Las Vegas has low business taxes, which is one reason why it’s a great place to own a small business. If you have even one employee in Nevada, you are required to have workers’ compensation insurance. Here’s everything you need to know about workers compensation insurance in Las Vegas.

- The 6 best workers comp insurance in Las Vegas, Nevada

- What does workers comp insurance cover?

- Workers compensation laws in Nevada

- What happens if I don’t have workers’ comp insurance in Las Vegas?

- How much does workers comp insurance cost in Las Vegas, Nevada?

- Factors affecting your workers’ compensation rates in Las Vegas, Nevada

- How to find cheap workers comp insurance in Las Vegas, Nevada?

The 6 best workers comp insurance in Las Vegas, Nevada

Hundreds of insurance companies offer workers comp insurance in Las Vegas, Nevada. We have researched more than 30 companies and here are our recommendations of the top 6 providers.

- CoverWallet: Best for comparing online quotes

- Pie: Best for easy process

- Liberty Mutual: Best for discounts

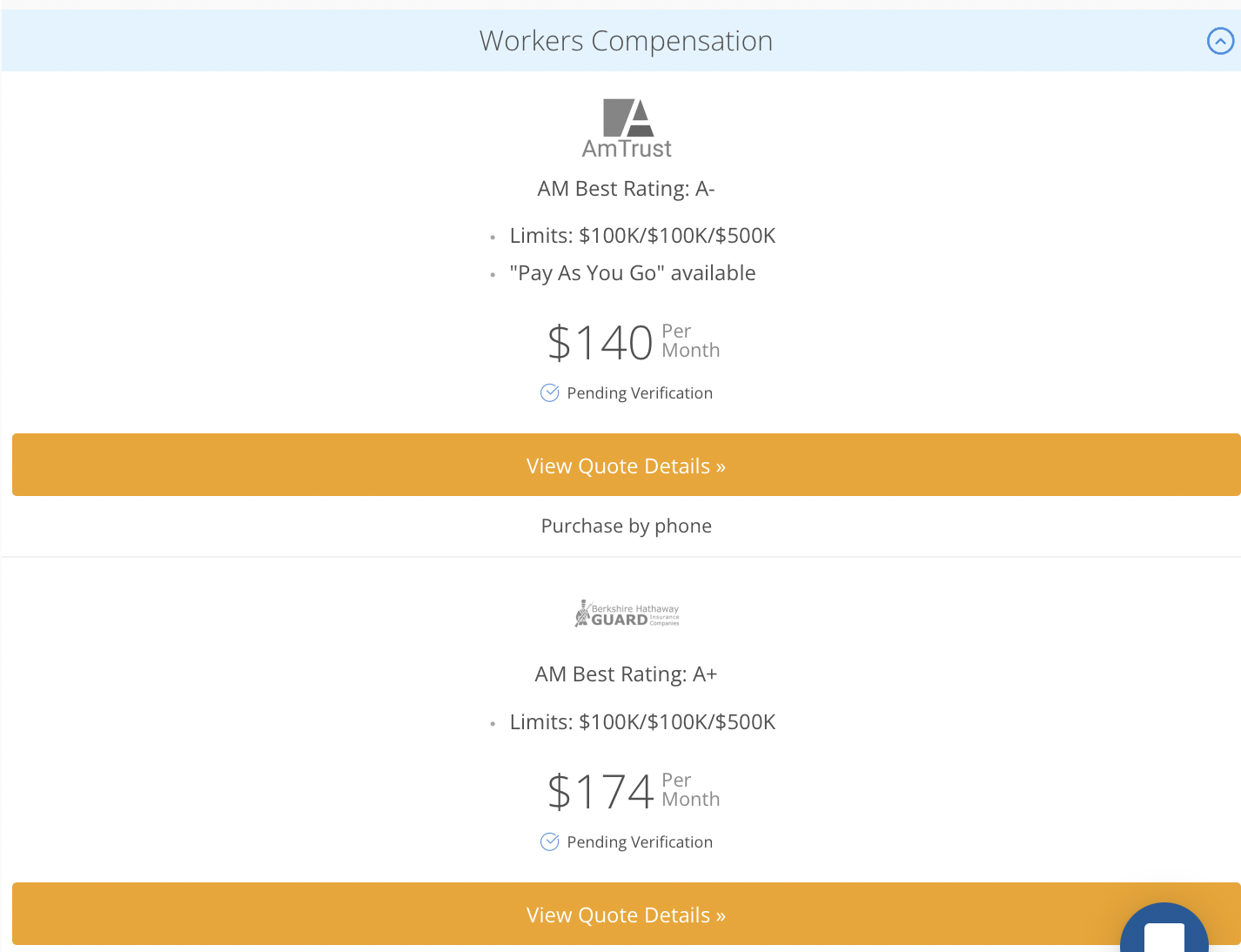

- AmTrust Financial: Best for 24/7 claims reporting

- Travelers: Best for larger businesses

- The Hartford: Best for pay-as-you-go insurance

CoverWallet: Best for comparing online quotes

CoverWallet is a digital broker of business insurance. They partner with many top insurance companies to provide you with several quotes after completing just one form. Completing the form takes about ten minutes. If you need other types of business insurance, you still fill out the one form and CoverWallet will provide you with quotes for multiple types of insurance. Then, you can manage all of your policies in the same “wallet” (on the same website).

Quotes are not always instant, though—sometimes it will give you a message that states they will email you your quotes within 24 hours.

These quotes are for an IT consulting business with 2 full-time employees and $500, 000 in revenue.

Pie: Best for easy process

Pie claims they can save you 30% on your workers’ compensation insurance. However, we couldn’t find anything even close to IT consulting when we tried to find our industry on the drop-down menu, and then they gave us this message:

You can also get other types of business insurance through Pie, including:

- Business Owner’s Policy

- Commercial Auto

- Error and Omissions

- General Liability

- Professional liability

- Small group health

Pie has good customer reviews—even on Trustpilot, they average 4.6 based on 352 reviews.

Liberty Mutual: Best for discounts

Liberty Mutual is the 6th largest property and casualty insurer in the world. They have a full range of business insurance, but if you try to get a quote, you either be told to contact an agent, or you will be referred to commercialinsurance.net. Commercialinsurance.net will take your information and then you will get a message saying someone will contact you to discuss your needs.

There is not a lot of information about rates on the Liberty Mutual website. They do offer many types of business insurance, for both small and large businesses. They cover many different industries. Once you’ve bought insurance, you can pay your bill and manage your policy online. There are also a great many discounts available.

AmTrust Financial: Best for 24/7 claims reporting

AmTrust Financial focuses on small businesses and workers’ compensation coverage. They also provide other types of business insurance, such as business owners’ policies, commercial property, cyber liability, umbrella, and more. They have an A+ rating with A.M. Best, so financially they have the strength to pay claims.

You can’t get a quote online, as AmTrust Financial prefers to work through agents. One thing to be aware of is that on Trustpilot, they have only been reviewed by eight people, and every single one of them gave AmTrust Financial one star. It’s true that people go to the internet to complain, but we still think you should be aware.

Also, AmTrust Financial doesn’t necessarily offer every type of policy in every area in the country, so be aware of that. You can get a 10% discount on your workers’ compensation insurance if you buy a business owner’s policy.

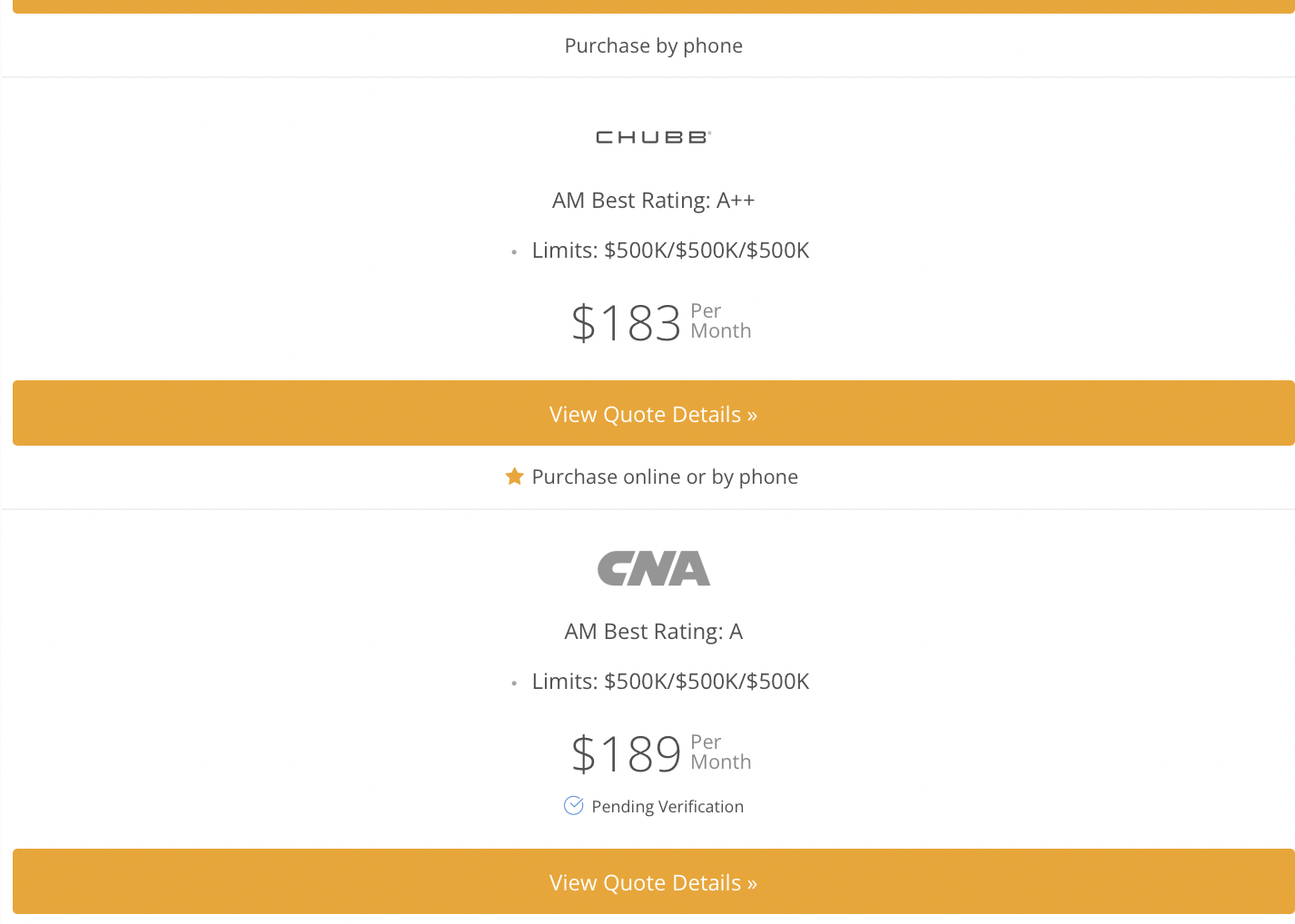

Travelers: Best for larger businesses

Travelers is the second-largest writer of business insurance in the United States, and the largest writer of workers’ compensation insurance.

What’s nice about Travelers workers compensation insurance is that every single person involved in the claim, from the injured employer to the employer to the care providers can access the online portal and find out what’s going on. They have more than 2,000 people handling workers’ compensation claims. Travelers might be a good fit for you if you have many employees and complex insurance needs. Small businesses should seek quotes elsewhere to see if you can get a better rate.

You can’t get a quote online: you’ll have to talk to an agent.

The Hartford: Best for pay-as-you-go insurance

According to The Hartford, they are number one in customer satisfaction. They do have a wide variety of business policies, including business interruption insurance, cyber insurance, commercial auto, and many other types of insurance. There are a lot of flexible options and customization available for specific industries. For workers’ compensation insurance, they offer pay-as-you-go insurance, which could save you money.

You can get a quote online, but to buy the insurance you’ll need to contact an agent. This quote is for an IT consulting firm with two full-time employees and $250,000 in annual payroll.

What does workers comp insurance cover?

Workers’ compensation insurance pays for lost wages, medical bills, and, in the worst-case scenario, funeral expenses for injured employees. It will also pay for rehabilitation and retraining, if an injury prevents someone from doing the same job. It also pays for disability benefits if the employee is unable to go back to work.

Workers compensation laws in Nevada

Any business that employs even one employee needs workers’ compensation insurance in Las Vegas (all of Nevada, actually). In addition, Nevada is a no-fault state when it comes to workers compensation benefits, so it doesn’t matter if the employee was at fault, or the employer was negligent. The only defense an employer would have is to prove the employee was not injured on the job.

There are only a few exceptions:

- Casual employees who worked less than 20 days or earned less than $500

- Employees brought to Nevada on a temporary basis that already have insurance from another state

- Employment covered by private disability and death benefit plans

- Theatrical performers

- Real estate brokers

- Domestic service providers

- Sole proprietors (you don’t need to buy workers’ compensation insurance for yourself)

- Employees who injure themselves intentionally

- Employees who injure someone else intentionally

- Employees under the influence of drugs or alcohol

Other than those few exceptions, you need workers’ compensation insurance, even if all your employees are minors, your own family, or part-time.

What happens if I don’t have workers’ comp insurance in Las Vegas?

If you fail to obtain workers’ compensation insurance, you can be fined up to $15,000. If you don’t pay or are unable to pay, your business could be closed until you obtain workers’ compensation insurance. Furthermore, if one of your employees does become injured, you will be responsible for all of their medical bills. Even if you settle the case, it will likely cost you more money than the cost of workers’ compensation insurance.

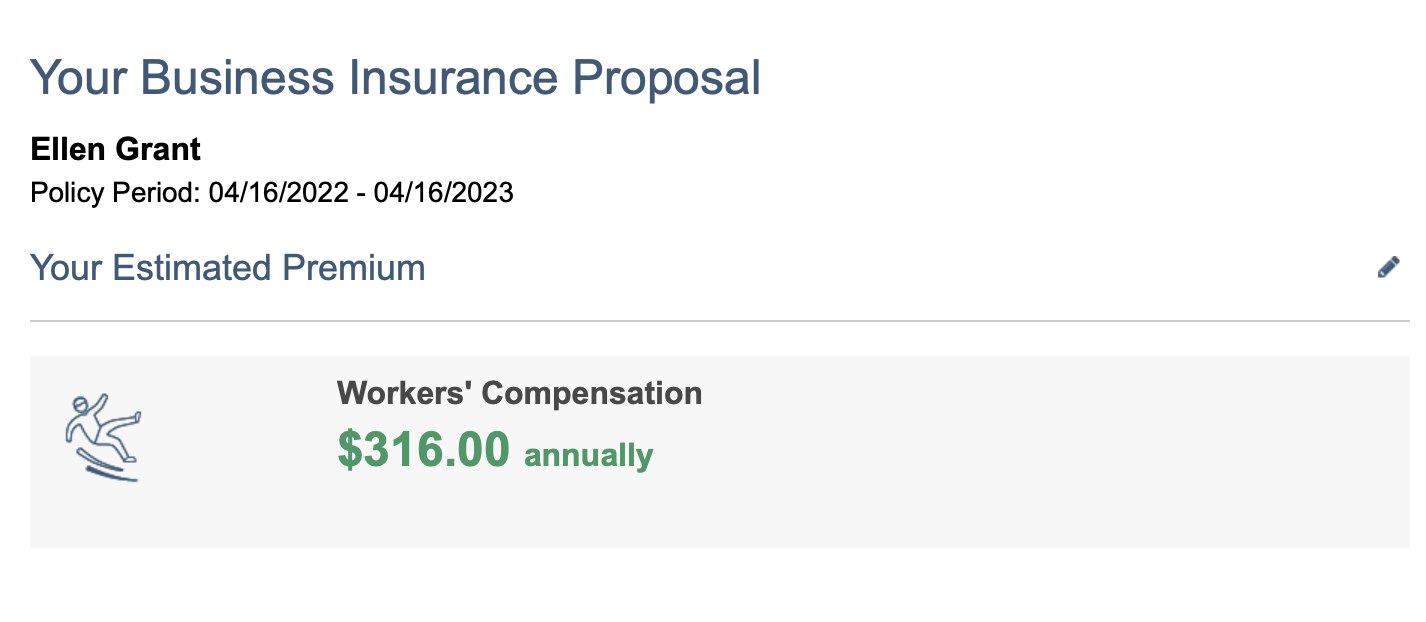

How much does workers comp insurance cost in Las Vegas, Nevada?

Nevada has some of the lowest workers’ compensation rates in the country, with employers paying an average of 32% less than most other states.

The average cost of workers’ compensation insurance is $1.31 per $100 of payroll. That’s just an average, though. Your rate will vary by things like:

- Type of business you own

- Level of risk

- Prior experience

- Claims history

If you’re interested in paying less for workers compensation, you should make your workplace as safe as possible.

Be sure to shop around with a few companies or work with a broker like CoverWallet or commercialinsurance.net to compare several quotes to find the cheapest one for your company.

Learn more about the cost of workers comp insurance

Factors affecting your workers’ compensation rates

The average cost of workers’ compensation insurance is $1.31 per $100 of payroll. That’s just an average, though. Your rate will vary by things like:

- Type of business you own

- Level of risk

- Prior experience

- Claims history

If you’re the sort of person who likes to crunch numbers, you can play with this formula:

Class code x experience modification rate x payroll = premium

So, first of all, what is a workers’ compensation class code? Class codes are what the insurance industry invented to classify workers by their level of risk. They assign codes to every possible type of job based on how likely it is that such an employee will become injured. Office workers, for example, are pretty unlikely to injure themselves at work (not to say it can’t happen), whereas construction workers have a much higher risk level.

Most states, including Nevada, use the WC codes set by the National Council on Compensation Insurance, or the NCCI. Some states prefer to use their own codes. If you’re curious, you can find the class codes here.

The experience modification rate is the only part of workers’ compensation cost that you can do anything about. It’s based on your company’s history of injuries and the chances of future injuries. What if this is your first year in business and you have no history of workplace injuries? Business won’t have an experience modification rate for the first few years. In this case, you’ll pay the average rate for your industry.

Experience modification rates range from 0.75 to 1.25. If you have the same frequency of workplace injuries as others in your industry, your EMR is 1.0. If you have fewer than average incidences of employee injuries, you get as low as 0.75 and pay less money. If you have a history of employee injuries, you’ll earn a rating of up to 1.25 and pay more in premiums.

The last factor is payroll. The more employees you have, the more you’ll pay for workers compensation insurance. More employees = more opportunities for one of them to suffer a workplace injury.

How to find cheap workers comp insurance in Las Vegas, Nevada?

Workers’ compensation insurance rates in Nevada are mostly set by the state, but there are a few things you can do to save money.

Have a documented safety plan in place: Post it where employees can see it, and make sure it’s followed. A written safety plan is imperative in promoting workplace safety.

Have a return-to-work program: Accidents happen but try to get your employee back to work as quickly as possible, without being sociopathic about it. Follow up with injured employees and wrap up claims quickly.

Make sure you’re using the correct class codes: Mis-classifying an employee can cost you hundreds, even thousands of dollars. Make sure you’re using the right codes.

Shop around: The rates are set by the state, but insurance companies might vary in what EMR they assign you and what codes they use. Also, some insurance companies are able to offer discounts.

Consider pay-as-you-go: Workers compensation insurance is based on payroll, but if you use a pay-as-you-go system, your rate is based on your actual payroll instead of an estimate. This could save you money since employees might leave or get fired, or you might cut hours to adapt to a slower period.

Learn more at the cheapest workers comp insurance companies

How does workers comp insurance differ from general liability insurance?

Although it is true that general liability insurance covers bodily injuries, it covers them for customers and vendors only—in other words, third parties. Your employees need to be covered by workers’ compensation insurance to provide them with medical payments, lost wages and possible rehabilitation.

Learn more at the best general liability insurance companies and the cheapest general liability insurance companies

Last thoughts

Las Vegas is a great place to run a business, but don’t gamble by not having workers’ compensation insurance. Shop around and have a good safety plan in place and hopefully you’ll never have to file a claim.