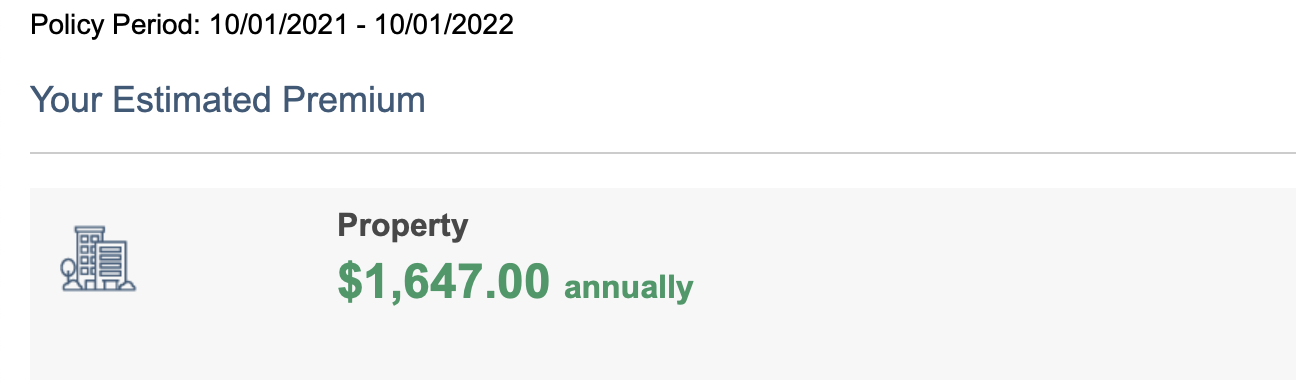

BiBerk: Best for a fast online quote

BiBerk prides themselves on making small business insurance simple and claims they can save you 20% over other companies. They use AI to generate quotes within minutes. This is a quote for a small café in New Hampshire with four employees and $250,000 in revenue a year.

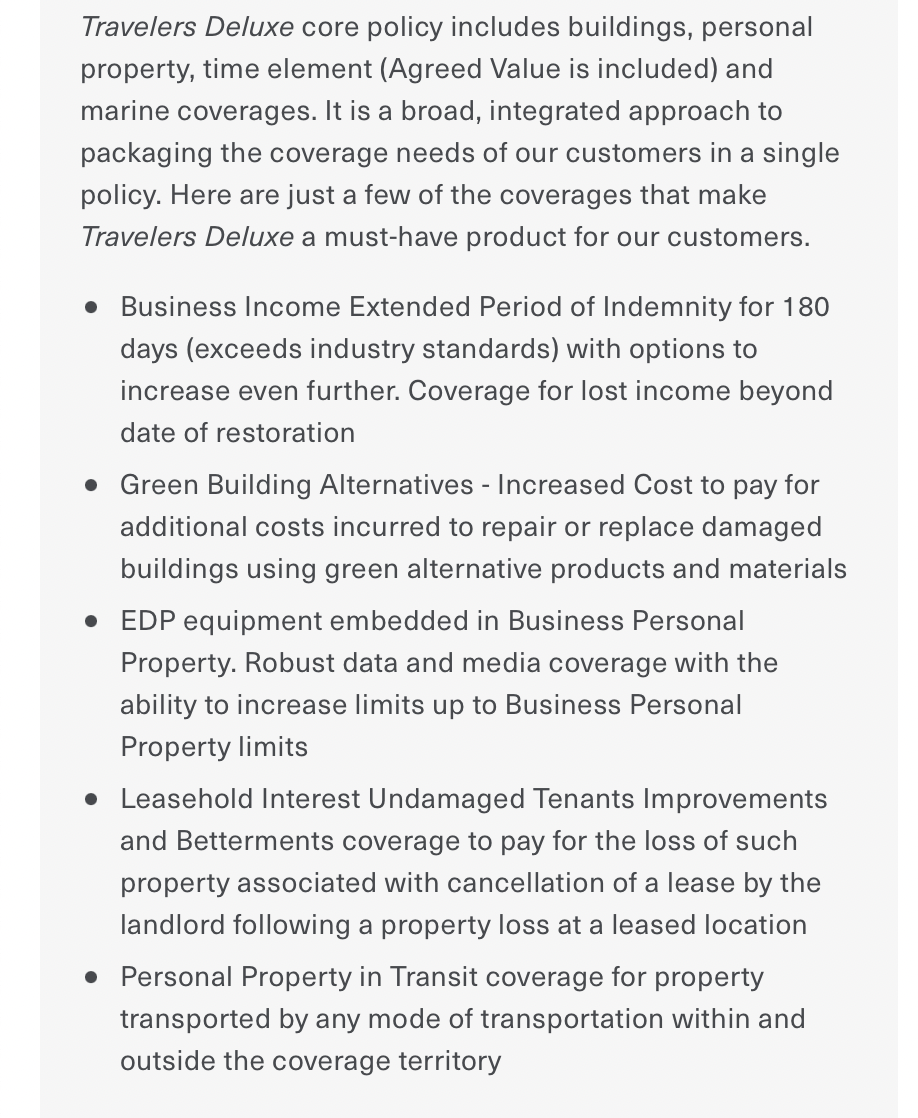

Travelers: Best for comprehensive hazard coverage

Travelers has something called Travelers Deluxe commercial property insurance. If you want a quote, you’ll have to work with an agent, but here is a breakdown of what the policy covers. It is probably the most comprehensive coverage in our research.

In general, Travelers has excellent commercial property coverage, and they will be able to cover any additional hazards common in your area.

The Hartford: Best if you want to have business hazard coverage included in your BOP policy

BOP (or Business Owners Policy) is probably the most common policy small businesses should have. It bundles general liability insurance, commercial property insurance, and sometimes business interruption income insurance policy for a reasonable price. If your business operates in a physical location and its operations depends on the physical location being able to open for business, you should definitely consider getting a BOP policy.

The Hartford has a BOP policy that’s flexible and can be adapted to cover a variety of risks, including business hazard coverage. You can get a quote online, but to complete the purchase, you’ll have to call.

What does business hazard insurance cover?

Hazard insurance that’s part of commercial property insurance usually covers things like:

- Fire

- Hail

- Snow storms

- Lightning

- Theft

- Vandalism

- Explosions

- Civil unrest

In such situations that you live in California and your business could suffer damage from an earthquake. However, earthquakes are not covered in your standard commercial property insurance policy, you would want to get additional hazard insurance for that. Likewise, if you live on the coast, you will want to get additional coverage for hurricanes and flooding.

You can get a stand-alone for such hazard coverage or you can have add-ons for these coverages.

Business hazard insurance vs. business property insurance: Are they exactly the same?

In many cases, business hazard insurance and business property insurance or commercial property insurance are essentially the same. However, for businesses located in areas prone to hurricane, flood, earthquake, or terrorism, they might be different.

That’s because the standard business property insurance doesn’t cover damages caused by hurricane, flood, earthquake, or terrorism. And if your business is located in areas prone to these perils, you need to obtain additional coverage for these. That is where business hazard insurance comes in.

Businesses located in California, California, or Louisiana definitely needs business hazard insurance coverage. And they might get a stand-alone business hazard policy which is separate from business property insurance policy.

Businesses in other areas with lesser risks of flood or hurricane, but not non-existent, like New York, might be able to add a hazard endorsement to their business insurance policy.

>>MORE: Best Commercial Property Insurance Companies

Types of business hazard insurance

Depending on where you live, you may need to add these types of hazard insurance policies:

Flood insurance: If you live in a flood zone, you probably already know that flooding is not typically covered in commercial property insurance. Flood insurance protects you from damage by any type of flooding, such as snow melt, flash floods, or storm surges.

Earthquake insurance: Residents of California who live along the San Andreas fault will want to add earthquake insurance to their policies.

Terrorism insurance: Terrorism insurance is generally an add-on to commercial property insurance and protect your business from acts of terror. It used to be included for free, but after 9/11 insurance companies started to charge for it. For a terrorist act to be covered, it must be declared a “certified act’ by the Secretary of the Treasury, according to the iii. Acts of war are almost never covered, and most nuclear, biological and chemical warfare events are also not covered.

>>MORE: The Best Cyber Insurance Companies

Small business administration loan requirements of business hazard insurance

If you apply for an Economic Injury Disaster Loan (EIDL) or Paycheck Protection Program (although that ended in May 2021) through the Small Business Administration (SBA) you will discover that the SBA requires proof of business hazard insurance. If you apply for a loan of over $25,000 the SBA wants to see coverage of at least 80% of the loan amount.

The good news is that you’re probably covered under your commercial property insurance. If, however, you run your business out of your home, your personal homeowners’ insurance doesn’t count for the SBA requirements. Actually, your homeowners insurance probably won’t cover your business if they think you’re claim is business related. Also, homeowners insurance probably isn’t enough to cover all of your business equipment such as printers, computers, and/or inventory.

How much does business hazard insurance cost?

Like commercial property insurance, certain things affect how much you’ll pay, such as:

- The age of the building

- The value of the property

- Square footage

- Construction of the building (wood, masonry, etc.)

- Value of the equipment

You’ll also have to decide if you want full replacement cost or actual cash value. Full replacement cost is more expensive and covers the amount you need to spend to replace whatever was damaged. Actual cash value gives you whatever the items were worth, taking age and depreciation into account.

Different insurance companies will have different quotes. If you want to get the cheapest quote, be sure to shop around with a few companies or with a digital broker like CoverWallet to compare several quotes:

Learn more at how much does business hazard insurance cost?

Who is business hazard insurance for?

If you live in an area prone to certain disasters, you’ll need to add hazard insurance onto your commercial property policy, or your business owners policy. Without this insurance, any losses you suffer due to the named disaster won’t be covered.

If you don’t live in such an area, commercial property insurance or a business owners policy should be adequate.

Learn more about why small businesses need business hazard insurance.

Last thoughts

It’s a good idea to check your commercial property insurance to find out what is covered, as they vary from company to company. If you’re not happy with your current policy, it pays to shop around.