Every motorized vehicle in the state of Maryland is required to have at minimum liability coverage. Regardless of whether the vehicle is used for personal or business purposes, that is. If insurance policies are canceled or non-renewed for any reason, the insurance company is required to notify the Motor Vehicle Administration that the policy was terminated.

- 5 best commercial auto insurance companies in Maryland

- Commercial auto insurance requirements in Maryland

- What does commercial auto insurance cover in Maryland?

- How much does commercial auto insurance cost in Maryland?

- Factors affecting the cost of commercial auto insurance in Maryland

- How to save money on commercial auto insurance in Maryland

5 best commercial auto insurance companies in Maryland

- Progressive: Best Overall

- biBERK: Best for low-cost coverage from a reputable carrier

- Smart Financial: Best if you prefer working with a knowledgeable agent

- THREE: Best for a complete and comprehensive policy

- biBERK: Best for low-cost coverage

Progressive: Best Overall

Progressive writes more than 13 million auto insurance policies annually. The company is known for personal auto insurance policies, but they also offer commercial auto policies. In fact, they are the biggest commercial auto insurance company with 12% market share.

Progressive provides online quotes, and the company boasts of 24/7 claim service. There is an app to help you manage your payments and coverages. You can get a quote on Progressive website in less than 10 minutes and buy a policy immediately. Progressive is one of the three companies offering commercial auto insurance quotes online in Maryland. The other two companies are InsurePro and THREE, which we cover below as well.

Progressive doesn’t offer the cheapest policy, however, their coverage is the most comprehensive and with the highest limits.

If you want to make sure you will be well-covered when things happen, you should consider Progressive. Even if you are not sure you can afford it, it doesn’t cost to get a quote on their website to compare with other options. It only takes 5-10 minutes.

biBERK: Best for low-cost coverage from a reputable carrier

bibERK is a subsidiary of Berkshire Hathaway, the reputable parent company of Geico. They definitely have a stellar reputation and excellent financial strength to honor their promises to their customers and pay the claims when they need to.

biBERK builds a direct-to-customers business model. They sell commercial truck insurance directly to the customers. Their business model helps them save costs and pass savings to their customers. In fact, they claim that their customers will be able to save at least 20% premiums when buying commercial truck insurance from them.

Thanks to their direct-to-customer business model, they are one of a few carriers that can offer commercial truck insurance quotes online. You can get quotes and buy a policy completely online in a few minutes.

Pros:

- A part of Berkshire Hathaway’s family. Excellent financial strength

- Claim to save 20% on premiums

- Can download copies of your insurance certificate online

- Easy to file claims online

Cons:

- Best for simple insurance needs

- Not all types of insurance are available in every state

Smart Financial: Best if you prefer working with a knowledgeable agent

Smart Financial is an online insurance broker specializing in providing small businesses insurance products. Most of the company’s client base has an annual revenue of less than $100 million. If you prefer the traditional way of buying business insurance, ie. working with an agent, Smart Financial is the best option for you. They partner with a network of hundreds of agents, each of whom is the most knowledgeable in their own field and industry. After you submit a quote request on Smart Financial’s website, their algorithm will match you with the most knowledgeable agent about your specific situation and industry and the agent will help you find the best coverage at the most affordable price.

If you have a hard time finding coverage for your company because of any reason, maybe you have a bad driving record or your company has filed too many claims in the past, etc. Smart Financial might be able to help you find coverage.

THREE: Best for a complete and comprehensive policy

THREE insurance is another subsidiary of Berkshire Hathaway, the owner of Geico. They believe that small business insurance should be simple and easy to understand. That’s the reason why their commitment to you is that their policy document is always 3-page long and always includes all coverages that your small business may need. So even if you only apply for commercial auto insurance, THREE will provide you with a quote including not only commercial auto insurance, but also general liability and commercial property coverages, which are the two most popular insurance coverages for small businesses.

If you want to get one single and comprehensive policy protecting your small business at a reasonable price, you may want to get a quote from THREE.

biBERK: Best for low-cost coverage

biBerk provides affordable insurance to small businesses to help them save money. biBERK offers an easy-to-use enrollment process, but its experts can help you figure out policies and coverage. biBERK offers competitive rates for its commercial truck insurance policies. In fact, they claim that they save trucking businesses at least 20% on truck insurance. They also offer other business policies.

biBERK is one of a few companies offer trucking insurance quotes online. Within less than 10 minutes, you can get a quote on their website and if you are happy with the quote, you can buy the policy online as well.

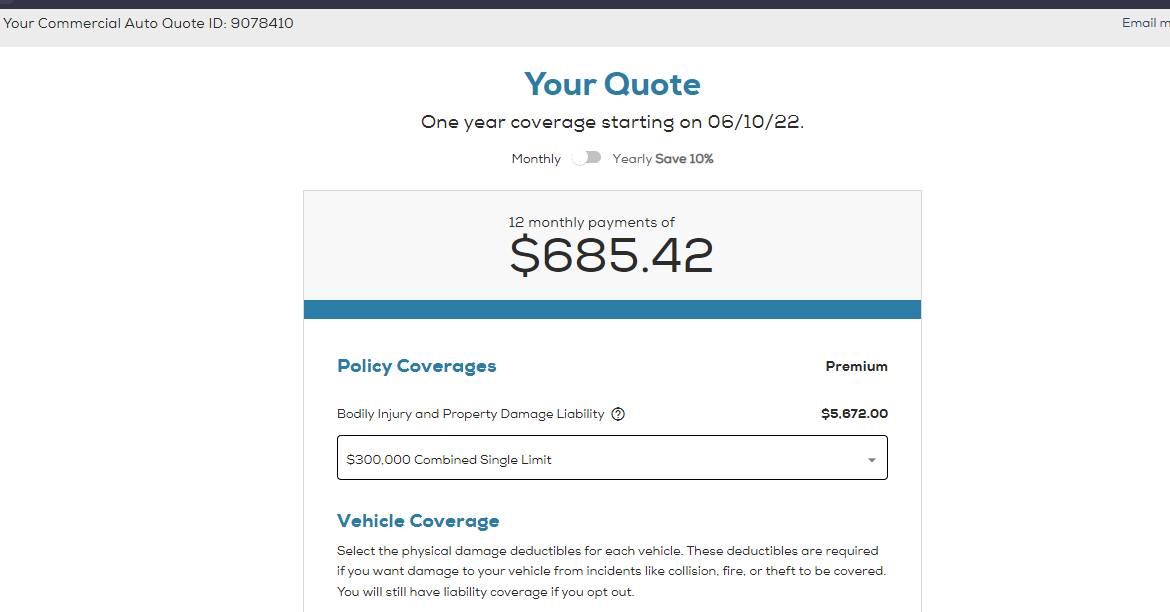

The following is a sample quote from biBerk for a box truck in Chicago.

Pros

- You can get quotes and buy insurance online

- You can file claims online

- Most of their policies are low-cost

- They have a strong financial backing. It is a subsidiary of Berkshire Hathaways, ie. the same owner of Geico.

Cons

- The policy’s coverage limits may be lower than usual, but they can adjust the coverage limits that work best for you.

Commercial auto insurance requirements in Maryland

It is required by law in Maryland that if you use a vehicle for business, you must have commercial auto insurance. Personal auto insurance policy will not cover you and your vehicle. If you are involved in an accident while driving for your business and don’t have commercial auto insurance, your personal auto insurance company will refuse to pay you and may drop you off altogether. And you may not be able to get coverage again. Learn more at commercial auto insurance: why small businesses need to have it and the differences between commercial auto insurance and personal auto insurance

All commercial auto policies in Maryland are required by law to have a minimum liability limit of of 30/60/15, or

- $30,000 per person

- $60,000 per accident for bodily injury, and

- $15,000 for property damage

Above is the state’s minimum coverage requirements. However, higher coverage limits may be required in some policies based on the types of vehicles they insure. Quotes by any insurance companies we recommend above should already meet the state’s minimum requirements for the specific vehicles of your company.

Maryland law also requires all commercial vehicles have uninsured motorist coverage (UM/UIM). This coverage helps pay for the medical expenses and property damages that result from injuries caused by both uninsured and underinsured drivers and hit-and-run situations.

You should select limits that are best for your business in addition to the minimum requirements of Maryland state law. Lacking the right amount of protection for your unique risk could leave you responsible for financial debts that might force your company and even yourself to bankrupt.

What does commercial auto insurance cover in Maryland?

Commercial auto insurance provides insurance in case you’re in an accident. It covers the following situations in Maryland:

- Liability: if you cause an accident, this will protect you from bodily injury to other people in the accident. It pays for medical costs and lost wages of anyone injured.

- Collision/Comprehensive: Much like in a personal auto insurance policy, this covers damages to a third party and your own vehicle if you’re in an accident. It also covers theft, vandalism, weather damage, and damages from animals.

- Uninsured motorist coverage: Pays for your injuries and/or property damage if you’re hit by an uninsured motorist.

- Underinsured motorist: the person who hits you has coverage, just not enough

Who needs commercial auto insurance in Maryland?

Any businesses with a vehicle must have commercial auto insurance. In general, if you drive a vehicle for business purposes, you must have commercial auto insurance.

How much does commercial auto insurance cost in Maryland?

The average cost of commercial auto insurance in Maryland is $145 per month, or $1,740 per year. Some companies offer commercial auto insurance in Maryland for as low as $97 a month. Other companies may pay up to $650 per month for their commercial auto insurance coverage.

The costs are significantly affected by the coverage limits you select when purchasing your policy. Other factors affect your cost as well.

This is just the average. Your rate will be different. Be sure to shop around with a few companies that we recommend above. Get quotes online from Progressive, Simply Business, InsurePro, and THREE to compare and select the cheapest one for your company.

Factors affecting the cost of commercial auto insurance in Maryland

The risks you incur while operating your business affect your commercial auto insurance costs in Maryland. Several things affect your risk assessment. Here are a few of them.

- What is your business? The kind of business you have and how often you drive for that business affect your rates. Different businesses have different levels of risk. For example, someone who delivers meals once a week will have a different risk level than someone who delivers industrial parts daily.

- What kind of vehicle do you have? Different vehicles rate differently with insurance companies which affect your rates.

- What is your driving history? Do you have a good driving record, or do you have multiple moving violations or parking tickets? A good record gets you better rates.

- What is your location? You can expect higher insurance premiums if you live in a risky area.

- What is your mileage? Are you traveling 100 miles or more a day? How far you drive will affect how much you pay for your insurance coverage.

- What coverage do you need? The amount and kind of coverage you need will increase or decrease your rates.

How to save money on commercial auto insurance in Maryland

Commercial auto insurance is a necessary expenditure, but there’s no reason you can’t save money wherever possible. Here are a few tips for saving money on your premiums.

- Keep a good driving record. Any driver who drives for your company should maintain a good driving record.

- Pay your premiums on time, every time. Keeping up with your premiums will save you on late fees and could lead to discounts further down the road.

- Pay your total six-month or annual premium upfront rather than breaking it into payments whenever possible.

- Talk to your insurance agent and determine if they offer discounts or bundled policy rates to help you save.

- Compare costs from at least 3 companies. Feel free to shop around for the best prices. You aren’t required to purchase the first policy you are quoted.

Final thoughts

Maryland requires all vehicles to maintain minimum liability coverages. Suppose you have an automobile you use for business beyond commuting to work. In that case, you should purchase commercial auto insurance because your auto policy may not sufficiently cover your business risks.