Small businesses in Kansas are sued more than their counterparts in other states. The following are some statistics about the lawsuits against small businesses in Kansas:

- In 2012, there were 5,521 small business lawsuits filed in Kansas.

- This is more than twice the number of small business lawsuits that were filed in California, which had the second highest number of filings.

- The most common type of lawsuit against a small business in Kansas is for personal injury.

There are several reasons why small businesses in Kansas should have general liability insurance. First, the odds of being sued are higher in Kansas than in other states. Second, the cost of defending a lawsuit can be prohibitively expensive for a small business. Third, even if a small business is victorious in court, it may still have to pay damages to the plaintiff. General liability insurance can help protect a small business from these risks.

This article recommends the 5 best general liability insurance companies in Kansas and discusses what you need to know to get the right general liability coverage for your business in Kansas.

- 5 best general liability insurance companies in Kansas

- General liability insurance quotes online for small businesses in Kansas

- General liability insurance requirements in Kansas

- What does general liability insurance cover in Kansas?

- How much does general liability insurance cost in Kansas?

- How to find cheap general liability insurance in Kansas

5 best general liability insurance companies in Kansas

Many companies offer general liability insurance for small businesses in Kansas. After intensive research, we recommend the following 5 best providers:

- Simply Business: Best broker to work with to find cheap coverage

- NEXT: Best digital carrier offering low-cost general liability coverage

- CoverWallet: Best for comparing several quotes online from top companies

- Hiscox: Best for a bundled policy (general liability and professional liability)

- Smart Financial: Best option if you prefer working with an experienced agent

Simply Business: Best broker to work with to find cheap coverage

Simply Business is a small business insurance brokerage. They work with many carriers with a focus on helping you find low-cost coverage that your business may need, including general liability insurance. They specialize in finding good low-cost carriers to partner with. They vet the carriers that they work with to ensure that all of them have excellent financial ratings.

Pros:

- Easy to get and compare several quotes online

- Able to get quotes from A-rated carriers which you may not be aware of

- Knowledgeable agents that are available to help you along the process

- Good consumer satisfaction rating on trustpilot

Cons:

- Quotes online are available for general liability and professional liability only

- Have to file a claim directly with the carriers

NEXT: Best digital carrier offering low-cost general liability coverage

NEXT is a 100% digital carrier. They are new, founded in 2016, specializing in providing general liability insurance online for contractors and other local businesses. Working with NEXT is fast and easy. You can do everything completely online.

Pros:

- Excellent digital experience from quoting, buying a policy, and managing a policy. Everything is fast and easy online

- Reasonable rates, especially for contractors

- Backed in A+ reinsurer, Munich Re

Cons:

- Limited specialty insurance types

- Limited customer service support during the buying process

CoverWallet: Best for comparing several quotes online from top companies

CoverWallet is another brokerage specializing in small business insurance. They work with a lot of top-rated carriers such as Chubb, Liberty Mutual, or Hiscox. They make it super easy for small businesses to compare several quotes from these top-rated carriers online.

Pros:

- Get multiple quotes by filling out one form

- Manage all your policies in one “wallet”

- Wide variety of coverage types available

Cons:

- They don’t write policies: they are a broker

- Quotes are not always instant and in certain circumstances, you have to call

Hiscox: Best provider for bundled policy (general liability and professional liability)

Hiscox is a very well-known small business insurer. They actually pioneered offering small business insurance online and have been around for more than 100 years. They have a good reputation and excellent financial strength. You can easily get a quote and buy a policy online within 10 minutes.

Pros:

- A solid carrier with an excellent reputation and financial strength

- Have been around for more than 100 years

- Specialize in general liability and professional liability coverage

Cons:

- Rates can be higher than other options

- Their policies may not be available to some niche industries like contractors or handyman

Smart Financial: Best option to work with an experienced agent

Smart Financial is another insurance brokerage. However, unlike Simply Business and CoverWallet who believe in a digital insurance buying experience for small businesses, Smart Financial believes that small businesses should work with experienced agents to find the right coverage for their businesses at a reasonable rate.

Pros:

- An extensive network of knowledgeable and experienced agents

- Provide coverage for small businesses of all sizes and in all industries

- If you are new to buying insurance for your small business, working with an experienced agent is a good idea

Cons:

- No mobile app

- You have to work with an agent on the phone

General liability insurance quotes online for Kansas small businesses

To illustrate how easy and simple getting online general liability insurance quotes for Kansas small businesses is like, we got quotes from 3 companies: InsurePro, Simply Business, and NEXT. Below are three quotes for a small accounting firm with 5 full-time employees, $400,000 in payroll and $800,000 in revenue:

InsurePro general liability insurance quotes online:

Below is the quote from InsurePro. InsurePro also has the cheapest quote for the accounting firm located in Kansas.

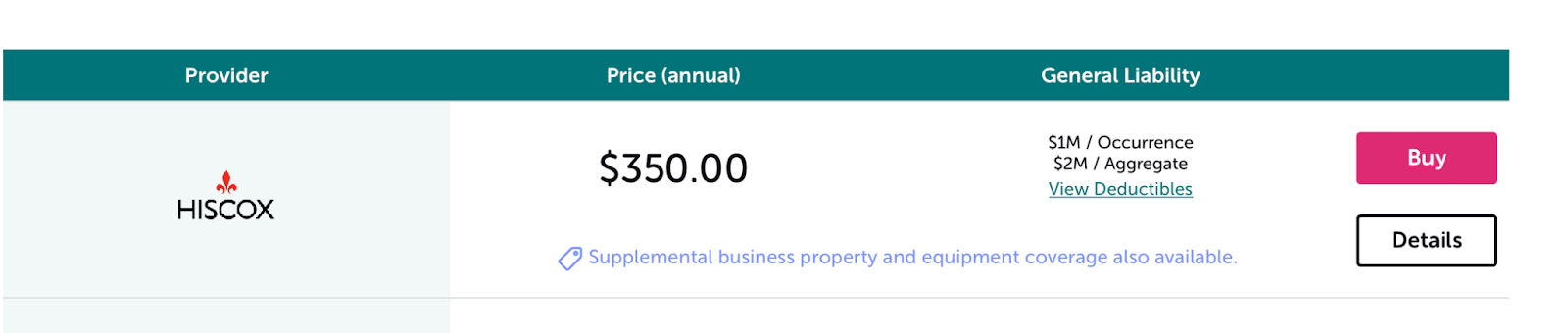

Simply Business general liability insurance quotes online

Below is the quote from Simply Business. They only offer online quotes from Hiscox. However, they also offer quotes from another 3-4 companies on the phone.

Next general liability insurance quotes online

Here is the quote from NEXT insurance. This is also the second cheapest quote for an accounting firm located in Madison, Kansas.

General liability insurance requirements in Kansas

General liability insurance is not legally required by the state of Kansas although the Department of Insurance in Kansas state advises that any business that sells goods or services in the state should have general liability insurance.

Did you know that slip and fall accidents account for over a million emergency room visits every year? The chances that one of your customers will slip and hurt themselves are pretty high. Likewise, if your business visits people in their homes or on their property, you run the risk of damaging their property and having to pay out of pocket if you don’t have insurance.

If you lease or rent a space, however, your landlord may require it. The policies that Kansas requires are commercial auto insurance (if you drive a vehicle for business purposes) and workers compensation insurance (if you have one or more employees).

Why should Kansas small businesses have general liability insurance?

According to the U.S. Chamber of Commerce, small businesses that are sued pay an average of $274,000 in legal costs. This is many times more than what small businesses can afford to pay out of their pockets. As a result, small businesses are much more likely to go out of business after being sued than large businesses.

Given that the cost of a general liability insurance policy for small businesses in Kansas is just about $400 per year. Small businesses in Kansas should have general liability insurance to protect them from the high costs of lawsuits.

What does general liability insurance cover in Kansas?

General liability insurance (GL), also known as business liability insurance, or commercial general liability (CGL), is a coverage that can protect you from a variety of claims arising from your business operations,

These claims may include the following:

Bodily injury

General liability insurance protects against business-related incidents that cause bodily harm to a third party. For instance, if one of your employees mistakenly drops on hammer on someone’s foot, this coverage should cover any damages. This coverage, however, only does not apply to employee injuries.

Property damage

General liability can also protect you from any third-party property damage caused by your business operations. For example, imagine you break a client’s window while cleaning their apartment; this policy should cover the damages.

Product liability

General liability insurance protects against liability for faulty products. Products are any goods that your company manufactures, sells, or distributes. This coverage protects a business if such a product causes physical injury or illness. For instance, if your customer becomes sick after buying infected food from you.

Operations liability

Completed operations coverage is just like product liability. It, however, protects you against faulty services or work performed by your business. For coverage to apply, you must finish such a project.

For example, a customer hires your service clean their bathroom. However, you forget to turn off a tap in the bathroom, causing the bathroom to flood after you left. Your general liability may cover the damages caused since you already left when the issue happened.

Personal and advertising injury

Your general liability policy may also cover any written or verbal communications that cause harm to a third party. This includes, among other things, libel, slander, malicious mischief, and copyright infringement.

For example, if your local competitor accused you of spreading rumors about their poor customer service. The company can sue you for personal and advertising injury if the competitor’s reputation and profitability are harmed. In such a case, general liability will cover you.

Damages to rented property

Damage to land, buildings, or structures you rent or lease is also typically covered under general liability coverage. For coverage to apply, the insured or their business must be legally liable for the damages.

For example, a local baker may rent a property that catches fire due to a careless employee leaving the oven unattended. General liability may cover the damages because the business operations caused the fire. On the other hand, this coverage would not apply if a lightning strike started the fire.

Learn more about general liability insurance coverage

What doesn’t general liability insurance cover?

Although general liability insurance is one of the most important policies for small businesses, it doesn’t protect businesses from all risks. The policy doesn’t cover the following:

- Employees’ injuries and accidents at work. This has to be covered to workers comp insurance

- If you or your employees are involved in an accident while driving for business purposes, you’ll need commercial auto insurance to cover this.

- If your business provides services or advice and is sued by your clients because they believe you make a mistake or are negligent, you’ll need commercial auto insurance to cover that.

How much does general liability insurance cost in Kansas?

As you can see, general liability insurance averages about $408 a year, or $34 a month (with a down payment usually due the first month). However, costs can vary widely, you may find you pay much more or slightly less. Below is the summary of Kansas general liability insurance costs from several companies:

| Companies | General liability insurance cost in Kansas |

| InsurePro | $31 per month |

| NEXT | $42 per month |

| Simply Business | $29 per month |

This is just the average. Your rates from these companies will be different. Be sure to shop around with a few companies or to work with a digital broker like Simply Business, CoverWallet, or InsurePro to compare several quotes to find the cheapest one for your company.

What affects general liability insurance costs in Kansas?

There are many factors that affect how much you’ll pay for business insurance in Kansas. They include:

- Industry

- Years of experience (yours)

- Business structure (sole proprietor, LLC, partnership, corporation, etc)

- Location (even within Kansas, some areas have higher risks than others)

- Size of the business

- Payroll

- Revenue

- Claims history

- Deductible

- Policy limits

The higher the risk in your industry, the more you’ll pay for insurance. Contractors usually pay much higher rates than, say, accountants.

How to find cheap general liability insurance in Kansas

The easiest way to save money is to shop around. Get quotes from at least three different companies. If you go through an insurance broker, try a few to get multiple quotes. For the investment of just an hour or two, you could save hundreds of dollars.

Choose a higher deductible. Just be sure you have that money available somewhere in case you need it.

Make sure you run a safe business. Have a safety policy and post it where everyone can see it. Don’t encourage your workers to rush, as this often leads to mistakes and injuries. Make sure floors are swept and equipment is picked up and put away.

Insurance agents sometimes get a bad rap, but if you find a good one, they can help you save money. They’ll steer you toward the insurance policies you need and tell you which ones you don’t need. You want to work with an independent agent, not a captive agent. An independent agent works with many insurance companies and can help you find the best price. A captive agent works for only one company and will only be able to sell you policies from that company: no matter how expensive they are.

Lastly, consider bundling general liability with other commercial insurance policies that your business may need. The most popular bundle is general liability and commercial property policies. In many cases, this means that you will buy a Business Owners Policy (BOP) for these two important coverages.

Learn more at the cheapest general liability insurance companies for small businesses

3 industries with the cheapest general liability insurance in Kansas

The three industries with the lowest general liability costs are:

- Photo and video – Learn more at photographer insurance

- Hair salon –

- Insurance professionals – Learn more at E&O for insurance agent

Do you still need a product liability policy if your business manufactures and sells physical products?

General liability insurance is a type of insurance that provides coverage for business owners against certain types of claims, such as personal injury, property damage, and advertising injury. Product liability insurance, on the other hand, is a type of insurance that provides coverage for businesses that manufacture or sell products. Product liability insurance covers businesses in the event that a consumer sustains an injury as a result of using a product that was manufactured or sold by the business. Some of the similarities between general liability and product liability insurance include:

- Both types of insurance provide coverage for certain types of claims.

- Both types of insurance are designed to protect businesses in the event that someone suffers an injury as a result of using a product or service.

- Both types of insurance are available to businesses in the private and public sectors.

There are also some key differences between general liability and product liability insurance:

- General liability insurance covers businesses in the event that someone suffers an injury at the workplace or as a result of the business’s operations. Product liability insurance, on the other hand, covers businesses in the event that a consumer sustains an injury as a result of using a product that was manufactured or sold by the business.

- General liability insurance is more popular and widely used than general liability insurance. Most small businesses should have general liability insurance

- Product liability insurance is typically more expensive than general liability insurance.

General liability insurance vs. workers comp insurance: which one do you need?

Both general liability and workers compensation insurance provide coverage for businesses in the incident of someone getting injured at a worksite.

The main difference between the two is that workers compensation insurance is specifically designed to protect employees who are injured or become ill as a result of their job, while general liability insurance provides businesses with coverage from claims of any third-party’s personal injury or property damage.

Do I need both general liability insurance and professional liability insurance?

General liability insurance is different from professional liability insurance because it covers a wider range of incidents. General liability insurance is designed to protect a business from any third-party claims, such as injuries or property damage that occur as a result of the business’s operations. Professional liability insurance, on the other hand, is specific to certain professions and covers claims made by clients for alleged negligence or mistake or malpractice. It is usually for professionals in business of giving advice or services to their clients such as accountants, financial advisors, doctors, nurses, or engineers.

Does general liability insurance cover data breaches and hacks?

Many people may think that since general liability insurance cover property damages of the business’s customers and any data breaches or cyber-attacks will result in customers’ property damages, general liability insurance should cover it.

You will be surprised to learn that general liability insurance doesn’t actually cover data breaches and cyber hacks. Many general liability insurance policies actually highlight the exclusions of property damages resulting from data breaches and cyber attacks Cyber liability insurance is designed to protect businesses from the financial fallout of a cyber attack. It covers the costs of repairing or restoring your computer systems, as well as the costs of any legal action that may be taken against you in the wake of a cyber attack. General liability insurance, on the other hand, covers accidents and injuries that occur on your work sites or as a result of your business activities.