Workers Compensation Insurance is required by state law in all states, except Texas. It is a crime in many states if you don’t have it. It protects you as a small business owner from potential law suits and provides your employees medical costs and potential wage loss when they get injured at work. Getting workers’ compensation insurance should be a priority for any businesses. Shopping around with multiple carriers or working with an independent agent or broker who can help you shop is important to get the best price. The good news is that many insurance companies offer this product. Here is our pick of the best 7 companies offering Workers Compensation Insurance for small business for your consideration.

Best 10 Workers’ Compensation Insurance Companies

After researching more than 30 companies offering workers compensation insurance, including both traditional and insuretech insurance companies, here are our top 10 recommendations:

- CoverWallet: Best for Comparing Online Quotes from Leading Companies

- Pie Insurance: Best for Getting Online Quotes

- Foresight Insurance: Best for Medium-Sized Businesses in High-Risk Industries

- Huckleberry: Best for Getting Online Quotes of Workers Compensation and other Related Insurance

- Geico Workers Compensation Insurance: Best for Getting Insured Fast

- Travelers: Best with a Flexible Payment Plan

- Nationwide: Best with a Great Claims Center With a Robust Toolkit

- Liberty Mutual: Best with a Managed Care Pharmacy Program

- The Hartford: Best with Their Comprehensive Preferred Medical Provider Network

- Next Insurance: Best for Small Businesses with a Fully Digital Experience

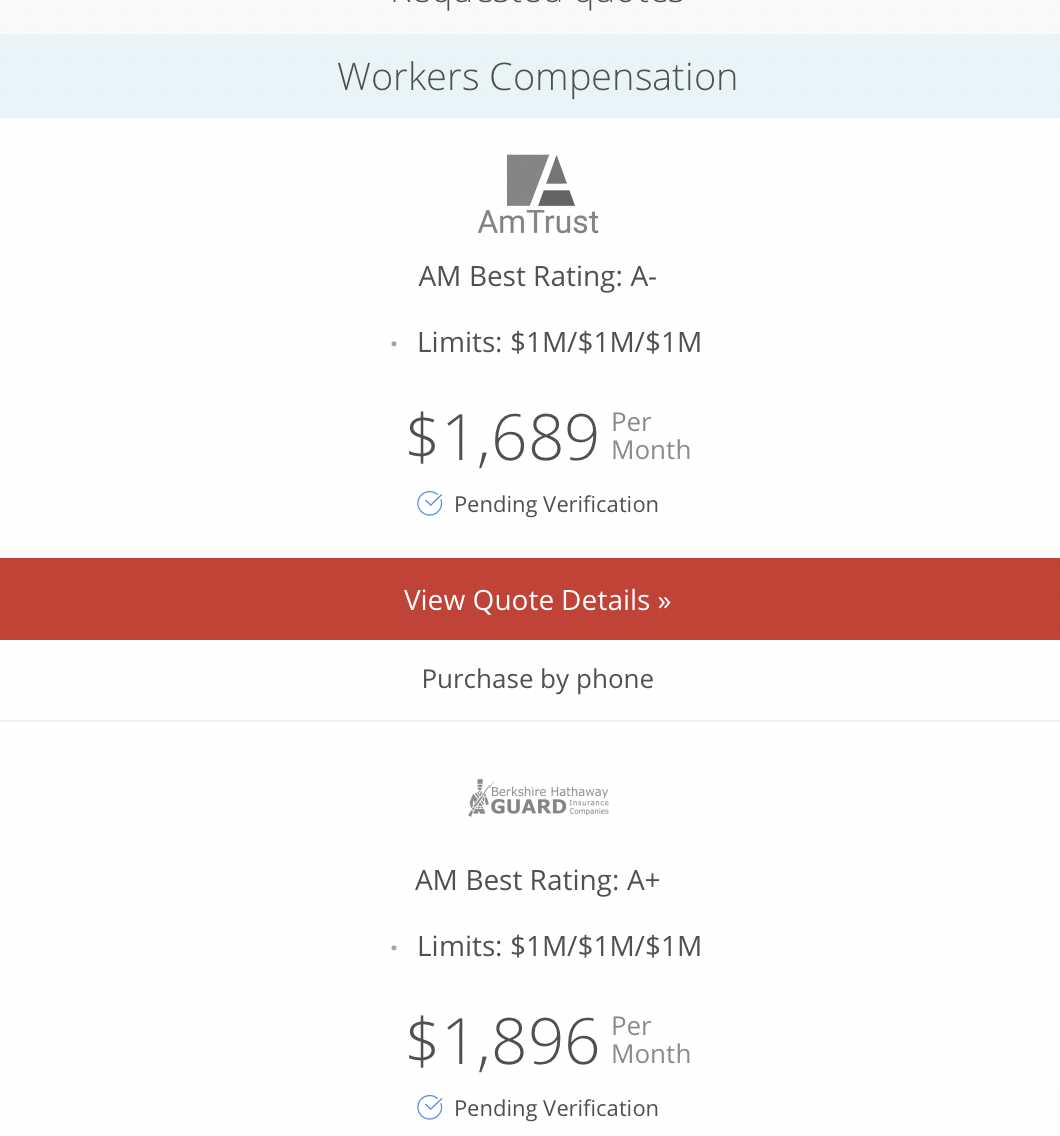

CoverWallet – Best for Comparing Online Quotes from Leading Companies

CoverWallet specializes in commercial insurance for business. In addition to workers compensation, you can also get quotes for general liability insurance, professional liability insurance, umbrella insurance, commercial auto, and others. Keep in mind that CoverWallet is actually an insurance broker that works with many insurance companies and is able to get quotes from these companies for your comparison.

The following quote is for a landscaping business located in Sacramento, CA with 10 employees and a $1 million in revenue. We tried to keep as many of the details as similar as possible for easy comparison. As you can see below, we are able to get 2 quotes: one from AmTrust and the other from Berkshire Hathaway Guard insurance company, a company mostly focused on providing workers compensation insurance.

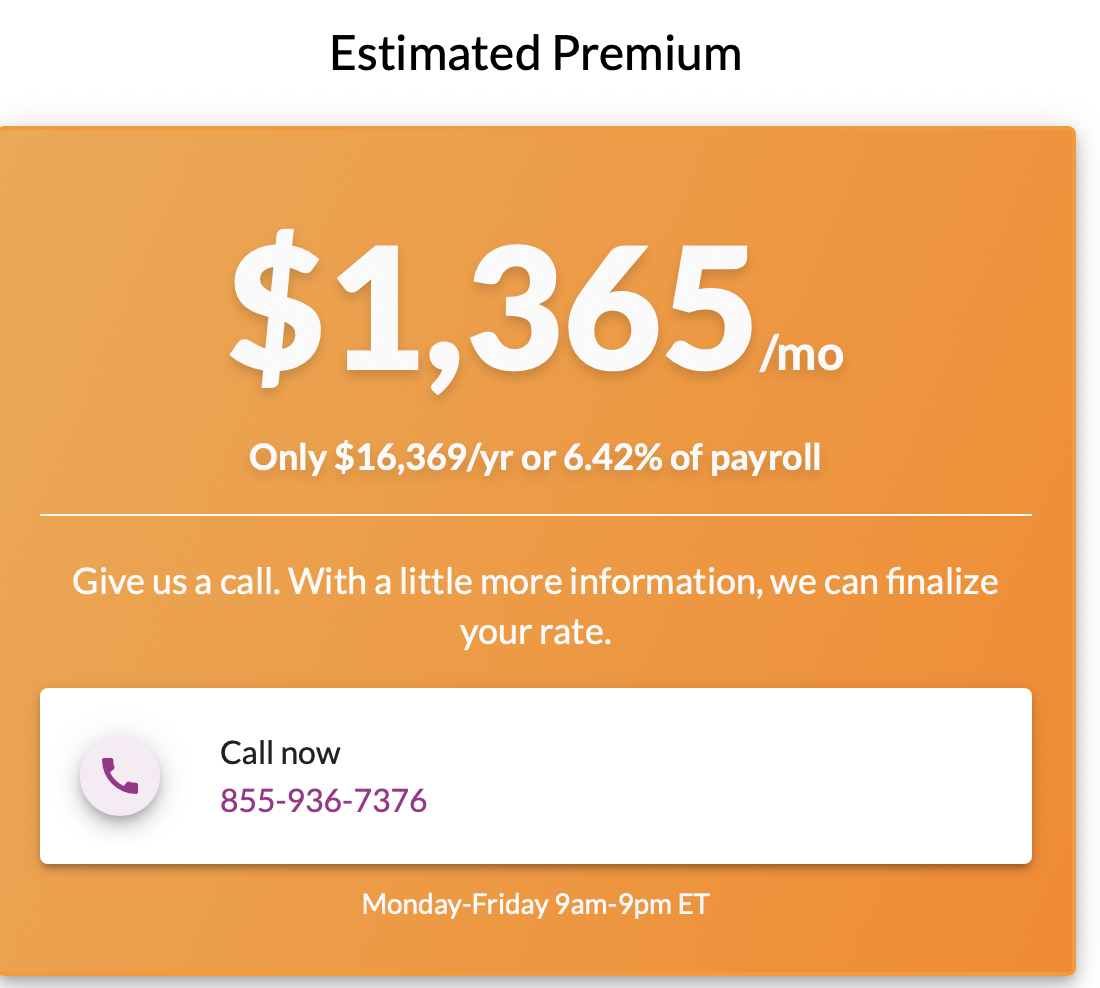

Pie Insurance: Best for Getting Online Quotes

Pie asserts that they can save you up to 30% on your workers compensation insurance. They cover most industries and have excellent reviews on Trustpilot.

The following quote is for a landscaping business in California with ten employees and $1 million in revenue.

Foresight Insurance: Best for Medium-Sized Businesses in High-Risk Industries

Foresight is a fairly new company that specializes in higher-risk industries. They also focus on mid-sized businesses as opposed to smaller ventures. In addition to workers compensation, they also offer builders risk, contractor’s equipment and inland marine as add-ons.

Foresight only insures eight states so far: California, Texas, Arizona, Arkansas, Oklahoma, Nevada, New Mexico and Louisiana. In addition, Foresight works through insurance brokers and does not offer online quoting.

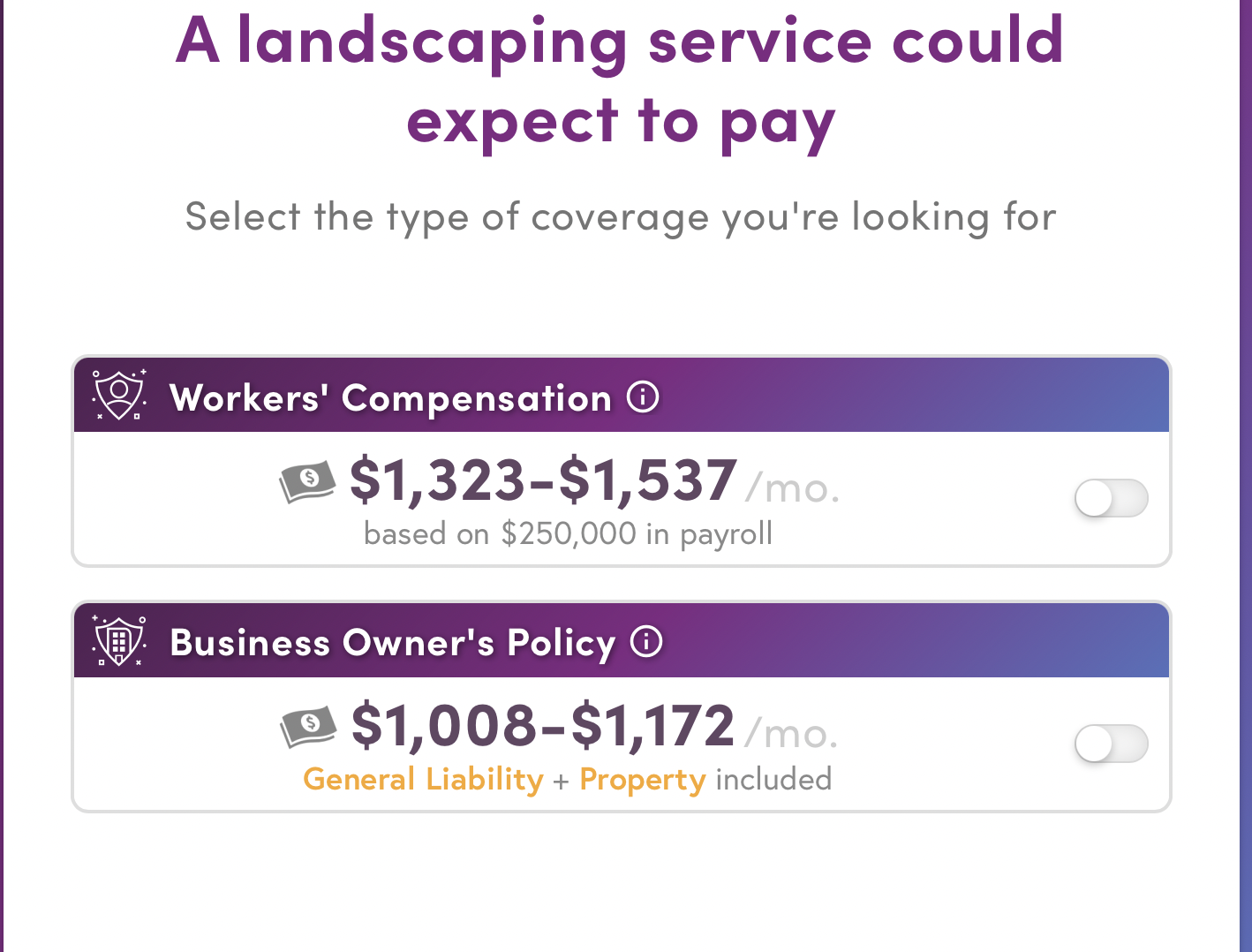

Huckleberry: Best for Getting Online Quotes of Workers Compensation and other Related Insurance

Huckleberry is a new company, starting in 2017, but it’s backed by Markel insurance, which has been around for decades. Huckleberry’s goal is to provide small businesses with the insurance they need in minutes. You can get a quote, select a policy and purchase it all online. As of right now, they’re available in 45 states, with plans to expand to the other five. The following is an estimate of what you could expect to pay with Huckleberry: to get an actual price, you would have to enter more details about your business, your employees, and what kind of work you do.

Geico Workers Compensation Insurance: Best for Getting Insured Fast

Geico partners with BiBerk, a Berkshire Hathaway company to provide workers compensation insurance. BiBerk also offers general liability insurance, commercial auto insurance, professional liability insurance, property and liability insurance, and umbrella insurance.

You can get almost instant coverage with BiBerk, and do the whole process online. They have good customer reviews and the process is very easy.

Travelers – Best with a Flexible Payment Plan

If you’re looking for experienced agents, Travelers is your best bet. They are the number one writer of workers compensation insurance in the United States. Travelers is committed to reducing claim costs, helping you make a safe work environment, getting injured workers appropriate care, improving claim outcomes, and/or helping employees return to work. Travelers has over 500,000 customers with Workers’ Comp insurance, and offers protection for many different industries.

For small businesses, Travelers offers Proprietary Risk Control Services – they have a trained team to help recognize and prevent accidents before they happen. They have more than 2,000 Workers’ Comp claim professionals to simplify the claims process, as well as

500+ in-house nurses and medical professionals to care for injured employees. Travelers also offers flexible payment plans, great for any small business.

>>MORE: What is Employers’ Liability Insurance? And Best Providers

Nationwide – Best with a Great Claims Center With a Robust Toolkit

Nationwide offers many options for purchasing Workers’ Comp insurance, like the ability to enhance a basic policy with additional commercial liability insurance, including general liability insurance and more. To get a Workers’ Comp quote, you’ll just need to enter some basic information about yourself and your business. You might have to call Nationwide between the hours of 7:30 AM and 9:30 PM EST in order to talk to an agent who will be able to help you with your quote.

Like Travelers, Nationwide has a dedicated claims center, along with a Workers’ compensation claims toolkit, including workers’ compensation rules, regulations, and required postings. These vary by state, so Nationwide’s toolkit has information to help your business stay up to date on Workers’ Comp laws. They also have a streamlined system for filing a claim, and will work one-on-one with small businesses to ensure you are receiving the correct coverage for the cheapest price.

>>MORE: How to Find Cheap Workers Compensation Insurance?

Liberty Mutual – Best with a Managed Care Pharmacy Program

Like Nationwide, Liberty Mutual offers a great toolkit for small business owners to help them make the right decisions when it comes to Workers’ Comp insurance. Policyholders can access Liberty Mutual’s pharmacy program online, where they can view instructions on how to find local medical providers. They also have easy access to state-specific workers compensation claims forms, posting notices, and websites. Liberty Mutual also has a dedicated hotline number for small businesses with questions or claims about their Workers’ Comp policies.

Liberty Mutual Insurance’s managed care pharmacy program gives injured workers access to medications and doctor care for their work-related injuries. Also, because laws vary from state to state, Liberty Mutual offers a list of state-specific Workers’ Compensation Resources, which can save you time and money.

On Liberty Mutual’s website, in addition to searching state by state, you can easily search to find Insurance agents near you who can help you purchase a workers’ comp policy for your small business.

>>MORE: What are Workers Compensation Insurance Requirements by States?

The Hartford – Best with Their Comprehensive Preferred Medical Provider Network

The Hartford offers two different ways to pay for your Workers’ Comp policy–Annual Payments, or Pay as You Go. Having options like this is great for small businesses who may encounter unforeseeable costs and problems when their business is growing.

In addition, The Hartford offers programs designed to support companies, promote employee safety and well-being, and return injured employees to work as soon as possible. If the injured employees cannot return for whatever reason, The Hartford can find them work training for new skills. Long-term benefits may also be included if the employee is permanently injured.

Workers’ Comp insurance from The Hartford includes a preferred medical provider network, where employees can view a nationwide network of over than one million medical providers who specialize in workplace injuries. They are also connected to 65,000 participating pharmacies throughout the US, along with a convenient mail order service. The Hartford offers experienced nurse case managers and easy-to-use Pay-as-You-Go Billing Solutions.

>>MORE: How Much does Workers’ Compensation Insurance Cost?

Next Insurance: Best for Small Businesses with a Fully Digital Experience

Next offers very affordable prices for small businesses, with Workers’ Comp coverage starting at just $14 a month for some companies. However, prices also vary widely from state to state due to the differing requirements of each state. To find out exactly how much workers’ compensation insurance will cost, you’ll have to get a quote that is tailored to your industry, location, and specific needs.

Next Insurance is completely online, and they offer a Live Certificate in lieu of paperwork. The Live Certificate is a digital alternative to paper/downloaded Certificates of Insurance. It’s an online proof of insurance which you can easily and instantly share with anyone by email or link.

Next Insurance is just starting to offer Workers’ Comp plans, so it may not be available in your area yet. You can easily check on their website if its offered in your state by entering your zip code.

- What is Workers Compensation Insurance and What does It Cover?

- Workers Compensation insurance Requirements by States

- California ; Florida ; Texas ; New York ; New Jersey ; Pennsylvania ; Illinois ; Massachusetts ; Ohio ; Colorado ; Georgia ; Maryland ; North Carolina ; Oregon ; Louisiana

- Workers Compensation Insurance for Independent Contractors

- How Much does Workers Compensation Insurance Cost?

- How to Find Cheap Workers Compensation Insurance?

- What is Self-Insured Workers Compensation?

- Additional Insured Workers Compensation Insurance

- Nanny Workers Compensation Insurance

- General Liability vs. Workers Compensation Insurance: How are They Different?

- Occupational Accident Insurance vs. Workers Compensation Insurance

- Employer Liability Insurance vs. Workers Compensation Insurance

What is Workers Compensation Insurance and What does It Cover?

Workers compensation insurance protects both the employer and the employee in case the employee becomes ill as a result of something on the job or injures themselves while at work. Without workers compensation insurance, the employer would be held liable for all medical bills and expenses for employees who got hurt while on the job.

In some states, workers comp includes employer’s liability insurance and protects employers from civil suits filed by employees, paying both for legal representation for your business and legal fees. It’s good for the employee, too, as it covers lost wages and even can cover the cost of re-training if the employee suffers a career-ending injury. Lastly, should the worst happen, and an employee dies while on the job, workers comp will cover burial expenses.

By accepting workers compensation benefits, employees agree not to file suit against an employer. However, sometimes they will reject said benefits and file a lawsuit anyway if they think they can win a bigger settlement. That usually happens if the employee believes their injury or illness was a result of gross negligence on the employers’ part. If this happens, workers compensation insurance will cover the employer’s legal defense (up to certain limits).

You can prevent most such lawsuits by providing a safe working environment. Don’t depend on workers compensation insurance for everything.

>>MORE: Workers Comp Insurance: Latest Changes Small Businesses Need to Know

Workers Compensation insurance Requirements by States

Almost every state requires workers compensation insurance. They do vary by how many employees you need to have before workers compensation is mandatory (although in many states, one employee is enough). They also vary in what penalties you’ll incur by not having workers compensation insurance.

Since state regulations change all the time, the best way to learn about your state’s workers compensation requirements would be to contact your states department of workers compensation. You can find a list of who to contact here.

Some states have some types of employees excluded from workers compensation coverage. These can include, but are not limited to:

- Domestic servants

- Babysitters

- Farm laborers

- Real estate brokers

- Contracted entertainers

- Non-commercial cleaning employees

- Independent contractors

- Inmates

- Volunteers

As an example, we can look at workers compensation requirement from three of the biggest states: California, Florida, Texas, and New York. For more state requirements, you can see What are Workers Compensation Insurance Requirements by States?

Workers Compensation Insurance in California: Requirements and Best Providers

California takes workers compensation very seriously. You need it if you have even one employee, and if you don’t, it’s considered a criminal offense. The state can mandate you stop all work until you acquire workers compensation insurance. Then if you violate the stop order, you can be fined $10,000. You can also serve a year in jail for violations.

Think that sounds bad? It gets worse. If an employee gets injured and files a workers compensation claim with the Workers’ Compensation Appeals board and the judge then finds out you don’t have any, you can be fined $10,000 per employee, or up to $100,000.

Get workers compensation insurance as soon as you hire your first employee. Here is the Top 6 Providers of Workers Compensation Insurance in California.

Workers Compensation Insurance in Florida: Requirements and Best Providers

In Florida, you can get away without workers compensation insurance if you have three employees or fewer. If you fail in that, you’ll be subject to a stop-work order until you obtain some insurance and pay the penalties. Penalties are twice what you would have paid for premiums in the first place.

It is advisable to obtain workers compensation insurance as soon as you could to protect your employees and your business. Here is the Top 6 Providers of Workers Compensation Insurance in Florida

Workers Compensation Insurance in Texas: Requirements and Best Providers

Texas is the only state that doesn’t require workers compensation insurance. It’s optional. Only businesses that contract with any government entity are required to carry workers compensation insurance. Let us stress that it’s still a good idea to have it. Texas has some of the cheapest rates in the country for workers comp, so there’s really no reason not to get it.

Here are our recommendations of the top 4 providers of workers compensation insurance companies in Texas.

Workers Compensation Insurance in New York: Requirements and Best Providers

It is a crime not to have workers compensation insurance in New York. In addition, you are required to post a notice on work premises that all workers, including independent contractors, are covered under workers compensation insurance policy. In some cases, independent contractors might be exempt from workers compensation insurance requirements. You need to consult with your insurance agent or broker to ensure you follow the regulations correctly.

Obtain workers compensation insurance for your business as soon as you hire the first employee. Here is the Top 6 Providers of Workers Compensation Insurance in New York

Workers Compensation Insurance in New Jersey: Requirements and Best Providers

Employers in New Jersey are required to provide workers compensation benefits to employees. This includes part-time or seasonal employees, and it applies to businesses that operate as LLC’s. You’ll have to pay fines of up to $5,000 for every 10-day period that you don’t have it and eventually can face criminal charges. The only exceptions are:

- Unpaid volunteers or interns

- Independent contractors

- Workers covered by federal programs

In 2020, New Jersey governor Murphy signed a law that said essential workers who contracted Covid-19 would qualify for workers compensation benefits.

Top three companies for workers compensation insurance in New Jersey. Learn more at the best workers comp insurance companies in New Jersey

- The Hartford

- New Jersey Manufacturers

- CoverWallet

Workers Compensation Insurance in Pennsylvania: Requirements and Best Providers

Workers compensation insurance is mandatory in Pennsylvania, even if you only employ your own family members. Part-time and full-time workers both need to be covered. You are also required to post information regarding who insures you somewhere where employees can see it. The only exceptions are:

- Federal workers (federal workers are insured by the federal government)

- Railroad workers

- Longshoreman

- Agricultural workers who work less than 30 days per year or earn less than $1,200 a year

- Domestic workers who don’t elect to come under the Workers Compensation Act

Rates are:

Payroll (per $100) x class code rate x experience modifier rate = premium

Obviously, workers in different industries will have different rates.

Top companies for workers compensation insurance in Pennsylvania.

- The Hartford

- Progressive

- Huckleberry

- And if you want to compare online quotes, consider CoverWallet

>>MORE: 5 Best Workers Compensation Insurance Companies in Pennsylvania

Workers Compensation Insurance in Illinois: Requirements and Best Providers

If you own a business in Illinois, you need workers compensation insurance. If you don’t, you can incur a fine of $10,000. Even if you have just one employee, even if they only work part-time, you need workers compensation insurance.

The only exceptions are:

- Sole proprietors

- Business partners

- LLC members

- Corporate officers

- Domestic workers who opt out

If you fall into one of these categories and choose not to get workers compensation insurance, you’ll need to fill out a workers compensation coverage opt-out form and file it with the state.

If you don’t have workers compensation insurance in Illinois, you could be fined $500 for every day you don’t have it.

Top workers compensation insurance companies in Illinois:

- Pie

- Travelers

- Zurich

- CoverWallet if you want to compare online quotes from several companies

Here are our recommendations of the top 4 providers of workers compensation insurance companies in Illinois.

Workers compensation insurance in Massachusetts: Requirements and Best Providers

You must have workers compensation insurance if you have even one part-time employee in Massachusetts. The only exception is domestic workers who work less than 16 hours a week.

If you hire independent contractors, you’ll still need to provide workers compensation insurance unless you can prove three things:

- They don’t work under your direct supervision

- They perform work outside the normal course of your business

- Document that they have their own business doing this type of work

If you fail to provide workers compensation insurance, Massachusetts can issue a Stop-work order so you can’t do anything until you get insurance. You also get fined $100 a day.

Top workers compensation companies in Massachusetts. Learn more at the best workers comp insurance companies in Massachusetts

- Nationwide

- Chubb

- Hiscox

- CoverWallet if you want to compare online quotes from several companies

Workers Compensation insurance in Ohio: Requirements and Best Providers

Ohio is a little different than most states when it comes to workers compensation insurance. It uses a monopolistic state fund to provide employers with workers compensation insurance. You must purchase your workers compensation insurance through this fund—not through private insurance companies.

Even if you have only one employee, you’re required to have workers compensation insurance. The only exceptions are domestic workers, babysitters, and gardeners who make less than $160 per quarter. Since a quarter is three months, if you and your spouse go out more than four times in any three-month period and pay your babysitter $40 each time, she/he now qualifies as an employee, and you should purchase insurance for him/her.

If you don’t have workers compensation insurance (or fail to pay the premiums) the penalties are as follows:

- If you fail to file a payroll report on time the fine is 1% of the premium due

- Failure to pay a premium is a $30 fee, along with 15% of the premium due

- Assessment liens for nonpayment

You can only purchase workers compensation insurance through the Ohio Bureau of Workers Compensation (BWC).

>>MORE: Workers Comp Insurance in Ohio: How It Works & How Much It Costs

Workers Compensation insurance in Colorado: Requirements and Best Providers

Colorado is a no-fault state when it comes to workers compensation insurance. This means that it doesn’t matter if your employer does something negligent, or the employee does something stupid and injures themselves: they’re both covered under Colorado law.

Colorado also has a state fund for workers compensation insurance, but unlike Ohio, you don’t have to obtain your insurance through them, but it’s an option. You can get insurance through private insurance companies, you can self-fund, or you can obtain coverage through a group plan.

The only exceptions for workers compensation insurance in Colorado include:

- Real estate agents

- Independent contractors

- Domestic workers

- Volunteers

- Repair workers earning less than $2,000 a year.

Top companies for workers compensation insurance in Colorado. Learn more at the best workers comp insurance companies in Colorado

- The Hartford

- Liberty Mutual

- Travelers

- Pinnacol, which is the state fund for workers compensation

- CoverWallet if you want to compare online quotes from several providers

Workers Compensation insurance in Georgia: Requirements and Best Providers

If you have three or more employees in Georgia, you need workers compensation insurance. Even if your employees are part-time, you still need workers compensation insurance, regardless of how much they earn.

If your business is incorporated, up to five corporate officers can waive coverage on themselves. However, they still count towards the three-employee requirement, even if they opt out.

Top workers compensation insurance companies in Georgia:

- Pie

- Hiscox

- The Hartford

- CoverWallet if you want to compare online quotes from several companies

>>MORE: 6 Best Workers Compensation Insurance Companies in Georgia

Workers Compensation insurance in Maryland: Requirements and Best Providers

Businesses with even one employee need workers compensation insurance in Maryland. Like Colorado, Maryland is a no-fault state when it comes to workers compensation insurance. It doesn’t matter if the accident stemmed from negligence or carelessness (unless the employee was doing something illegal), the employee is covered.

The only exceptions to this rule are

- agricultural employers who have less than three employees and pay them less than $15,000 in total payroll.

- Employers with a net worth of more than $10 million can get approved to self-insure

- Tractor-trailer owner-operators

If you don’t have workers compensation insurance in Maryland, you can be fined up to $10,000.

There is a state fund you can purchase workers compensation insurance from as well, but it’s not a requirement, it’s an option.

Top four companies for workers compensation insurance in Maryland. See more details at the best workers comp insurance companies in Maryland

- Chesapeake Employer’s Insurance Company (state fund)

- The Hartford

- biBerk

- CoverWallet if you want to compare online quotes from several companies

Workers Compensations insurance in North Carolina: Requirements and Best Providers

Businesses with more than two employees are required to have workers compensation insurance in the Tarheel state. They can be full-time or part-time. The only exceptions are:

- Railroad workers

- Federal employees

- Domestic employees

- Casual employees

- Commission-based sellers of agricultural products

If you fail to obtain workers compensation insurance, you can be fined $1 per employee per day for failure to get coverage. The minimum is $50 a day, the maximum is $100. If the state determines that a business owner willfully disregarded the need for workers compensation insurance (as opposed to forgetting it or not being aware it was required) it can be considered a felony.

Top three providers in North Carolina. Learn more at the best workers comp insurance companies in North Carolina

- AIG

- Biberk

- The Hartford

- CoverWallet if you want to compare online quotes from several companies

Workers Compensation Insurance in Oregon: Requirements and Best Providers

If you have any employees at all, whether they are full-time or part-time, you need workers compensation insurance in Oregon. The only exceptions are:

- Independent contractors

- Sole proprietors

- Corporate officers

- LLC’s

If you don’t have workers compensation insurance, you can pay fines that amount to twice what you would have paid in premiums ($1,000 minimum). If you drag your feet, you’ll pay an additional $250 a day in penalties until you show proof that you’ve gotten the insurance.

Employers in Oregon pay an average of $1.12 per $100 of payroll for workers compensation insurance, although it varies by industry.

Top providers of workers compensation insurance in Oregon. Learn more details in the best workers compensation insurance companies in Oregon

- SAIF (Oregon’s not-for-profit insurance company)

- AmTrust Financial

- The Hartford

- CoverWallet if you want to compare online quotes from several companies

Workers Compensation Insurance in Louisiana: Requirements and Best Providers

Most employers are required to carry workers compensation insurance in Louisiana, even if you have only one employee and they’re part-time. You’ll also need workers compensation insurance if you employ seasonal workers or minors. There are some exceptions:

- Real estate brokers

- Musicians and performers

- Employees of a private homeowner

- Employees of a private unincorporated farm

- Federal employees

- Corporate officers

- Members of airplane crews involved in dusting or spraying operations

The average cost for employers compensation in Louisiana is $1.50 per $100 of payroll.

If you don’t have workers compensation, you can be fined up to $250 per employee for the first violation and $500 per employee for every violation after that, up to $10,000.

Top three providers of workers compensation insurance.

- The Hartford

- Pie

- CoverWallet if you want to compare online quotes from several companies

Learn more at the best workers comp insurance companies in Louisiana.

Who is exempt from workers compensation insurance in Florida?

Most employers with four or more employees will need to carry workers compensation insurance in Florida. However, there are a few special requirements:

- Sole proprietors don’t need to have workers compensation insurance

- Construction businesses need to have workers compensation insurance for every employee, including contractors. They are also responsible for making sure every independent contractor they work with has workers compensation insurance. Construction businesses can exempt up to three corporate officers.

- Agricultural businesses with six or more employees or 12 seasonal employees must obtain workers compensation insurance.

Who is exempt from workers compensation insurance in Texas?

In Texas, workers compensation insurance is optional for the most part. However, some industries do require it:

- Public employers

- State universities

- Construction contractors for public employers

- Motorbus companies

- Propane and natural gas dealers

- Employers of inmates who are on furlough

Since it’s not required, workers compensation insurance in Texas has some of the lowest rates, average only $0.55 per $100 in payroll.

Who is exempt from workers compensation insurance in California?

Workers compensation insurance is required for almost everyone in California, even if you have just one employee. It’s possible to get an independent contractor waiver, but California considers almost everyone who works regularly for someone to be an employee.

Even if you a sole proprietor, in some circumstances you’ll still need workers compensation insurance in California, even if you only work for yourself. Generally, if you do work that California considers risky, such as roofing or removing hazardous waste, you’ll need workers compensation insurance.

Workers Compensation Insurance for Independent Contractors

If you’re an independent contractor, most states don’t require your employer to have workers compensation insurance for you. However, if you work under contract, most contracts will require you to have it. You can get workers compensation insurance yourself, which anyone hiring workers under a contract may require anyway. You can read more about workers compensation insurance for independent contractors here.

How Much does Workers Compensation Insurance Cost?

How much you pay for workers compensation insurance depends on many factors. Just a few of them include:

- State laws

- Business’ size

- Number of employees

- Your claims history

- Type of work (higher risk industries pay more for insurance)

There’s a formula to calculate workers compensation insurance:

Classification rate * experience modification rate * (payroll/100) = premium

You can read more about how much workers compensation insurance costs here.

Many companies also offer free quotes, so be sure to shop around and compare.

How to Find Cheap Workers Compensation Insurance?

The best way to find cheap workers compensation insurance is to shop around for quotes. Companies may vary quite a bit in what they can offer.

There are a few state funded programs you can look into as well, so you can use some government funding to help you purchase insurance. Some states are monopolistic, meaning they don’t have any private workers compensation insurance available at all and you’ll have to go through the state.

You can also ensure you provide a safe working environment. Some companies will do a risk management assessment, so you can limit the amount of risk employees are exposed to. You can read more about how to find cheap workers compensation insurance here.

What is Self-Insured Workers Compensation Insurance?

Usually, employers provide workers compensation insurance for their employees through their insurance provider. In self-insured workers compensation, the employer pays all of the out-of-pocket claim costs for employees and assumes all of the financial risk. You eliminate the insurance company entirely. If an employee suffers an injury, the employer pays all the costs. Keep in mind, not every state allows this kind of arrangement.

There are some benefits to a self-insured workers compensation plan:

- Saving money upfront (as opposed to contributing to an insurance company’s overhead)

- Businesses who self-insure have a vested interest in providing a safe workplace

- Better cash flow: no money tied up in premiums

The biggest disadvantage is: accidents happen. You’ll need to have the resources available to cover huge medical bills, not to mention lost wages and other expenses. It’s a risk. You will have to decide if the benefits outweigh the risk.

Additional Insured Workers Compensation Insurance

You can list an additional insured on a liability policy, which means you are offering coverage to a third party you do business with. But you can’t list additional insured on a workers compensation policy, because only people who are your direct employees are covered. You can’t extend coverage to third parties.

Nanny Workers Compensation Insurance

State requirements vary on the status of nannies: in general, if the nanny is a full-time employee, you’ll need to provide workers compensation insurance. Some people are under the (mistaken) belief that their homeowners insurance will cover accidents suffered by the nanny, but that’s not true. Homeowners insurance is designed to cover you if a plumber or a electrician gets injured in your home, but those people are not your regular employees like a nanny. The only exception to this is California, where homeowners insurance has workers compensation coverage built in.

Not only could your nanny get injured, but some states will also fine you for non-compliance.

>>MORE: Best Nanny Workers Comp Insurance Companies

General Liability vs. Workers Compensation Insurance: How are They Different?

Sometimes people get confused about the difference between general liability insurance and workers compensation insurance. General liability insurance covers you if a third party injures themselves at your place of business: a customer or a visitor. It does not cover employee injuries: that’s what workers compensation insurance is for. General liability also covers you if you damage someone’s property. You need both if you operate as a business owner if you have employees.

Occupational Accident Insurance vs. Workers Compensation Insurance

Workers compensation insurance protects your employees. Occupational accident insurance provides similar coverage for independent contractors. Occupational accident insurance also covers lost wages, medical expenses, and death benefits. It’s usually cheaper than workers comp insurance, about 50% of the cost.

One thing to be aware of is that occupational accident insurance does not cover any of your legal bills. If your independent contractor sues you, you’ll be on the hook for all legal defense costs and fees. Also, many states have very specific requirements as to who can be covered under occupational accident insurance as opposed to workers compensation insurance. The best thing to do is contact your state’s workers compensation department to seek for their advice on your specific situation.

Employer Liability Insurance vs. Workers Compensation Insurance

Employer’s liability insurance is a part of workers compensation insurance. If an employee feels their injury or illness arose because of your gross negligence, they will refuse the workers compensation insurance benefits and sue you. Employer’s liability is the part of workers compensation insurance that will pay for your legal defense costs.

Final Thoughts

Workers’ Compensation Insurance is important for you, your business, and your employees. This is the only business insurance that is required by state law, except Texas. As soon as you have the first employee, you should look into this insurance immediately. Several insurance companies offer this product for businesses, from large to small, each with their own strengths and weaknesses. We pick and recommend 7 insurance companies, each with their own strengths and unique product features. You should definitely shop around with a few companies to find the most suitable for your needs and the best price.