If you work as a photographer, or even if it’s just your favorite hobby, your equipment is a significant investment. Have you thought about what would happen if your equipment were stolen, lost, or destroyed? Whether you run a business or you have a habit of carrying your camera with you everywhere, insurance for your camera and other equipment is a must.

If you’re wondering where to get insurance for your photography equipment or if other policies will cover your camera and equipment, this guide is for you. We’ve compared insurance companies that insure photography equipment and created a list of the six we considered the best.

- 6 best camera and photography equipment insurance companies

- What is camera insurance for photographers?

- What does camera insurance cover?

- Other insurance coverage photographers may need

- How much does camera insurance cost?

- Does homeowners or renters insurance cover cameras and other photography equipment?

6 best camera and photography equipment insurance companies

- Simply Business: Overall best photography insurance company

- NEXT: Fastest online quote

- CoverWallet: Best online broker

- InsurePro: Best for flexible on-demand short-term coverage

- FullFrame: Best for those on a budget

- Hill & Usher: Best for all media professionals

Simply Business: Overall best photography insurance company

Simply Business is an online insurance broker that works with top-rated carriers to provide small business owners with the policies they need. The application process for Simply Business is easy, and you typically receive quick responses with quotes from multiple insurers.

General liability and professional liability coverages are the top two necessary for any photography business. Simply Business combines both into a single package. For camera and photography equipment, Simply Business also offers commercial property coverage.

You can choose the general liability limits that best suit your business. For general liability, that’s between $100,000 and $2 million, and for professional liability, that’s up to $3 million. Keep in mind that a higher limit will also lead to a higher insurance policy premium.

Simply Business specializes in liability insurance. That means you may not be able to purchase all of the coverages you need on a single policy. They do have starting premiums beginning at $25.95.

Pros:

- Get multiple quotes with one application

- No brokers fees

- Online quotes and purchasing when ready.

Cons:

- Policies don’t always include equipment

- Financial ratings are based on the carrier, not Simply Business.

- No online account management

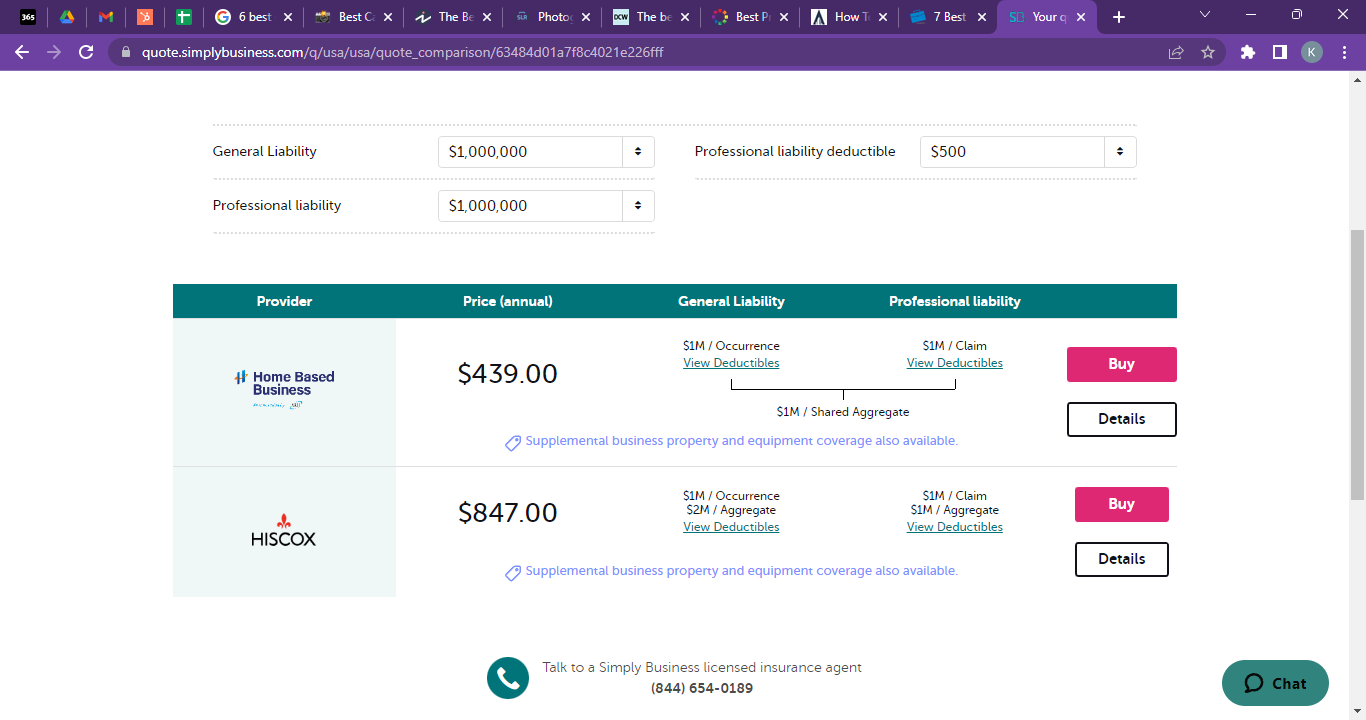

The following image represents an online quote from Simply Business for a photography business in Gadsden, Alabama.

NEXT: Fastest online quotes

NEXT specializes in small business insurance. According to their website, they’ve been rated 4.7 out of 5 by over 100,000 people across various small business industries. If you must make a claim, the company attempts to make claims decisions within 48 hours, so you are back to business quickly.

Obtaining a quote from NEXT was a simple online process that took less than ten minutes. Their application is simple and easy to understand. The online process tailors your quote to match the criteria you enter on the website. If you choose a policy from NEXT, you get access to unlimited insurance certificates 24 hours a day, seven days a week.

Pros:

- Easy online application

- Bundled policies can mean discounts

- Unlimited access to a digital certificate of insurance

Cons:

- All digital process can be off-putting to older business owners

- Doesn’t offer some specialized insurance coverages

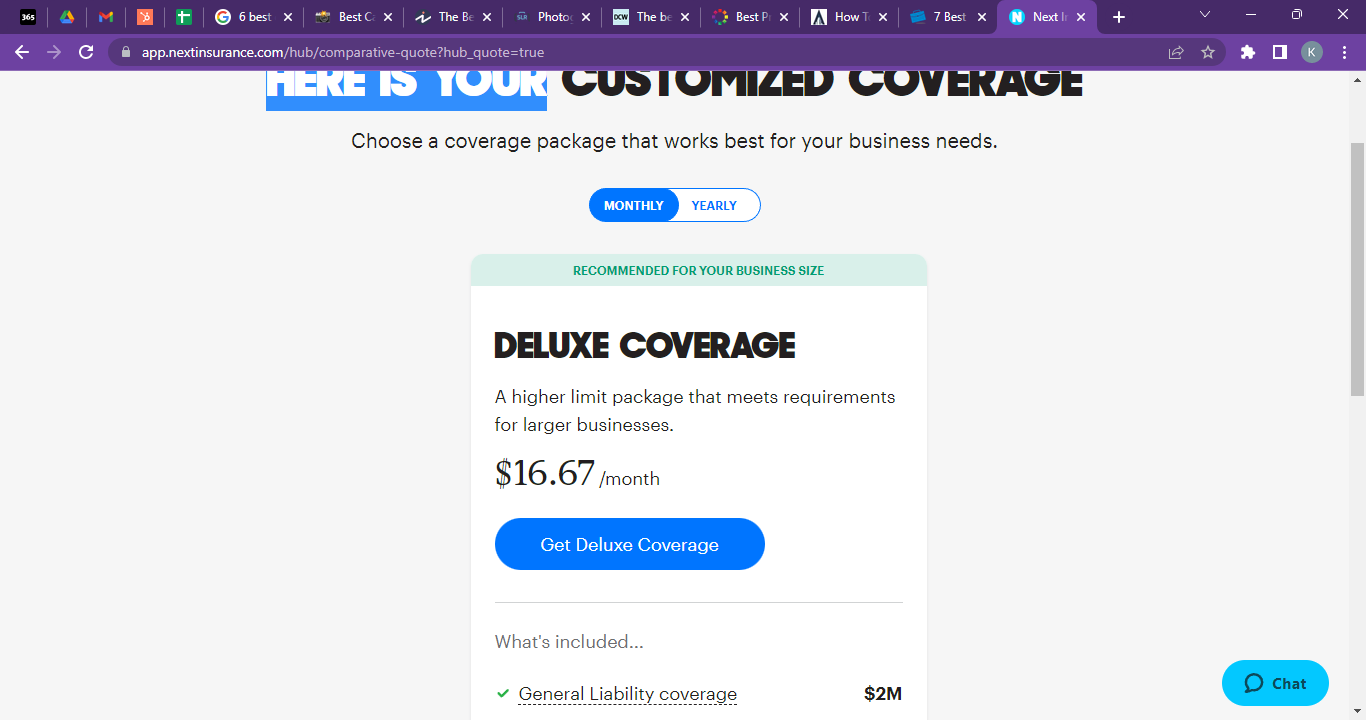

The following image is a quote from NEXT for a photography business in Athens, Alabama.

CoverWallet: Best online broker

CoverWallet is an online insurance broker specializing in small business insurance. The application process is relatively simple, although they do ask for more detailed information than some other companies. Typically, the entire process takes about ten minutes, from request to quote. However, it sometimes takes a little longer for the company to return quotes to you.

The company collects your information and generates up to three quotes based on your submissions. If it’s taking a while for them to get the quotes, they give you the option of having the quote emailed to you. When the company provides you with a quote, you have the option to purchase that policy immediately.

Pros:

- Get quotes from several providers with one application

- Various coverage types are available

- Online dashboard for policy management

Cons:

- Coverage provided by the third party

- Sometimes required to call to obtain a quote

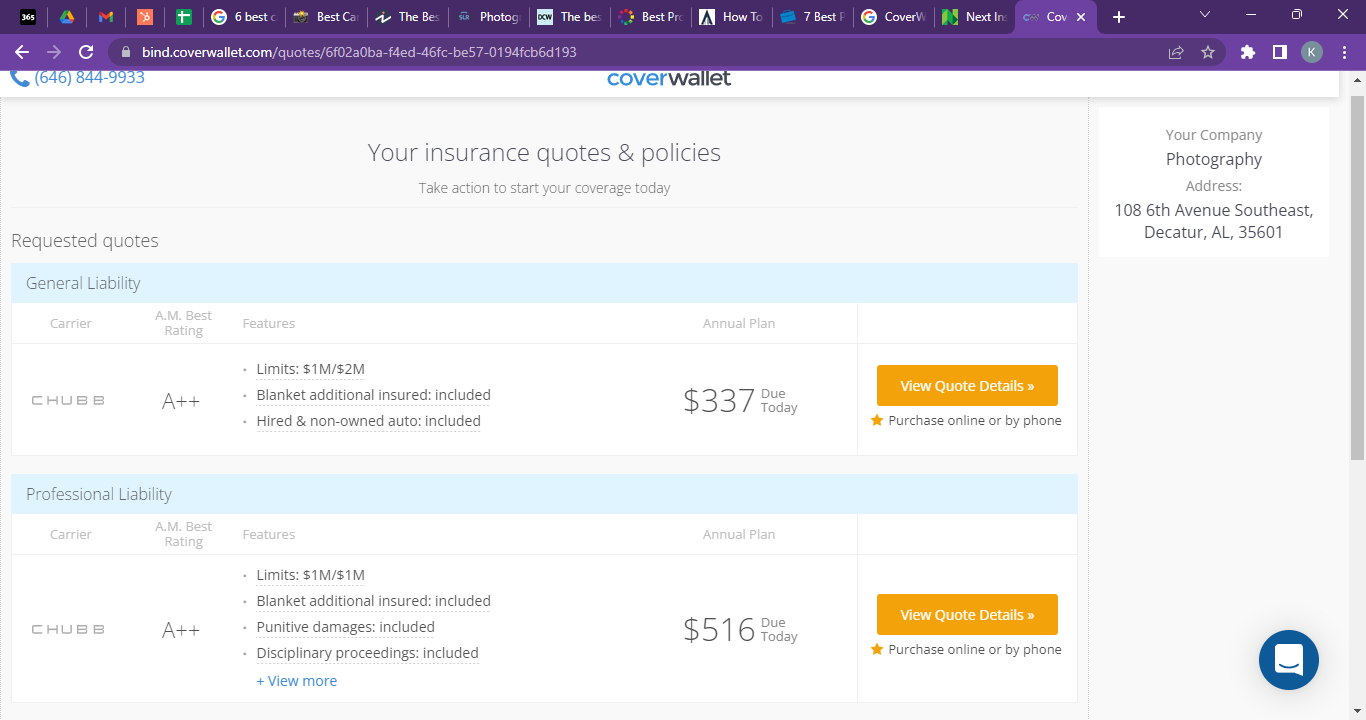

The following is a quote we obtained for a photography business in Decatur, Alabama. As you can see, based on the information we provided, CoverWallet returned two quotes.

InsurePro: Best for flexible on-demand short-term coverage

InsurePro compares quotes from over 20 companies to help you find the right insurance for your business. You complete one online application, and they do the legwork for you. The company offers several coverage options for business owners, but if you need a specialized policy, you may want to look elsewhere.

InsurePro coverages include general liability, worker’s compensation, commercial property, and commercial auto. If you’re looking for quotes for good basic business insurance, this company may be able to help you. The company works with various providers to find the coverage you need. Travelers, Liberty Mutual, and Nationwide are some of the well-known companies they work with.

One of their unique differentiators is their on-demand short-term coverage. For photographers who may need coverage for only one day, a few days, or just an event, InsurePro is the best option. They offer pay-per-day coverage, which can help them save a lot of money.

Pros:

- Complete one application online

- Works with multiple companies to find the best quotes

Cons:

- Only offers basic coverages

- The third-party handles underwriting and other services

Full Frame: Best for those on a budget

Full Frame has scalable coverage that is designed for the unique needs of photographers and videographers in the US. Coverage is available in 44 states, and the easy, hassle-free quotes process is handled completely online.

Full Frame offers coverage for equipment that helps to repair or replace damaged or stolen items. They also offer errors and omissions, general liability, professional liability, and coverages for damage to rented premises.

There are three policy plans to choose from based on the needs of your business. The Annual Plus policy includes general liability coverage as well as multiple camera insurance options and additional coverages. The policy also includes unlimited additional insureds.

The Annual policy is slightly less expensive than the Annual Plus and includes everything except the camera insurance options. The Event policy is the least expensive of the three policies and is designed to protect you at an event. The coverage is good for up to three days. It includes $2 million in general liability coverage and unlimited additional insureds.

Pros:

- Offers event coverage

- Specializes in photographer and videographer coverages

- Can choose from three policies based on business needs

Cons:

- Only available in 44 states

- Not all coverages include equipment coverage

Hill & Usher: Best for all media professionals

Hill & Usher is based in the US. They have a policy designed specifically for professional photographers which bundles property and liability coverage in one premium. Choosing their Package Choice policy gives your business comprehensive coverage.

Your equipment is protected even on location or while in transit in the US and Canada. You also have the option to extend your policy to include international coverage if you need to travel somewhere other than the US or Canada. Depending on the Hill & Usher policy you choose, your deductible will range from $250 to $1000. The company also allows you to cover rented or leased equipment.

A policy also covers any equipment within your studio with Hill & Usher. For photographers, this means computers, printers, darkroom equipment, supplies, furnishings, and any improvements you’ve made to a rented studio would be covered.

Pros:

- Covered in the US and Canada

- Offers international coverages

- Can cover rented or leased equipment

Cons:

- Must be US-based

- Website needs updating

What is camera insurance for photographers?

Camera and photography equipment are the most valuable assets of any photographer. They are considered the business property of any photography business.

Business property insurance covers your photography studio if it’s damaged by fire, extreme weather, or vandalism. More important to many photographers is that it covers equipment stored in their place of business if damaged, destroyed, or stolen. Equipment can include:

- Cameras

- Flashes

- Memory cards

- Computers and external hard drives

- Stands and backdrops

Professional photographers also need their cameras and other equipment covered during transit or at events as well. Business property coverage customized for photographers should offer the coverage.

What does camera insurance cover?

Camera insurance protects your camera and other equipment for your photography business if they are damaged by fire, extreme weather, or vandalism, or stolen in the following locations:

- at your studio

- in transit to your workplace, likely the event locations

- at event locations where you are working

The insurance policy may pay to have the cameras and other equipment repaired or replaced with new ones. You can also choose for the insurance company to pay you the value of the cameras as well.

Other insurance coverage photographers may need

In addition to protecting their cameras and other photography equipment, photographers may need other insurance coverage to protect their business. Below are some of the popular policies for photographers:

- General liability insurance protects photographers if their operations cause bodily injuries or property damage to their clients or other people at the events. For example, it will pay medical expenses if a wedding guest trips over a lighting cable and breaks a leg or if you accidentally break an expensive vase in a client’s home while taking a photo of their dog.

- Interruption for computer operations insurance pays if you can’t use your computers to process or store images.

- Professional liability insurance pays legal and settlement costs and damages if you’re ever sued over the professional photography services you provide. For instance, if you fail to show up at a wedding you were booked to photograph.

- Workers’ compensation insurance pays benefits if you or someone who works for you becomes injured or ill for work-related reasons. For instance, if a photographer slips on a rock while on a professional photo shoot and breaks an arm, workers’ comp will pay medical bills related to the incident, lost wages, job retraining, and more as needed. Your state will likely require you to get this coverage if you have employees.

- Commercial auto insurance covers injuries and vehicle and property damage if you or an employee is involved in an accident while driving for work. Personal vehicle insurance doesn’t pay for incidents when driving for work purposes.

- Business income off-premises coverage goes into effect if your equipment is damaged while you’re away from your primary business location. If you can’t complete a job because your equipment isn’t working, this coverage can help cover your lost income.

- Unmanned aircraft coverage helps protect a drone if you use one for work purposes.

Learn more at the best insurance companies for photographers and photography businesses.

How much does camera insurance cost?

The average cost of camera insurance is just about $12 per month, or $144 per year. This is for a comprehensive policy covering your camera and other equipment everywhere and with a coverage limit of up to $1M.

This is the cost for your camera insurance only. Photographers and photography businesses may need other coverages, which will cost more. Learn more at how much photographer insurance costs

Camera insurance is quite affordable. Make sure you shop around with a few companies to find the best deal for you and your business.

Does homeowners or renter’s insurance cover your cameras and other equipment of your photography business?

The short answer is no. Homeowners and renter’s insurance cover your personal belonging if they are damaged or stolen in your home. However, as soon as the insurance companies learn that your camera and other equipment is for your business, they will refuse to pay the claims. Homeowners and renters insurance does not cover your business belongings.

Your commercial property or business property insurance covers your business properties only when they are stored in your business location such as offices or warehouses. When your camera and other equipment are damaged or stolen in your car, or in transit, or at events where you are working, commercial property insurance policy doesn’t cover them.

Wedding photographer insurance

Many photographers specialize in weddings and they may want to get an insurance policy customized for weddings. Some wedding photographers work full time, many work part-time and only need coverage for the days when they work.

Learn more at the best wedding photographer insurance companies

Final thoughts

Whether you are a professional photographer or it’s your favorite hobby, the equipment can cost a pretty penny. If it’s your hobby, your homeowner’s insurance might cover any losses you may endure. However, if you use your cameras for business, you must purchase business insurance.