Anyone who has ever owned a home knows that there is a never-ending list of things to do and things that need maintenance or repair. A handyman could do all of these projects. A handyman is a jack-of-all-trades person whose jobs can include anything from drywall repair to painting a living room to building a deck. Anything that needs to be done that the homeowner lacks the time or the skills to complete on their own; that’s what a handyman does.

Since a handyman’s job always involves going into clients’ homes, getting a general liability insurance policy is an excellent idea. A general liability policy will protect you if you accidentally gouge the tile floor or knock over the expensive vase that dear Aunt Martha gave your client.

- 6 best general liability insurance companies for handymen

- What does handyman general liability insurance cover and why do you need it?

- Are handymen required to have general liability insurance?

- How much general liability insurance do handymen need?

- How much is the average cost of handyman general liability insurance?

- How to find cheap handyman general liability insurance?

What is handyman liability insurance?

Handyman liability insurance is a policy that covers handymen for any damages they may cause while working. This can include damage to property, personal injury, or even death. This type of insurance is important for anyone who does repair work or construction, as it can help protect them from any legal issues that may arise from their work.

Handyman liability insurance is a short form for general liability insurance for handymen. General liability insurance is the most popular policy protecting small businesses from liabilities they may have from their work and their operations.

What does handyman liability insurance cover?

As a handyman (or handyperson), you enter clients’ homes all the time. Have you ever accidentally damaged a client’s property? Maybe you scratched the wood floor, or perhaps you left some of your equipment out, and the homeowner tripped over it and broke an ankle. General liability insurance is for exactly those scenarios. If you had a business where people came to you, general liability would cover you if a client or a customer injures themselves on your property.

Lastly, general liability insurance covers advertising injury. This covers you for slander, libel, stolen ideas, and copyright infringement. If you pay someone to design a website for your business and your competitor starts using the exact same webpage with his name inserted instead of yours, general liability insurance will cover your legal costs.

General liability will not cover you for intentional damage, illegal acts, or injuries to yourself or your employees.

Are handymen required to have general liability insurance?

No, it is usually not required by law. However, there are exceptions. For example, if you are a handyman working in apartment complexes in Florida, you are legally required. to have general liability coverage. Even when it is not required by law, it’s a good idea anyway. Most lawsuits against small businesses, especially handymen, are actually related to general liability. More importantly, many of your clients, especially the large and important ones, are likely to require you to have it.

The only insurance policies handymen are required to have are workers compensation, if you have employees, and commercial auto insurance, if you use a vehicle for work. Since you’re a handyman and you use a vehicle to drive to different jobs, you will need a commercial auto policy of at least 10/20/10, which is $10,000 per person, $20,000 per accident, and $10,000 in property damage. Just like your personal auto policy, these limits do not cover damage to your own car or property—you’ll need collision and comprehensive insurance for that. Also, these limits are extremely low. You should strongly consider a policy with higher limits.

Different states have different minimum commercial auto insurance requirements. You need to check with your state regulation to get the right coverage.

Learn more at the best handyman insurance companies

How much liability insurance do handymen need?

Most handymen should consider a policy of $1 million dollars per occurrence/$2 million aggregate. That means up to a million dollars in coverage per incident, and up to $2 million a year.

How much is the average cost of handyman liability insurance?

The average cost of a $1 million general liability insurance policy for handymen is $65 per month, or $780 per year. Most handymen pay from $50 to $190 per month, which is a wide range.

The handyman’s general liability insurance cost depends on several factors such as the nature of handyman’s work, years of experience, location, policy details such as coverage limits and policy’s deductibles, etc.

This is just the average. Your rates will be different. Be sure to shop around with a few companies or work with a broker like InsurePro, Simply Business, or CoverWallet to compare several quotes to find the cheapest one for you.

Learn more at how much handyman insurance costs

How to find cheap handyman liability insurance quotes?

Handyman insurance is generally expensive. Below are a few tips to help you find cheap handyman general liability insurance.

Get and compare several quotes

Get quotes from a few companies and compare them to find the right coverage for you at a reasonable cost. Getting online quotes from NEXT is fast and easy. Working with a broker like CoverWallet, InsurePro, and Simply Business is a good way to get several quotes more easily and conveniently. These brokers work with several insurance companies and they can pull quotes from these companies to show you at once. That would make it easier for you to compare several quotes and select the cheapest one for your handyman business.

- NEXT: Best fast online quotes with reasonable rates

- InsurePro: Best for short-term coverage, even just for one day

- Simply Business: Best for comparing several quotes to find low-cost coverage

- CoverWallet: Best for comparing several quotes from top rated carriers

Partner with an experienced agent or broker

There are a lot of nuances in handyman insurance as you can see. Any small details in your handyman operations can have a big impact on the cost of insurance. However much you can learn on your own, it will not be comparable to an agent or broker who does this for a living and has worked with hundreds, if not thousands, of handymen. Partner with an agent or a broker that you could trust so that they can advise you on the right coverages that you should have. They could also help you get several quotes to compare as well if you decide to work with a broker.

Safety-first in your operations

Insurance is always more expensive if you have claims and insurance companies give you a bad assessment of safety practices and standards. Emphasizing safety practices with both your employees and your customers, and requiring all of your employees to complete safety training and implement safe practices at the workplace will help reduce the number of accidents and claims in the future. Doing those may also decrease your current premiums since insurance companies’ underwriting engines may take these factors into consideration.

Apply for discounts

If they’re not offered to you when getting a quote, ask about them, whether you’re buying online or through an agent. Insurance companies often offer several discount programs that you can take advantage of. Even if you may not eligible for one or many of these programs today, you can still make changes in your operations so that you can be qualified to get these discounts in the future.

Taking these steps will help ensure you’re not paying too much for your handyman coverage.

6 best general liability insurance companies for handymen

These are the companies we recommend for handyman general liability insurance:

- Simply Business: Best for comparing several quotes online

- CoverWallet: Best for finding cheap coverage from top insurance companies

- NEXT: Best for fast coverage and a great digital experience

- The Hartford: Best for comprehensive coverage

- Hiscox: Best for small businesses with 10 employees or less

- InsurePro: Best for short-term temporary coverage

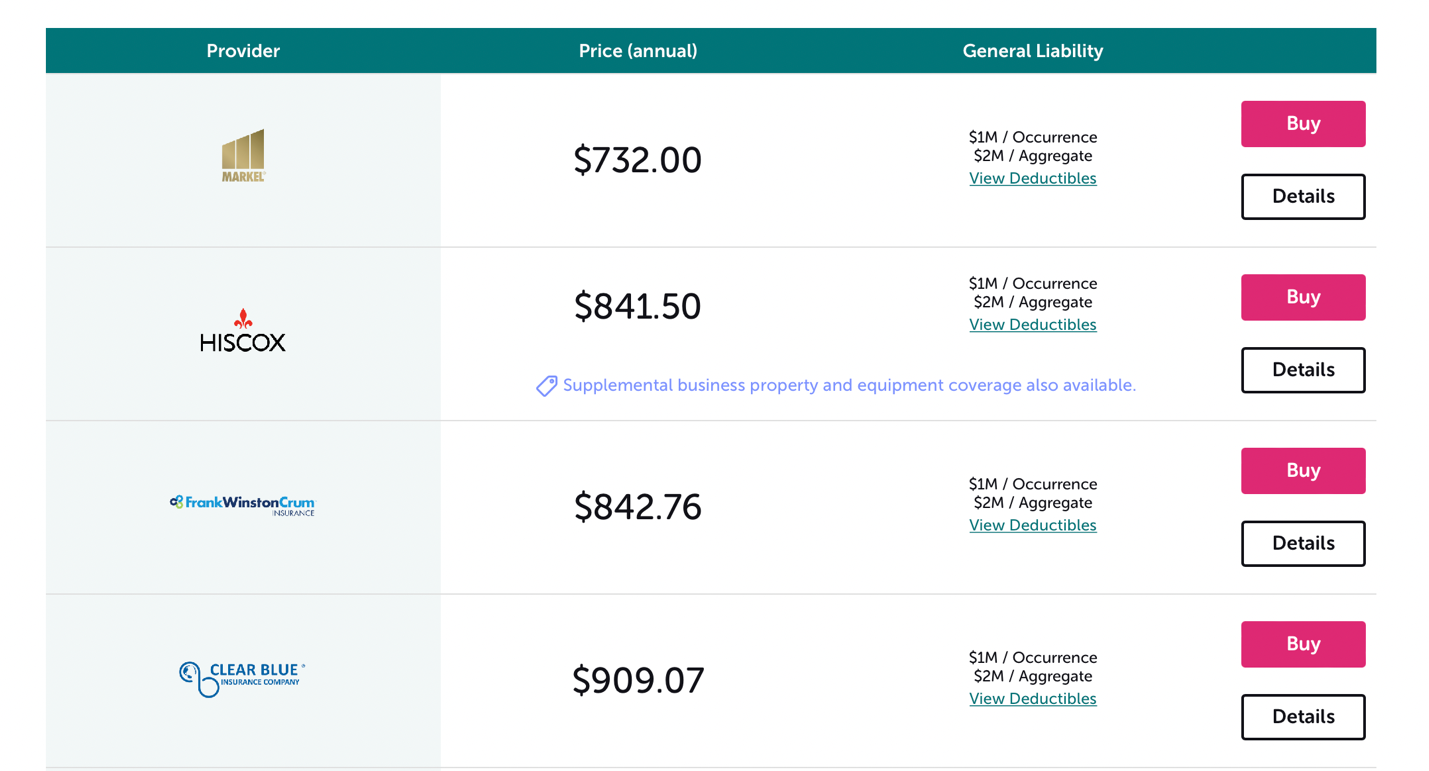

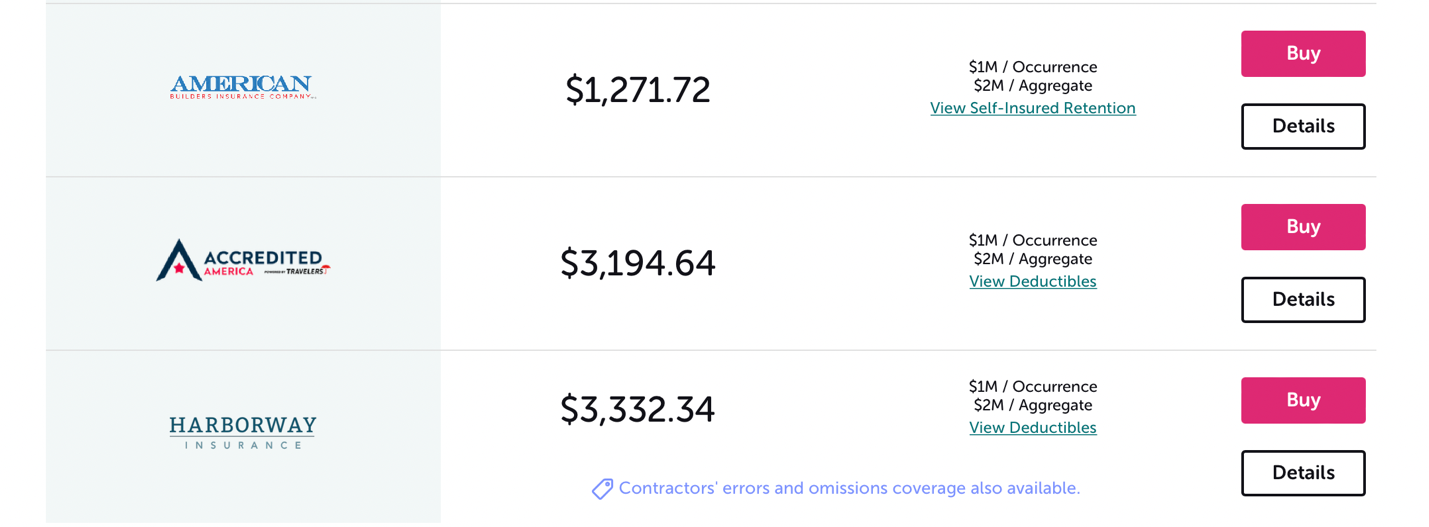

Simply Business: Best for comparing several quotes online

Simply Business is an online insurance broker, much like CoverWallet. Unlike CoverWallet, Simply Business can usually generate quotes in a matter of minutes and they pop up right on the website.

These are quotes for a handyperson in Jacksonville, FL, with $100,000 in revenue a year.

As you can see, they gave us seven quotes, and it took less than ten minutes.

Pros:

- Fast quotes

- Easy process

- Quotes show up right away

Cons

- General liability is the easiest form of insurance to quote; other types won’t get as many quotes

- Some types of insurance may not be available

CoverWallet: Best for finding cheap coverage from top insurance companies

CoverWallet is an excellent place to start your insurance search because they can give you up to four quotes when you fill out one form. CoverWallet partners with over 20 insurance companies like Chubb, Liberty Mutual, Hiscox, Progressive, and more. However, that means they only provide you with quotes from partner companies. As of late, instead of spitting out quotes on the webpage, they email them to you in a separate link. Quotes can still take a day or two to generate.

Pros:

- Multiple quotes

- Easy to fill out

- Manage all your policies in one place

Cons:

- Quotes must be emailed to you

- Can only provide quotes from partner companies

NEXT: Best for fast coverage and a great digital experience

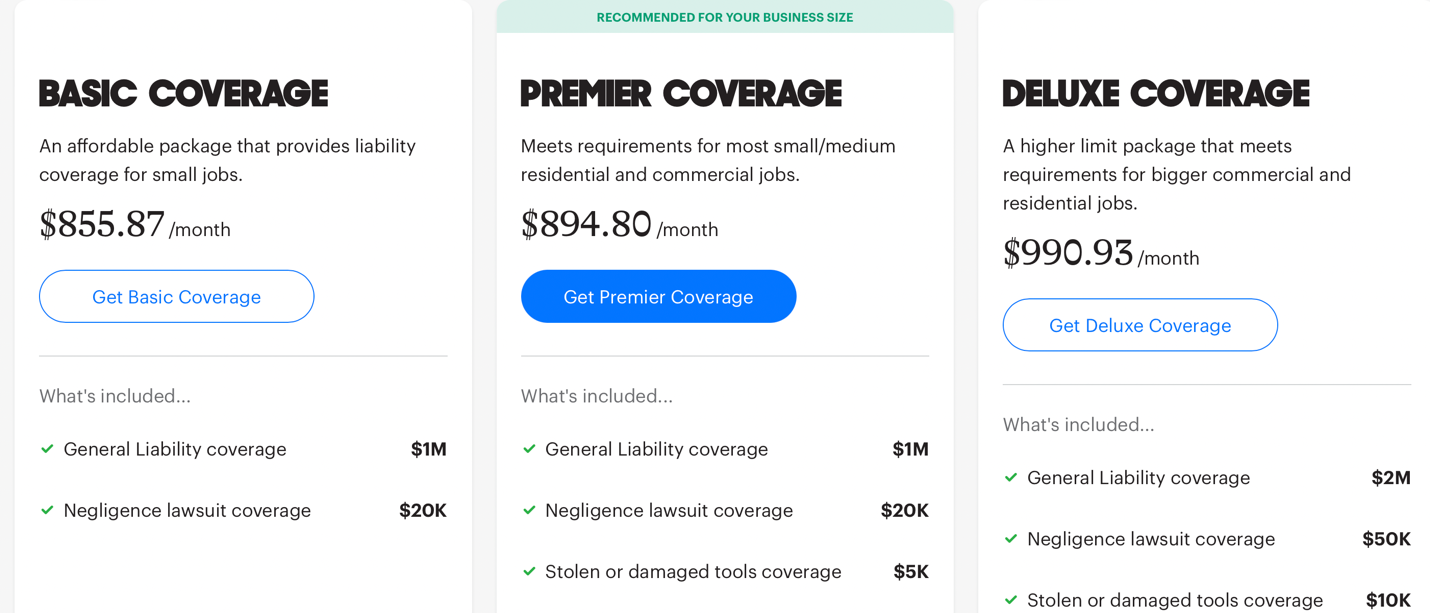

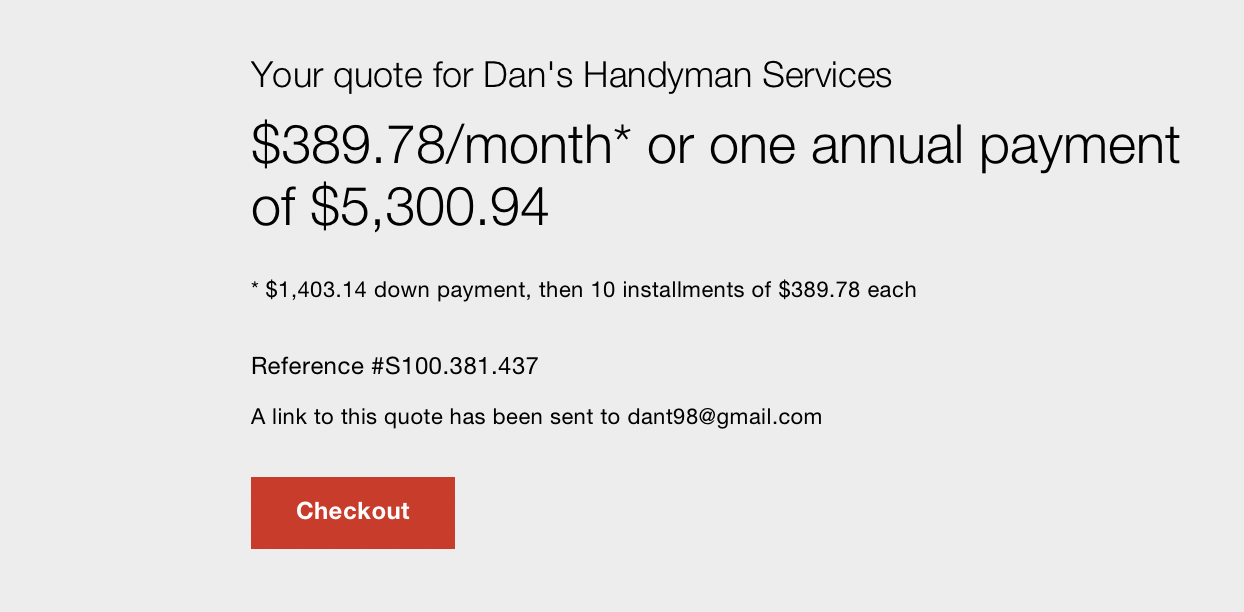

Next is an insurance company, not an online broker. That means they fulfill their own claims and service everything themselves. It’s pretty easy to get a quote, and you can buy a policy and be on your way in less than ten minutes. Next also offers a 10% discount when you buy multiple policies. When you give them your phone number, you consent to receive text messages from them.

This is the quote they gave us for our handyperson in Jacksonville, FL:

Pros:

- Easy online process

- Bundling discount

- Services their own policies

Cons:

- When you leave your phone number, you consent to receive text messages

- They may not have every policy you need/want

The Hartford: Best for comprehensive coverage

The Hartford offers flexible coverage for general liability insurance, and you can get up to $2 million per occurrence, $4 million aggregate. The Hartford also offers a lot of endorsement options, which could save you money. They can offer you a quote, but to buy the insurance you’ll have to contact an agent.

Pros:

- Flexible policies with higher limits than most

- Multiple endorsement options (internet-related advertising injury, data breaches, drones, etc.)

- Decades and decades of experience

Cons:

- You can’t necessarily get a quote; they might refer you to commercialinsurance.net

- To buy a policy you have to contact an agent

Hiscox: Best for small businesses with 10 employees or less

Hiscox has an easy application process and they can provide policies for businesses with fewer than 10 employees. You can get a quote online, and they have discounts if you buy more than one policy. You can add an endorsement for business equipment up to $25,000 on your general liability policy, which is handy if you have some valuable equipment but not enough to warrant commercial property insurance.

Pros:

- Easy online quotes

- Added endorsements

- Bundled discounts

Cons:

- Not all types of business insurance are available

- Some negative reviews on Consumer Affairs

InsurePro: Best for short-term temporary coverage

If your handyman business hasn’t taken off yet, or if you just do seasonal work, InsurePro is for you. InsurePro is an insurance broker, specializing in finding cheap temporary coverage for small businesses and contractors. You can get a general liability policy for as long—or as short—a time as you want, even if it’s just for an hour. If you want to add Business Equipment Protection, you can do that, too. Once your business starts to grow, you can add other policies as needed such as commercial auto and workers comp insurance.

Pros:

- Easy to get a quote—under a minute

- Offers policies for as long as you want them

- Easy to pause

Cons:

- InsurePro doesn’t underwrite general liability, other insurance companies do.

- InsurePro is a new company, doesn’t have a long track record yet.