SBLI stands for Savings Bank Life Insurance, and they are proud to say that’s all they offer–life insurance. SBLI feels companies that offer a ton of insurance products or toss in credit cards and other financial products tend to lose their way. They originated in 1907 by Louis Brandeis, whose goal was to help everyone get affordable life insurance. That’s still their goal today. As a mutual company they are owned by their customers, rather than their shareholders. They have protected over a million families since they started, and they have paid out over $4 billion dollars in dividends.

- Pros and Cons of SBLI Life Insurance

- Products Offered by SBLI Life Insurance: 60/100

- Financial Strength Rating of SBLI Life Insurance: 80/100

- Customer Satisfaction Rating of SBLI Life Insurance: 90/100

- Consumer Complaints Rating of SBLI Life Insurance: 50/100

- Digital Experience Rating of SBLI Life Insurance: 70/100

Pros and Cons of SBLI Life Insurance

| Pros | Cons |

| – Easy to obtain a quote – Some policies have a no medical exam option – Coverage for 49 out of 50 states – Dividends are possible with whole life – Good customer reviews | – Not available in New York – No online payments – No universal life insurance options |

>>MORE: Best Life Insurance Companies – Compare 30+ Life Insurance Companies

Products Offered by SBLI Life Insurance

SBLI offers both term and whole life insurance, as well as a unique blend of the two.

The term life insurance is available in terms of 10, 15, 20, 25 or 30 years. You can convert any term insurance policy to a whole or universal life insurance policy. There is a no-medical exam option if you are between the ages of 18 and 60 and want less than $500,000 in life insurance (although you will have to have a thirty minute interview with an underwriter, who will review your health history before setting a rate).

SmartTerm 360 is the ability to develop a policy that offers flexibility for your changing life circumstances. You can ladder two or three term policies to cover you for different phases of your life.

Whole life insurance is life insurance with a savings account attached. This is known as cash value, and once it accumulates you can either withdraw from the cash value or take out a loan against it.

They also have a policy called Flex whole life insurance, which allows you to choose a term life insurance rider to go along with your whole life insurance policy.

SBLI’s LifePace whole life lets you get a term insurance policy, or there is a 30-year Cash-Out term insurance rider. If you choose this rider, once you’ve had the policy for 30 years you can cash it out and get back all of the money you paid in premiums

>>MORE: A Guide to the Best Whole Life Insurance Companies

SBLI also offers some riders you can add to your policy, such as:

- Accelerated death benefit –

- Children’s level term rider – Learn more about life insurance for children

- Accidental death benefit – Learn more about accidental death benefit

- Waiver of premium

- Term rider

- Guaranteed purchase option rider – Learn more about guaranteed purchase life insurance

- Single pay paid-up additions rider

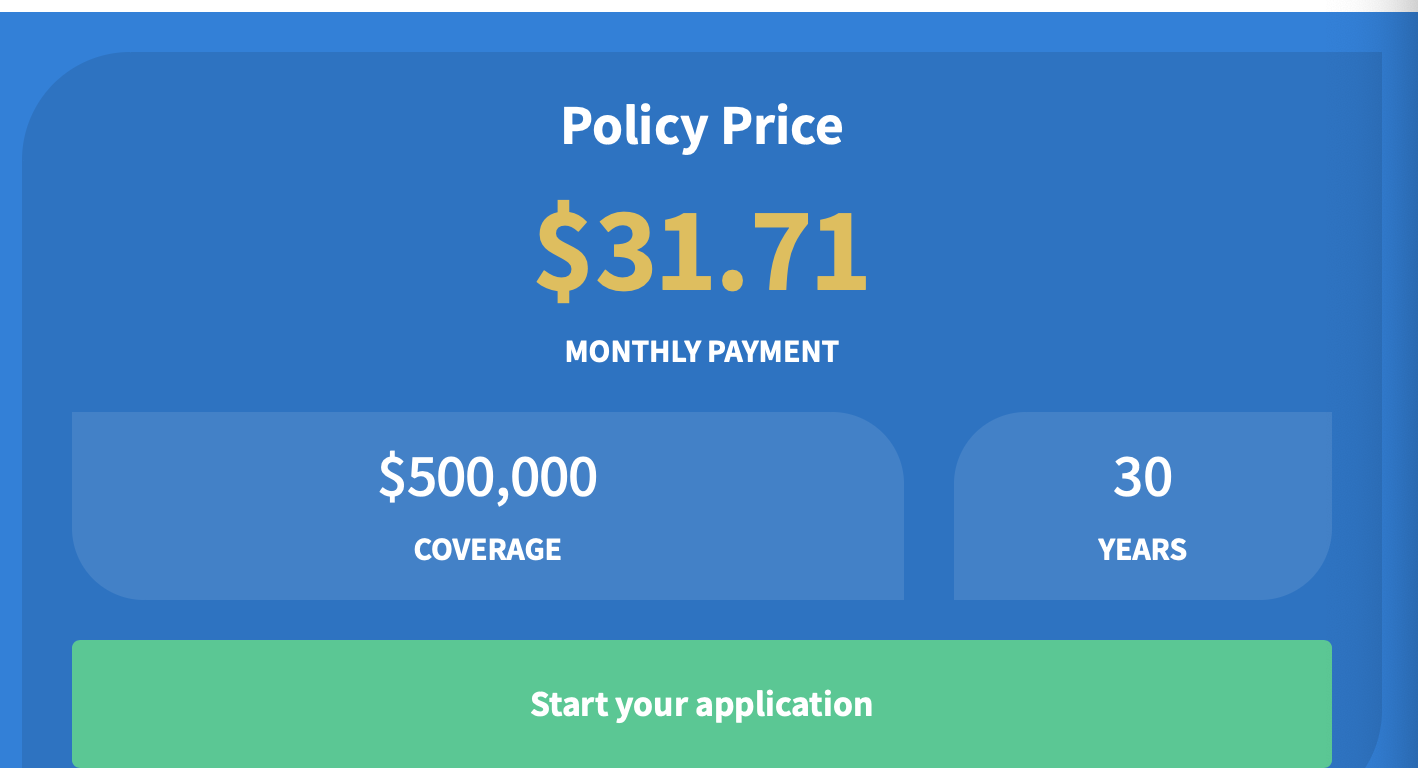

Getting a quote from SBLI is a simple process of entering your name, how much life insurance you want, your age and your health. For a 30 year old male in excellent health, SBLI gave us this quote:

Once you get a quote, you’ll start an application and you can be approved in as little as a week. An underwriter will review your health records and history and then formalize your rate.

>>MORE: 10 Largest Life Insurance Companies

Financial Strength Rating of SBLI Life Insurance

SBLI is not one of the largest life insurance companies, but they are a stable company.

A.M. Best gives them an A, with a stable outlook. This means they are more than able to meet financial obligations.

Customer Satisfaction Rating of SBLI Life Insurance

SBLI does not appear on J.D. Power’s life insurance study, so we’ll look at other websites. The BBB gives them an A+. They’ve been accredited since 2007. There are four customer complaints on the website, and four reviews. One of the reviews gives them five stars and one gives them three stars, with the last two being one-star reviews. Still, four complaints and four reviews are pretty minimal.

Consumer Complaints Rating of SBLI Life Insurance

The NAIC evaluates every insurance company and calculates a complaint ratio. The average median score is 1.0, which reflects the average number of complaints you would expect a company to have. SBLI earns a ratio of .98, so almost exactly the expected number of complaints.

Digital Experience Rating of SBLI Life Insurance

Securing an online quote for term life insurance is easy, although whole life insurance will require a call, but this is pretty typical for whole life insurance. SBLI has been trying to update their online experience in general, and you can now file a claim online, as well as ask for help from the online chatbot.

Like many life insurance companies, there is an online insurance calculator, so that you can figure out how much life insurance you need. It asks you about your income, if you’re married, your savings and investments, number of children and how much debt you have.

They have what they call “Life’s Mission Control” where you can store all of your financial accounts online, as well as everything your family might need in the event of your death. These include power of attorney, advance directives, retirement accounts, etc. You could just as easily give this to a lawyer or even drop it all in a file cabinet, but it’s a nice touch.

You can pay your premiums by automatic bank draft or by check—so far, no online payments, which is a bummer.

Last Thoughts

While not the largest life insurance company, SBLI has been around for over 100 years. They are a solid company with good customer service and decent rates. If you are interested in a simple life insurance policy and are shopping around, it’s worth getting a quote from them. On the other hand, if you want to explore universal life options, variable or indexed, SBLI can’t help you. But if all you need is term, or even whole insurance, they’re worth a look.