Wisconsin pioneered the Workmen’s Compensation Act; a law that provided workers with coverage for medical expenses and lost wages while also protecting businesses from lawsuits. Prior to 1911, a worker’s only option after an injury on the job was to seek medical attention, and he could only seek compensation for lost wages by suing his employer. Before this period, many attempts had been made in 1898, 1902, 1908, and 1909 to pass the laws for workers’ compensation. All these attempts failed as they were struck out in court as unconstitutional. However, in 1911, Wisconsin become the first state to pass a comprehensive workers compensation law that survived a court challenge. Ever since 1911, the laws of Wisconsin require that employers provide compensation insurance for their workers. In this article, we will explain all that you need to know as regards workers’ compensation insurance.

- The 6 best workers compensation insurance companies in Wisconsin

- What is workers’ compensation insurance?

- How does workers compensation law work in Wisconsin?

- Who needs workers’ compensation insurance in Wisconsin?

- What does the Wisconsin workers’ compensation insurance cover?

- Who is exempt from Wisconsin workers’ compensation insurance?

- How much does workers’ comp insurance cost in Wisconsin?

- How to find cheap workers comp insurance in Wisconsin?

The 6 best workers compensation insurance companies in Wisconsin

After detailed research and review of the best insurance companies that provide workers’ compensation insurance in Wisconsin, we found 6 of the best that are worth your time and consideration. Here is our list of the top 6 providers:

- CoverWallet: Best for comparing offers across multiple carriers

- Huckleberry: Best for ease of use

- Cerity: Best for Affordable offers

- Travelers: Best company for public entities

- Nationwide: Best for construction companies

- Employers: Best in terms of experience

CoverWallet: Best for small businesses in Wisconsin that want to compare several quotes online from multiple carriers

CoverWallet is a small business-focused online insurance broker. As a broker, CoverWallet does not offer any insurance policies instead, it obtains quotes from a variety of workers’ compensation insurance providers for you to compare. The online application is simple to complete and frequently yields multiple offers.

CoverWallet will match you with one of its insurance partners after you submit your information. Depending on your business and other factors, the website might recommend a Pay-as-you-go premium, rather than upfront payments. If you are pleased with your quote, you can contact CoverWallet to activate your policy and begin receiving coverage right away.

Sometimes not all users get an instant quote. The website may require that you call and speak with a representative to obtain an insurance quote.

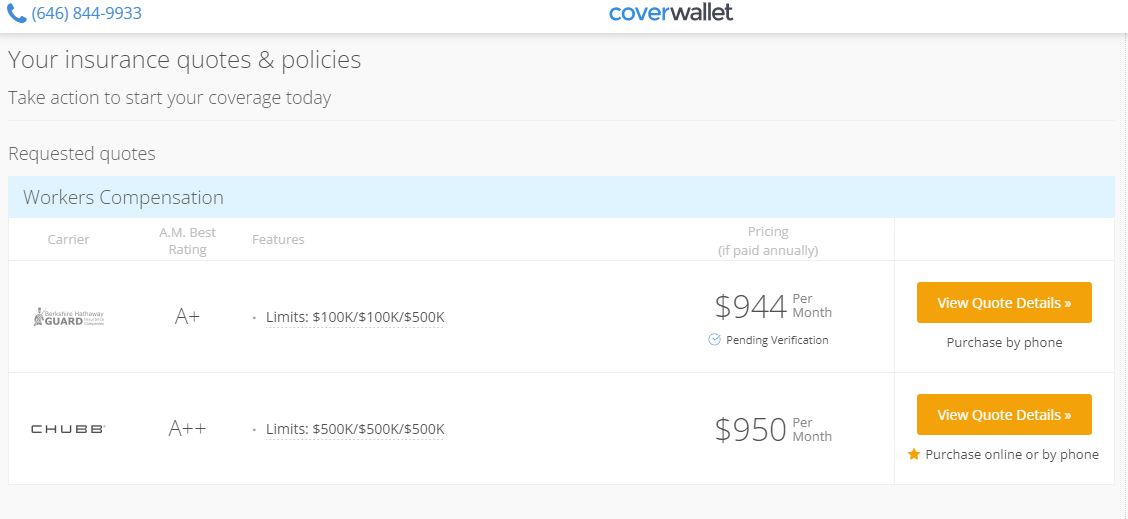

Here is a sample quote generated from Coverwallet for a hypothetical commercial cleaning company in Brookfield, WI with 4 full-time employees, an annual payroll of $260,000, and annual revenue of $500,000.

As you can see, the two quotes we received from Guard and Chubb via CoverWallet are almost the same for this company. However, the quotes for your own business might be different, so be sure to get and compare quotes for your company

Huckleberry: Best for ease of use

If you are looking for a carrier that makes it easy to generate quotes, Huckleberry is your best bet. Huckleberry is a relatively new online insurer that offers the best of worker’s comp to large and small businesses in Wisconsin.

The aim of the company since its inception has been to create a platform where companies can find fast insurance coverage options with ease. Interestingly, they have been able to achieve this since all their processes are done online 100%.

Huckleberry provides good work comp insurance to small and large business owners in Wisconsin state. The good thing is, when you buy a policy from them, it comes tailored to your needs. That way, you receive comprehensive workers’ compensation coverage that truly protects your interests as well as that of your employees. Finally, the company has good ratings amongst its online users.

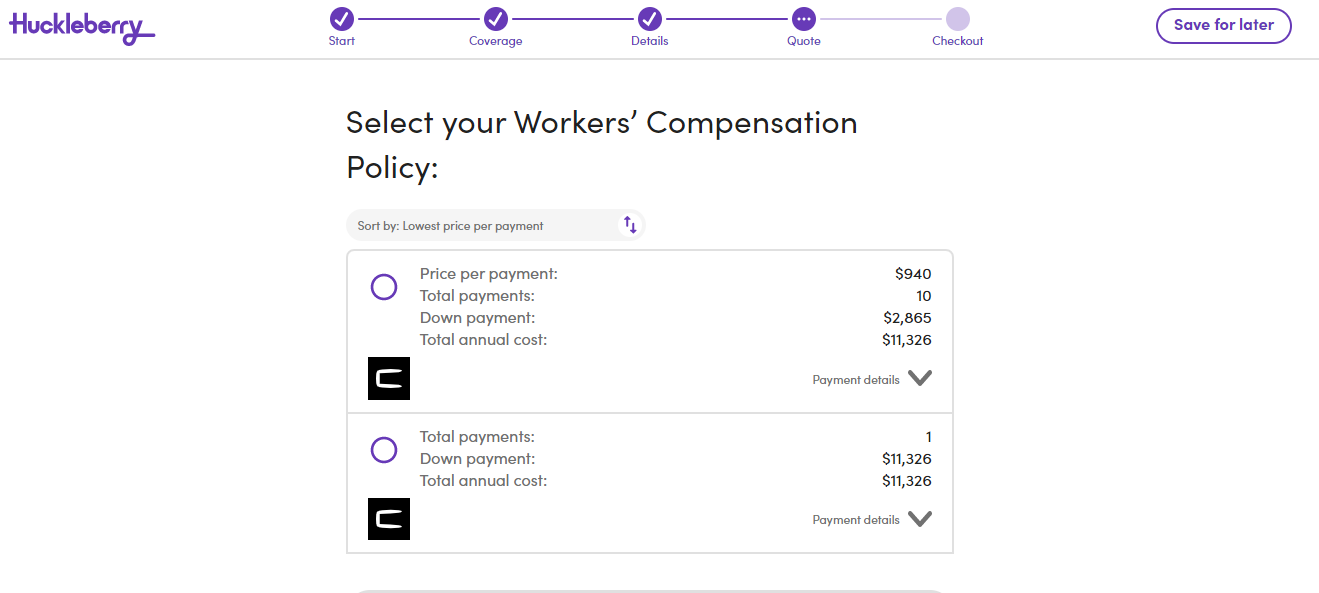

Here is a sample quote generated from Huckleberry for a hypothetical cleaning company in Brookfield, WI with 4 full-time employees, an annual payroll of $260,000, and annual revenue of $500,000.

Through Huckleberry, we only receive one quote from Chubb insurance. However, we have two options: pay monthly or pay annual for this quote.

Cerity: Best for affordable workers’ compensation in Wisconsin

Cerity is a specialized firm that offers workers compensation in Wisconsin. At the moment, the company does not provide any other type of insurance beside the workers’ comp. Even at that, it does its best to provide affordable and high-quality service. Policies start at $25 per month, which is less than most insurers charge.

The beauty of Cerity is in how fast they generate their quotes. Using artificial intelligence technology, you can generate your quotes on the website in minutes. And if for any reason you need help or the system cannot generate your quotes, a customer rep will call you to speak with you. Their customer rep team are experienced in workers comp and they will give you all the information you need. Finally, Cerity customers rate the company well across most trusted platforms.

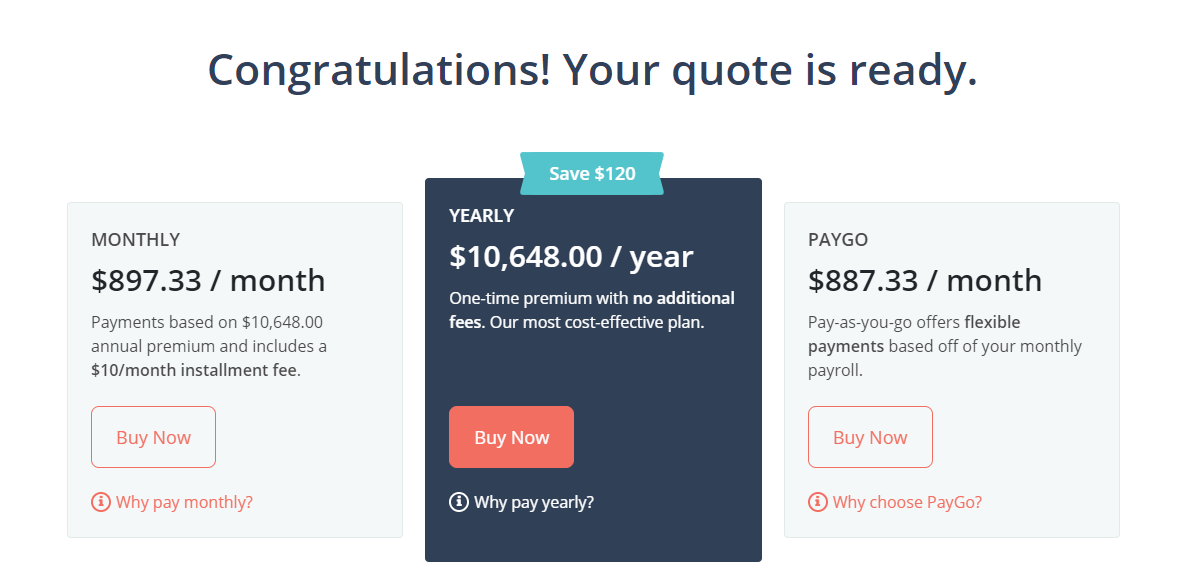

Here is a sample quote generated from Cerity for a hypothetical Commercial Janitorial company in Brookfield, WI with 4 full-time employees, an annual payroll of $250,000, and annual revenue of $500,000.

As you can see the quote from Cerity for the same company appears to be a bit cheaper than the quotes from Chubb and Guard, via CoverWallet and Huckleberry. However, you need to look into the coverage details and limits of these quotes to ensure you are comparing apples-to-apples. In our experience, when a quote may appear to be a bit cheaper, the coverage limits are also lower. So, be sure to study the quote carefully before making your final decision.

Travelers: Best for public entities

Travelers have a far-reaching reputation when it comes to worker’s compensation insurance in the US. In Wisconsin, they are also very popular as an ideal choice for local companies. The company focuses on the companies in the oil and gas industry, government organizations, and other small businesses. It is worthy to note that their expertise with public entities is second to none. That includes public entities like K-12 public schools, American Indian nations, municipalities and counties, transit authorities, and utilities.

Travelers are always there to protect your business in the case of any incident. But then, this insurer is more concerned with the health and safety of your workers and your business. Therefore, they organize training on accident prevention on regular basis. The training is to promote workplace safety and wellness culture in companies that they insure. Travelers insurers are rated A+ on BBB and A++ on AM. So, you can trust them with your company. Unfortunately, Travelers does not offer instant quotes on their website, to get a quote you have to speak with a representative.

Nationwide: Best for construction companies in Wisconsin

Speaking of large insurers in the United States, it would be a crime not to mention Nationwide. This company has been around since 1926 and today lives up to its name as it offers a comprehensive range of insurance products in almost all states in the US including Wisconsin.

Thanks to their experience and expertise in various industries, their workers’ comp insurance coverage fits rightly for most companies.

However, it offers construction and contracting businesses insurance options that can be bundled with workers’ compensation coverage, such as general liability insurance, professional liability, business auto, and contractor equipment insurance. This makes the offer more suited for construction companies.

Nationwide’s industry knowledge extends to risk management resources and services. Nationwide, for example, has excellent resources for businesses to evaluate their health and safety practices and work to reduce the risk of incidents that result in claims.

The Better Business Bureau has also accredited Nationwide with an A+ rating, indicating that they meet the BBB’s highest standards for fair business practices.

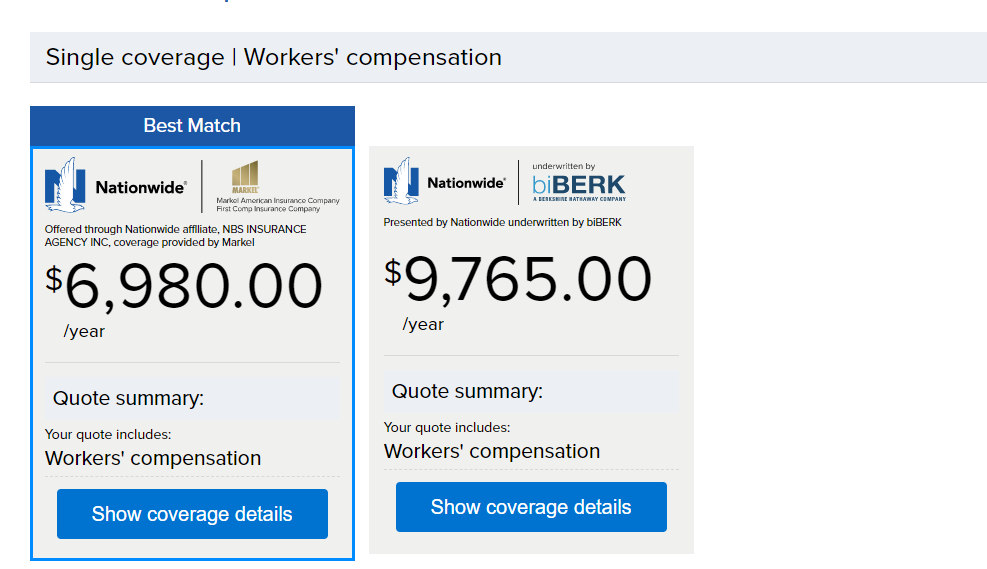

Here is a sample quote from Nationwide for an office cleaning company with 4 associates and an annual income of $500,000.

It is interesting to notice that Nationwide doesn’t underwrite workers compensation for this particular company, a commercial cleaning business. Instead, they are working with both Markel Insurance and biBERK to provide their customers with quotes. Essentially, Nationwide plays a role as an insurance broker in this case. And it is worth calling out that Markel offers the lowest quote for this hypothetical company, a commercial cleaning business based in Wisconsin. However, let’s be assured that the quotes for your own companies might not be the same from these carriers, so make sure you get several quotes to compare and select the best one for your business.

Employers: Best in terms of experience

Finally, Employers is a large insurer in the US that was founded in 1913, with more than a century of experience in the industry. After worker’s compensation was first legalized in the state, the insurance company was founded in Nevada under the name “Nevada Insurance Commission”. Their mission at the time was to bring affordable coverage for medical treatment and compensation of injured workers to the public. To date, the company has continued to provide worker’s compensation insurance to meet the needs of employees across the US. Their worker’s comp insurance in Wisconsin comes with side benefits like safety training and programs for loss prevention. The company also provides other risk management services to small businesses at affordable rates. Like with other companies, the carrier requires that prospective customers request a quote to get started. Finally, Employers is rated well by the BBB and the A.M. Best. Unfortunately, to get a quote from Employers, you have to speak with their representative. They do not offer instant quotes.

>>MORE: Top 10 Workers Comp Insurance Companies in the US by Market Share

>>MORE: The 10 Best Workers Comp Insurance Companies

What is workers’ compensation insurance?

Workers’ compensation insurance (workman’s comp, workers’ comp, or workers’ compensation insurance) is a special insurance coverage that pays for medical care, rehabilitation, and lost wages for injured or ill sick employers in Wisconsin. Workers’ compensation also covers the dependents of the employee in the event of death.

This insurance is a trade-off designed to benefit both the employee and the employer, as well as society as a whole. Workers’ compensation insurance is critical for businesses because it reduces a company’s liability, financial, and operational risk by lowering the likelihood of employee lawsuits for medical care, lost wages, and even death benefits.

The employee on the other hand benefits from the coverage if he or she is unable to work due to illness or injury. Finally, keeping workers’ compensation cases out of courtrooms benefits society by freeing up the capacity for legal disputes that cannot be resolved outside of court.

How does workers compensation law work in Wisconsin?

The Division of Workers’ Compensation of the Wisconsin Department of Workforce Development monitors and ensures that eligible workers in Wisconsin receive their Workers’ compensation benefits from insurers or self-insured employers as required by law. By so doing, the department encourages rehabilitation and reemployment for injured workers, and also promotes the reduction of work-related injuries, illness, and death.

Wisconsin provides all reasonable and necessary medical treatment, wage loss benefits, and vocational rehabilitation and retraining to injured workers. Injured workers may seek medical treatment from any doctor of their choice on any injury including mental injuries. To determine whether a mental injury is covered by workers’ compensation, the department decides to use its “extraordinary stress” standard. In other words, if you require treatment as a result of normal work activity, such as a work evaluation, the injury is unlikely to qualify for benefits.

Who needs to have workers’ compensation insurance in Wisconsin?

According to Wisconsin’s Department of Workforce Development, both private and public employers must have a workers’ compensation policy in place. Ideally, once you have a minimum of three employees, you qualify for the insurance policy. Note that the laws define employees as anyone who is under contract to perform services for your company. These include full-time workers, part-time employees and corporate officers.

Additionally, business owners must obtain workers’ compensation if they:

- Hire at least one full-time or part-time employee who earns a total of $500 in wages in one calendar quarter. Such insurance must be in place by the 10th day of the first month of the following quarter.

- Employ at least six workers on a farm on the same day for 20 or more days in a calendar year. In such a situation, insurance must be in place by the tenth day following the twentieth day.

Sole proprietors and partnerships with no employees, as well as limited liability companies (LLC) with only members, are exempt from carrying workers’ compensation in n Wisconsin. However, some business owners decide that workers’ compensation is necessary based on their discretion but then, it is not required by law.

The interesting part is, once you have been required to obtain workers’ compensation as an employer, the laws of the state demand that you continue for at least 1 year. Even if you decide to fire all but one part-time employee, you will still have to continue to cover the workers’ compensation insurance for that employee for the rest of the calendar year and the following calendar year. When you decide to start hiring again, you must have a policy in place to cover for every single employee that you offer jobs.

What does the Wisconsin workers’ compensation insurance cover?

Worker’s compensation is divided into four benefit categories. The four types are as follows:

Benefits for wage replacement

This began in January 2019 and it typically amounts to two-thirds of the worker’s average weekly wage up to $1,016 per week. Wage replacement benefits are not taxed, so they help a worker’s take-home pay. After missing a few days of work due to injury or illness, employees begin collecting.

Permanent partial disability benefits

This benefit compensates an employee who has been diagnosed with a permanent disability but whose disability does not eliminate their ability to work. Carpal tunnel syndrome is a common type of permanent partial disability. The amount of the benefit is determined by the part of the body or the severity of the disability.

Vocational rehabilitation benefits

These benefits assist workers who are unable to return to work due to an injury. Counseling, job retraining, job placement, job development, and vocational monitoring assist workers in finding new jobs within the same company or in finding new employment entirely.

Medical benefits

Injured workers are entitled to all medical care that is necessary and reasonable. Employees select their doctors.

Who is exempt from workers’ compensation insurance in Wisconsin?

Almost every Wisconsin employer is required to provide insurance to their employees. However, there are a few exceptions allowed by state law, depending on the type of work the employee performs.

Employees excluded include the following:

- Domestic servants, such as nannies, cooks, maintenance workers, and gardeners;

- Volunteers, especially those who receive less than $10 in cash or items per week;

- Farmer workers who do not meet the above criteria.

- Religious sect members

- Real estate brokers, salespersons, and agents

- Native American tribal enterprise employees including those that work in casinos. The employees might however need covering if such tribe decides to waive their sovereign immunity and offer workers compensation insurance. But then, it would be voluntarily.

- Workers who are already covered by federal workers’ compensation programs are also excluded. This includes people working in the military, postal service, railroads, etc.

>>MORE: Who Is Exempted from Workers Comp Insurance in the Top 10 States?

How much does workers’ comp insurance cost in Wisconsin?

Wisconsin is a self-governing state and as such, the state does not use the National Council on Compensation Insurance classification system. Instead, the Department of Workforce Development n Wisconsin state determines employee classification codes, base rates, and experience modifiers.

According to recent data from the National Association of Social Insurance, Wisconsin business owners pay an average of $1.58 per $100 of payroll for workers’ compensation each year for basic coverage. Premiums, however, may vary because it is usually are based on your payroll, the risks your employees face, and your claims history in comparison to similar businesses.

However, you can calculate your rate for premium using this formula:

Payroll / $100 x Classification Code Rate x Experience Modification Rating

In Wisconsin, your primary operations determine your class code. For instance, you own a landscaping company, the class code for landscaping services is 0042. You might have some employees whose duties may not include landscaping, but then they will all fall under the 0042 classification for the calculation they will all be insured at $8.89 per $100 of payroll. This base rate is then multiplied by an experience modification rating, which is a number calculated by your insurer to represent how safe it believes your business is.

Learn more how much workers comp insurance cost and how to calculate it.

How to find cheap workers comp insurance in Wisconsin?

Businesses in Wisconsin are able to choose their own workers’ comp insurance provider. You owe it to yourself to compare coverage and costs from several insurers. You can select one that offers you the coverage you need at the best possible cost.

The most important thing you can do to save money is make sure you’re using the right class code for every employee. Some class codes have much higher rates than others. Also remember to update the codes if an employee is promoted or changed jobs within your company.

You can also save money by providing a safe workspace for employees, so they won’t get injured. Make sure you establish the workplace safety standards and best practices for your company. Some insurance companies will provide a risk management assessment, which is worth taking advantage of.

You could also consider pay-as-you-go workers compensation insurance, which might save you money. It’s based on your actual payroll, rather than estimated payroll. So, if three people quit one month, your rate will be lower for that month.