According to the Small Business Administration, Washington has over 630,000 small businesses. These small businesses together employ more than half of the state’s workforce. If you own one of these businesses, you should consider several types of business insurance to protect yourself from various work-related incidents.

But then, getting business insurance is not as difficult as you imagine. Keep reading as we show you what it means. We will also show you the best places where you can buy your policies without stress.

- The 7 best small business insurance companies in Washington State

- Washington state business insurance requirements

- Why do I need business insurance in Washington State?

- What kinds of business insurance do I need in Washington State?

- How much does small business insurance cost in Washington State?

- What affects small business insurance cost in Washington State?

- How can I find cheap small business insurance in Washington State?

The 7 best small business insurance companies in Washington State

- CoverWallet: Best for comparing multiple insurance quotes

- Travelers: Best for general liability insurance

- Liberty Mutual: Best for Business Owners’ Policy

- The Hartford: Best for comprehensive coverage

- State Farm: Best for commercial liability coverage

- Progressive: Best for commercial auto insurance

- Pie: Best for workers comp insurance

CoverWallet: Best for comparing multiple insurance quotes

If you require multiple types of business insurance, CoverWallet provides a comprehensive list of insurance options. CoverWallet is best suited for businesses that require all types of business insurance but do not want to deal with the hassle of applying to multiple companies.

CoverWallet is a good option for many businesses because it has access to many insurers. CoverWallet, on the other hand, is not a lender; instead, they act as a middleman, connecting you with multiple insurance companies. They work hard to get you approved for whatever type of insurance your company requires and access to low rates.

Pros

- Allows you to compare several quotes at once

- Can save you some cost with low rates

Cons

- Can only offer policies from its partners

Travelers: Best for general liability insurance

Travelers is yet another big name in the world of commercial insurance. The company serves different companies in finance, manufacturing, retail, technology, and other industries.

This insurance company has been in business for over 160 years.

Travelers offer a wide range of coverage options in addition to industry-specific policies. However, Travelers’ general liability insurance policies stand out the most of all their policies. Over 500,000 businesses trust travelers for their excellent general liability insurance.

Pros

- Has an extensive library for risk management resources

- You can check the website to monitor claims

Cons

- They do not offer online quotes

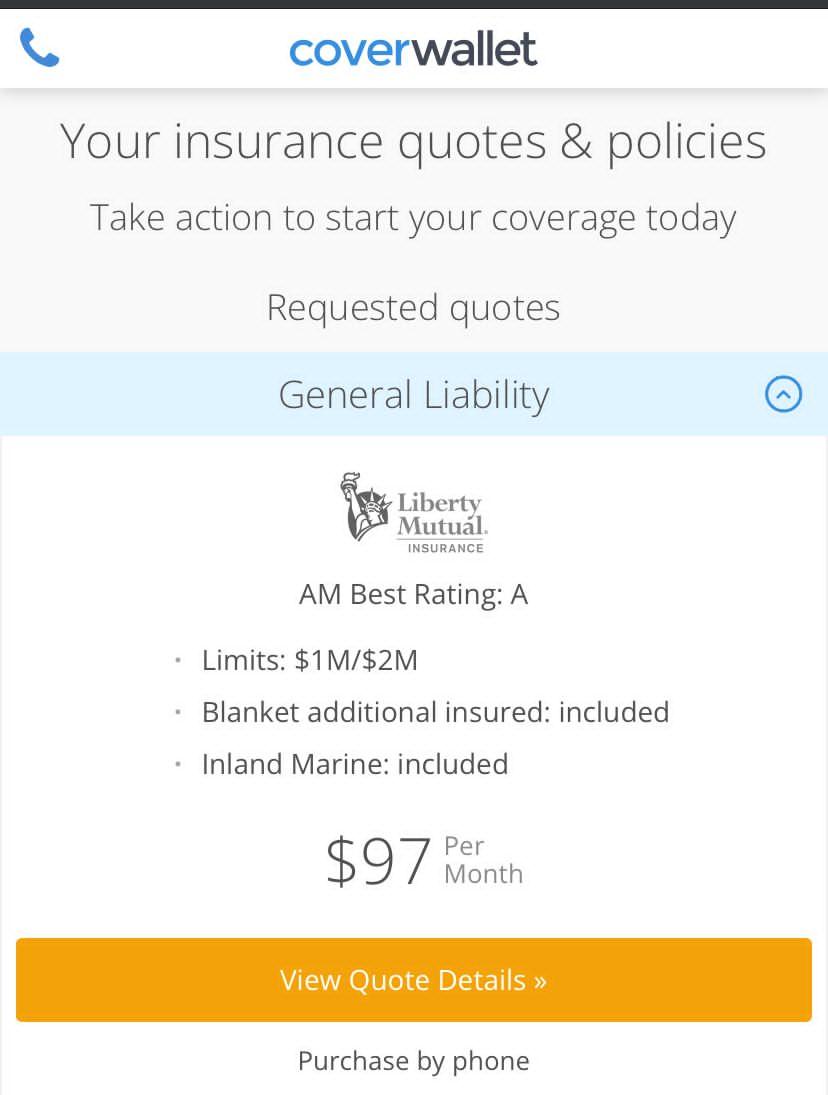

Liberty Mutual: Best for Business Owners’ Policy (BOP)

Liberty Mutual is in a unique position to assist many business owners in any industry.

Liberty Mutual provides commercial insurance through independent agents all over the country. Commercial auto, equipment breakdown, inland marine, umbrella coverage, and workers’ compensation are among the coverage options available.

Plus, they have 11 industry-specific solutions for businesses in construction, public entities, finance, healthcare, real estate, and wholesale. Through its nationwide contractor referral network, Liberty Mutual also advertises 24-hour claims assistance.

Pros:

- You can file claims on their websites or with their mobile app

- They have a 24-hours claims assistance

- They also have support services for crisis management

Cons:

- You can only get policies from their agents

The Hartford: Best for comprehensive policies

The Hartford distinguishes itself through its comprehensive Business Owner’s Policy (BOP). The policy is a three-in-one policy that combines general business liability insurance, business property insurance, and business income insurance.

The BOP also protects against income loss caused by fires, damaging winds or burglaries, bodily injury or property damage, and personal and advertising injury.

Pros

- Provides discount for bundling policies

- Online quotes for 51 professions across 24 industries

Cons

- Can’t file business claims on the app

- No live chat support

StateFarm – Best for commercial liability coverage

You can supplement your commercial liability coverage with StateFarm’s Commercial Liability Umbrella Policy. The company also offers professional liability, errors, omissions, employment practices liability insurance (EPLI), etc.

Pros

- It covers over 300 professions

- Offers highly customizable insurance policies

- Live chat assistance

Cons

- Claims are filed over the phone rather than online.

Progressive: Best for commercial auto insurance:

Progressive has a long history of auto insurance. This experience puts it ahead of other companies for commercial auto insurance.

They also have general liability, professional liability, and BOP insurance. The only downside is their commercial auto insurance might be a little expensive.

Pros

- You get a refund if you cancel your policy

- They have live chat support

Cons

- Some of their policies are offered in partnership with Hiscox

Pie: Best for workers compensation insurance

Pie is a relatively new company established in 2018. Their primary focus is worker’s comp, even though they offer other policies.

The company started as part of what is called insuretech companies. These tech firms aim to make insurance purchase an online process that is easy and fast.

Unfortunately, you cannot but workers comp from them because Washington does not allow you to buy from private insurers.

Pros

- Fast online quotes

- Suitable educational materials on their website

Cons

- Relatively new in the industry

- They only offer workers’ comp on their own. Other policies are by other carriers.

What is business insurance?

Business insurance is a broad name that refers to several coverages required to protect businesses. These coverages help business owners protect their businesses against damages regarding property, legal claims, lost wages, etc.

Different companies offer different coverage under this policy. The most common types include the following coverages:

- Commercial General Liability

- Commercial Property Insurance

- Income Interruption Insurance

- Workers Compensation

- Income Interruption Insurance

Washington state business insurance requirements

As a business owner in Washington state, the state laws do not require you to have business insurance. However, there are some coverages under the broad policy that you must carry. The following are some of the policies that you must have in Washington.

Workers compensation insurance

First, like in most states of the US, you need workers’ compensation insurance to do business in Washington. However, Washington is one of the few states in the US where you cannot buy workers’ compensation from private insurers.

To buy the policy, you will need to buy from the state’s insurance funds, or you can opt for self-insurance.

Commercial auto insurance

In addition to workers comp, you might need commercial auto insurance if your business owns a vehicle. The state of Washington requires that business owned vehicles carry minimum auto liability insurance as follows:

- Property damage liability of $10,000 per accident

- Bodily injury liability of $25,000 per person

- Bodily injury liability of $50,000 per accident

Trucking companies, however, may require additional coverages depending on their trucks and what they do.

Why do I need business insurance in Washington State?

As a business owner, your main job would be to reduce costs. So, you might ask if business insurance is necessary.

In simple terms, yes, you need business insurance in Washington. Different perils happen in Washington that can affect businesses. For instance, your employees may get injured on the job, leaving you with medical bills that can cost you thousands of dollars.

To avoid these issues and many more, you must get insurance for your small business.

What kinds of business insurance do I need in Washington State?

For adequate protection, your business requires various types of small business insurance. It would help if you discussed your needs with a professional when creating a policy to ensure you are getting comprehensive coverage.

That said, here are some of the most common types of coverage that small businesses benefit from:

Commercial general liability insurance

General liability insurance is one of the broadest types of commercial insurance and covers some of the most common risks businesses face. This includes bodily injury and property damage claims. Learn more at the best general liability insurance companies.

Commercial property insurance

Commercial property insurance is misunderstood by many. This policy isn’t just for companies with buildings or land, unlike what you think. It can also be written to cover damages to fixtures, inventory, and equipment, among other things. Learn more at the best commercial property insurance companies.

Income interruption insurance

This policy covers you for any lost income and operating expenses if your business cannot operate due to property damage caused by fire, vandalism, or other covered perils. Learn more at the best income interruption insurance companies.

Professional liability insurance

Professional liability policy, also known as errors and omissions (E&O) insurance, protects skilled professionals from claims of mistakes, negligence, or failure to deliver services as desired. Learn more at the best professional liability insurance companies

Workers compensation insurance

Workers comp insurance is compulsory in Washington state and some other US states. As long as you have employees in Washington, it would be best if you had this policy. It covers lost wages and medical bills when your employees get injured while working at their job. Learn more the best workers comp insurance companies.

Is there an easy way to get business insurance coverage in Washington?

You can do that by getting a Business Owner’s Policy (BOP). Considering the many policies under the business policy, insurers created the BOP.

It is a policy that brings together a collection of property and liability coverages.

In most cases, liability and property coverage will come with your BOP at the very least. In addition, you will need workers’ compensation insurance which is compulsory in Washington.

When you apply for coverage online, the insurer will most likely recommend additional coverages you need. To be clear, you can also visit business insurance agents for help.

Learn more at the best BOP insurance companies.

How much does small business insurance cost in Washington State?

Commercial insurance can be affordable for small business owners in Washington State. Statistics show that businesses in the state pay about $80 per month for business insurance, or $960 a year.

This is just the average, the insurance quotes for your business will be very different. Be sure to shop around with a few companies or with a digital broker like CoverWallet, Simple Business, Policy Sweet, or commercialinsurance.net to compare several quotes to find the cheapest one for your business.

What affects small business insurance cost in Washington State?

The type of business and its risks are two factors that influence the cost. Other factors that affect the cost include:

- Company operations and location

- Total number of employees

- The various types of business insurance that have been purchased

- Policy limits and additional coverage options

Location

Rates for commercial insurance vary depending on your location in Washington State. People that live in more populated areas have to pay more because the chances of accidents are more.

So, a cafe owner in Seattle will likely pay more than a cafe owner in Walla Walla, even if the size of their business is the same.

Coverage limits and deductibles

The higher coverage limits and the lower deductibles of your policy are, the more expensive the business insurance is. A $1M/$3M policy is more expensive than a $100K/$300K policy. Similarly, a policy with $100 deductible is more expensive than one with $500 deductible. Make sure you should the right coverage limits and the right deductible amount for your policy to get the best price.

Risk exposure

Depending on your industry, your commercial insurance costs may be high or low. For instance, a software engineer might pay less for business insurance than a handyman because his profession carries fewer risks.

Business size

The bigger your business is, the more expensive your business insurance cost will be. Bigger businesses have more and bigger locations and more customers, which increases the likelihood for an accident to happen.

Business stability

The number of years you’ve been in business and your demonstrated financial stability can help you save money on commercial insurance. Insurers believe newer companies are risky because they do not have the experience to avoid some critical mistakes.

Claims history

Having a history of liability claims will generally result in higher business insurance premiums.

How can I find the cheap small business insurance in Washington State?

The following are some ideas that might help you lower the cost of your business insurance in Washington:

Compare multiple quotes

Different carriers have their way of measuring risk. That means some companies might see you as less risky even when others think you are too risky to insure. In such cases, you might find cheaper options. So before you pay, ensure you seek the opinion of other companies and pick the one that offers the best value at the least possible price.

Check the coverages

You must understand that you pay more for higher coverage. So, you should check to see that you are paying for just the protection you need.

Buy policies in bundles

If you would be buying multiple policies, consider buying from an insurer. Most insurers have discounts for customers that buy multiple policies at once.

Commit to safety

Commitment to safety reduces the possibility of mishaps. This is one of those things insurers use in calculating your premium. So, if you want to lower costs, consider getting a safety plan.