Business renters insurance includes any policy or combination of policies that protect small businesses that rent commercial property against certain losses and damages. This can include many types of property including offices, storefronts, garages, storage facilities, warehouses, and more.

In this article, we’ll reveal the top 5 renters insurance providers along with what makes each one stand out. We’ll also explain what you need to know to get the right renters business property coverage for you.

- 6 Best business renters insurance providers

- What is business renters insurance?

- Who needs business renters insurance?

- What does business renters insurance cover?

- How much does business renters insurance cost?

- What is the difference between replacement cost and actual cash value coverage?

- How can I get business renters insurance?

- How to get cheap business renters insurance?

6 Best business renters insurance providers

Here are our recommendations of the 6 best business renters insurance companies.

- CoverWallet: Best for comparing several quotes online

- The Hartford: Best for getting complete coverage through a Business Owners Policy

- Hiscox: Best for small businesses with multiple rented locations

- Chubb: Best for businesses that have locations in countries outside of the United States

- NEXT: Best for a great digital experience and affordable rates

- Simply Business: Best for finding cheap coverage

CoverWallet: Best for comparing several quotes online

CoverWallet is one of the leading digital brokers specializing in small business insurance. They partner with several leading business insurance companies. The advantage of working with CoverWallet is that once you complete their quote form, they are able to pull several quotes from their partners to present to you so that you can compare and select the best one for your business.

Of course, if you really want to get quote from a particular company and that company doesn’t partner with CoverWallet, you have to go to that company directly.

Once you buy a policy through CoverWallet, you are able to manage your business insurance policies completely digitally through their dashboard.

The Hartford: Best for getting complete coverage through a Business Owners Policy

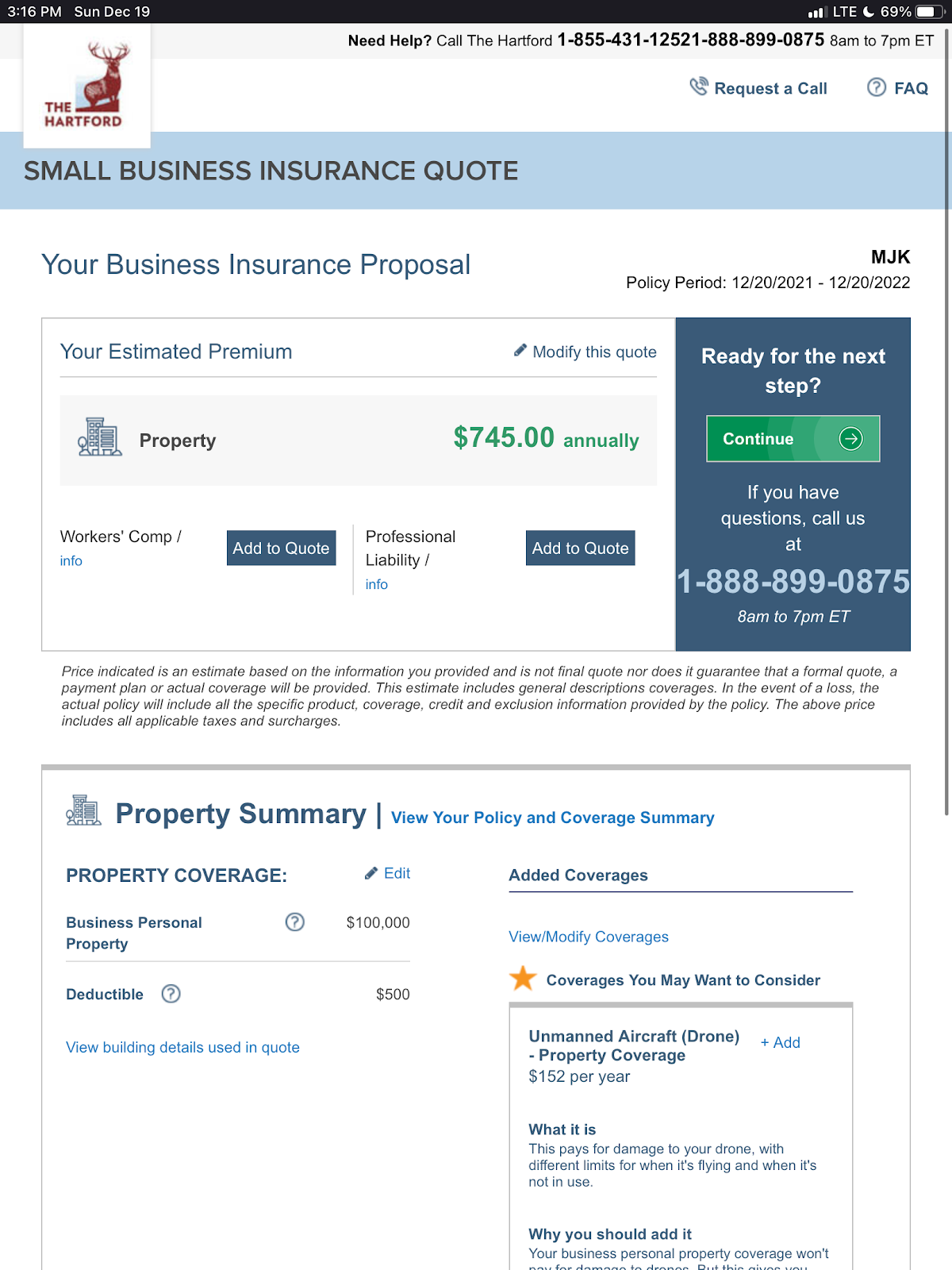

The Hartford is an established small business insurer known for its Business Owners Policy (BOP). The policy includes general liability, commercial property, and business income (or interruption) insurance. The coverage in it is designed to protect your business and spaces you own or rent from fire, theft, weather damage, and more. The Hartford makes it easy to customize coverages and levels. You can easily add other types of insurance to your BOP from The Hartford.

Here is a simple business renters insurance quote from The Hartford.

Hiscox: Best for small businesses with multiple rented locations

Hiscox offers a complete array of insurance solutions for small businesses in most industries. They make it fast and easy to customize a Business Owner’s Policy. A BOP from Hiscox typically combines general liability and property liability coverage. The BOP from Hiscox will protect property at up to five different business locations. Hiscox gives you the option to add business interruption coverage to your BOP (many providers include it in their core coverage). In addition, you can add coverage for things like vehicles owned and used by the business, data breaches, mistakes and errors made while doing business, employee accidents and injuries, and much more.

Chubb: Best for businesses that have locations in countries outside of the United States

Chubb is unique in that it offers renters and other coverage for businesses with international interests through its customizable Business Owners Policy. A BOP from Chubb combines general liability and commercial property insurance. Much like Hiscox, you will need to add business interruption coverage if you want it. Chubb also offers some unique types of property insurance, such as earthquake coverage, equipment breakdown protection, and crime insurance.

NEXT: Best for a great digital experience and affordable rates

NEXT is a 100% digital carrier. They are new, founded in 2016, specializing in providing general liability insurance online for contractors. Working with NEXT is fast and easy. You can do everything completely online.

Pros:

- Manage your policies online

- Easy online application process

- Writes their own coverage

Cons:

- Limited specialty insurance types

- Limited customer service support during the buying process

Simply Business: Best for finding cheap coverage

Simply Business is a broker specializing in small business insurance. They work with many carriers with a focus to help you find low-cost coverage that your business may need, including general liability insurance. They vet the carriers that they work with carefully to ensure that all of them have excelleny financial ratings.

Pros:

- Easy to get and compare several quotes online

- Able to get quotes from A-rated carriers which you may not be aware of

- Knowledgeable agents that are available to help you along the process

Cons:

- Quotes online are available for general liability and professional liability only

- Have to file a claim directly with the carriers

What is business renters insurance?

A business renters policy could include any or all of the following types of insurance.

- General liability insurance protects your business from non-employee claims related to bodily injuries, damage your business causes to client property while working, along with lawsuits related to advertising and reputational injuries. Learn more at the best general liability insurance companies and the cheapest general liability insurance companies.

- Commercial property (renters) insurance protects your business from losses that result from theft and property damage caused by natural disasters, weather events, or fire. This coverage is typically required by landlords for businesses that rent commercial property from them. Learn more at the best commercial property insurance companies.

- Business interruption insurance pays lost income if your business is ever unable to operate because of a reason covered by your insurance, such as a fire. This coverage is sometimes called business income insurance or income loss insurance. Learn more at the best business interruption insurance companies.

The easiest and most effective way to get these and the other coverages you need is through a Business Owners Policy (BOP), but more on that later.

Who needs business renters insurance?

Any organization that rents property for business reasons — whether it’s an office, storefront, garage, shed, or warehouse — should secure business renters insurance. Again, you will never find this coverage in any insurers application process. You simply click rent (or lease) rather than own when you apply for business coverage.

Most landlords require that a business renting property from them show proof of insurance. If this is the case for you, your landlord must specify what damages or claims on the property you are responsible for under the lease. They should also define the types and levels of insurance you must get to cover these obligations. You may want to get additional protection above what’s required to cover business owned equipment and other items used or stored in the rented space. Your business insurance agent or company rep can advise you on the right coverage types and levels for your business.

What does business renters insurance cover?

Again, there is no such thing as business renters insurance available through insurers. You will be getting business insurance, and inputting that you rent your property.

A business renters insurance policy should protect your business from claims and damages related to a rented property used by your company, including:

- Damages you, your employees, or a third party (for example, visitor to the location) make to the space.

- Damages to or theft of any equipment, inventory, or property used or stored in the rented space.

- Damages to the property or its content that are caused by a fire, natural disasters, and other covered event. (Your insurance agent or provider can explain what types of events are covered.)

- Accidents or injuries that happen in the rented space or on the property that result in a lawsuit against your business.

In most cases, a standard business insurance policy won’t cover all of these different things, which is why business renters insurance is usually a policy customized to the specific needs of a business or a combination of standard policies.

What is the difference between replacement cost and actual cash value coverage in business renters insurance?

Business renters insurance is offered with replacement cost versus actual cash value coverage. It’s important that you understand the difference.

- Replacement cost covers the cost of restoring, repairing, or replacing property to its original state, including labor, materials, or actual property replacement. This will pay whatever it takes to return things to like new condition, no matter what their condition or value was when they were damaged or stolen.

- Actual cash value pays to repair, restore, or replace damaged or lost property but will deduct some of the cost to do so for depreciation. You’ll receive compensation for what the property is worth at the time of the claim, as opposed to purchasing it in new condition..

Replacement cost commercial property insurance is more expensive than actual cash value coverage. However, if you have high value equipment or inventory that you need to protect, paying extra for it could be worthwhile.

How much does business renters insurance cost?

The cost can vary depending on many factors including the size and value of the property covered, number of properties, contents of the property, coverages and level of coverage, and more.

The average cost of business renters insurance is around $1,200 a year or $100 a month, but that’s only a benchmark. It’s a smart idea to get several quotes and compare them to ensure you’re getting the right coverage for you at the best possible cost.

Learn more at how much does business renters insurance cost?

How can I get business renters insurance?

Usually, the best way to get business renters insurance coverage is through a Business Owners Policy (BOP). A BOP is an insurance policy that combines general liability, commercial property (renters or owned) and business interruption insurance. Getting coverage through a BOP is generally the most cost effective and easiest way. You simply select rent rather than own when you complete your application and your BOP will be adjusted accordingly. Plus, a BOP makes it simple to add other coverages you may need to the base policy.

Learn more at the best Business Owners Policy (BOP) companies.

How to get cheap business renters insurance?

There are a few ways to find the coverage you need at a fair price:

- Shop around for the best value. Get quotes from a few companies and compare coverages and costs to find the best combination of the two.

- Don’t stop shopping around. Make sure you get new quotes when it comes time to renew your policy.

- Take advantage of discounts. If they’re not offered to you when getting a quote, ask about them, whether you’re buying online or through an agent.

Taking these steps will help ensure you’re not paying too much for your business renters insurance coverage.