If you take jobs fixing things up for neighbors or other people in your town, you might not always consider handyman insurance. After all, handyman jobs often feel like a casual side venture, not something you’d go out of your way to insure.

However, say you fixed a roof for someone, and despite your best work, the roof still leaked. That leak led to mold damage that cost the homeowner thousands of dollars to remedy. That homeowner could then hold you liable for the damages. So below we’ll look at what handyman insurance is, how much it costs, and where you can find it.

The 5 Best Providers of Handyman Insurance

To make it easy to find handyman insurance, we’ve listed some of the top options below.

- CoverWallet: Best for Comparing Online Quotes

- Next Insurance: Ease of digital quote process

- Progressive Commercial: Auto insurance

- Simply Business: Best for finding low-cost coverage

- InsurePro: Best for short-term coverage

CoverWallet: Best for Comparing Online Quotes

CoverWallet is a digital broker, specializing in small business insurance. They work with several leading business insurance companies. Once you provide your personal and business information, they will be able to provide you with several quotes of the companies that they work with such as Hiscox, Progressive, Liberty Mutual, Nationwide, just to name a few. Their quote form is relatively simple and straightforward. Within minutes, you will be able to compare several quotes in one place conveniently.

If you are new to buying handyman insurance, you can have a chat with their agents, who are very knowledgeable. They will be able to explain to you throughly so that you can make your informed decision.

Here is a quote sample we got from CoverWallet for a handyman general liability insurance policy.

Next Insurance: Best for Ease of Digital Quote Process

This company specializes in finding small business insurance with ease online. If you want a no-fuss process that’s 100 percent digital, check into this company. It has a page detailing handyman insurance.

When we selected to get a quote for handyman insurance, the system automatically recommended general liability insurance at $37.50 per month and commercial auto for $25 per month. This was for a Wisconsin location. You can save up to 10 percent when you bundle. The site was fast and responsive, showing rates on the second page.

Progressive Commercial: Best for Commercial Auto Insurance

This company sources its small business insurance from third party insurers. However, the company offers commercial auto insurance directly. Since auto insurance in a larger part of what a handyman often needs to insure, this is a good place to start for auto insurance rates. In order to get a quote, you have to enter in very detailed information about your vehicle.

Simply Business: Best for finding low-cost coverage

Simply Business is an online insurance broker, much like CoverWallet. However, unlike CoverWallet, Simply Business focuses on helping you find the cheapest coverage from their partners. They work with many carriers who are known to have good financial strength and offer low-cost coverage. If your main goal is to find low-cost coverage, you should definitely consider working with Simply Business.

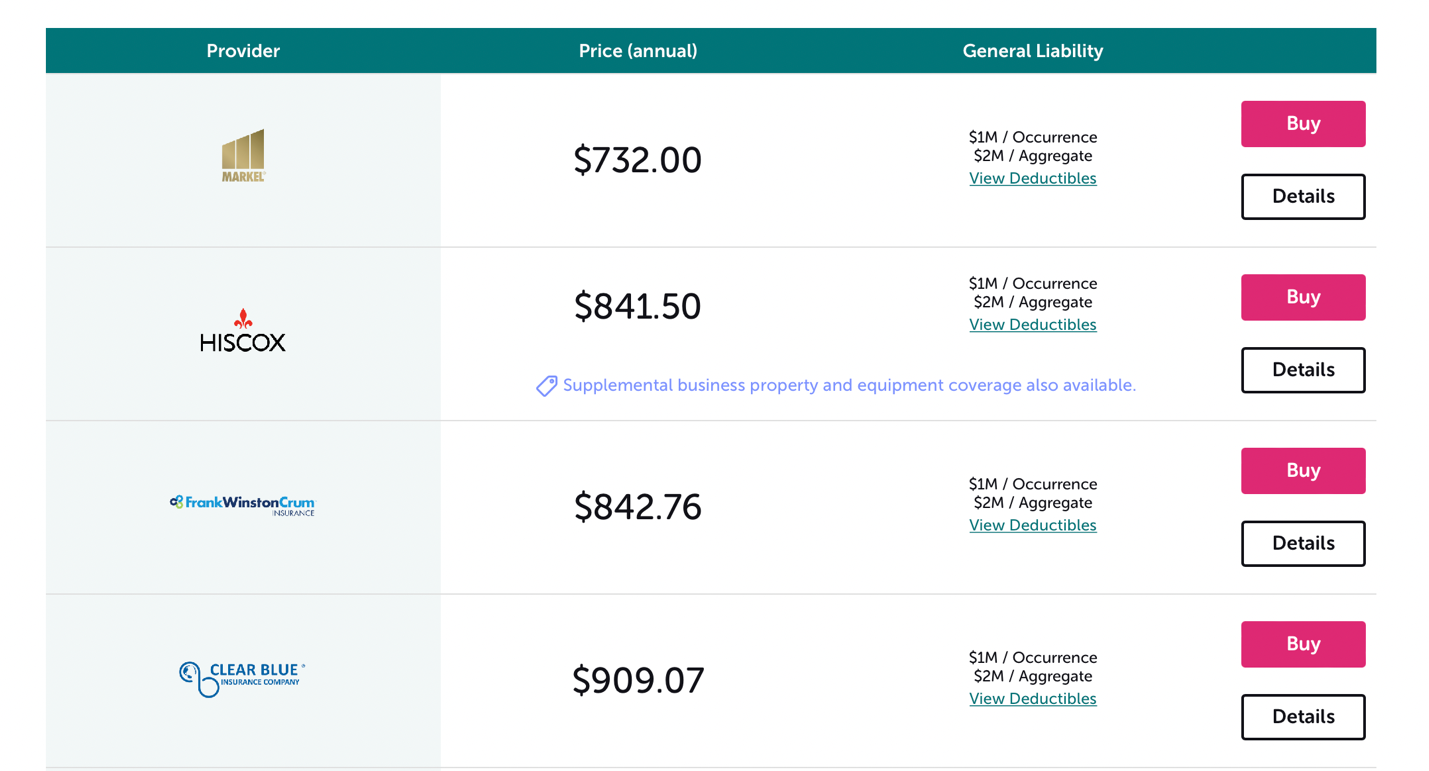

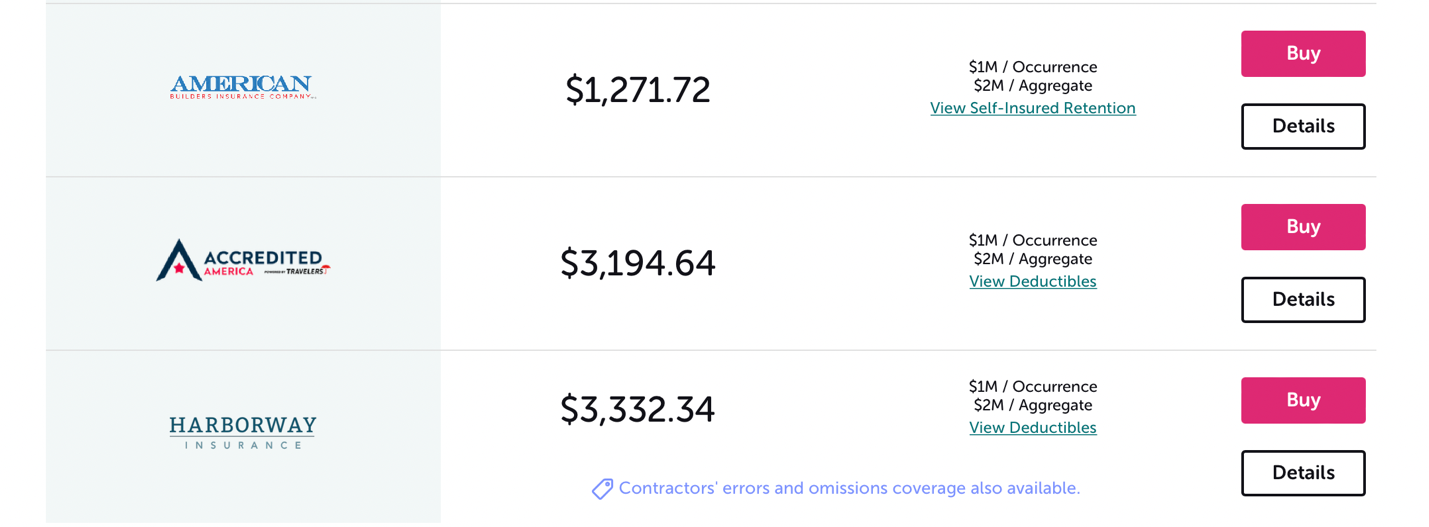

These are quotes for a handyperson in Jacksonville, FL, with $100,000 in revenue a year.

As you can see, they gave us seven quotes, and it took less than ten minutes.

Pros:

- Fast quotes

- Easy process

- Quotes show up right away

Cons

- General liability is the easiest form of insurance to quote; other types won’t get as many quotes

- Some types of insurance may not be available

InsurePro: Best for short-term temporary coverage

If your handyman business hasn’t taken off yet, or if you just do seasonal work, InsurePro is for you. InsurePro is an insurance broker, specializing in finding cheap temporary coverage for small businesses and contractors. You can get a general liability policy for as long—or as short—a time as you want, even if it’s just for an hour. If you want to add Business Equipment Protection, you can do that, too. Once your business starts to grow, you can add other policies as needed such as commercial auto and workers comp insurance.

Pros:

- Easy to get a quote—under a minute

- Offers policies for as long as you want them

- Easy to pause

Cons:

- InsurePro doesn’t underwrite general liability, other insurance companies do.

- InsurePro is a new company, doesn’t have a long track record yet.

What is Handyman Insurance?

Handyman insurance simply covers the types of insurance you should consider having as a professional handyman. If you work full-time as a handyman, it is always a good idea to have some insurance coverage to protect your and your business’s financial wellbeing. In many cases, your clients may request you to show insurance proof before they let you do the work in their house or property.

If you work part-time as a handyman and you have work quite often, almost every week, you should consider having some insurance coverage. However, if you just work as a handyman one day every month or even less, you might not need any insurance coverage.

>>MORE: Handyman insurance: What It Is, What It Covers, & Cost

What types of insurance does a handyman need?

Below are the types of handyman insurance you might want to consider include:

- General liability insurance

- Commercial property insurance

- Business Owners Policy or BOP

- Workers comp insurance

- Commercial Auto Insurance

- Contractor’s tools and equipment coverage

General liability insurance for handymen

This covers third-party claims for bodily injury, property damage, and advertising injury or harm to your reputation. If you get only one type of insurance, make it general liability insurance. General liability insurance will cover you if you are found legally liable for an accident that causes damages to someone else. For example, if your work causes damages to someone or breaks something valuable in your client’s house, this insurance will cover you.

Some states require some level of general liability insurance for handymen, so be sure to check your states regulations.

>>MORE: Best General Liability Insurance Companies

Commercial property insurance for handymen

If your handyman business is big enough that you operate it out of a physical location that you own or rent, and you store all of your handyman’s work equipment in that location, you will need commercial property insurance. This covers assets, building, equipment, and supplies you need to do your business.

If you run your handyman business out of your home, you might not need this. However, you might want to add an endorsement to your homeowners insurance policy to cover your home-based business.

>>MORE: Best Commercial Property Insurance Companies

Business owners policy (or BOP) for handymen

If the annual revenue from your handyman business is less than $1M or you employ less than 10 people, both full-time and part-time, you might want to get a BOP policy, instead of two separate policies of general liability and commercial property. BOP combines these two policies in a bundle to help you reduce cost and make it simpler to manage.

You can also add business income interruption coverage to your BOP as well. This can be useful especially if you are located in areas where extreme weather often makes you miss work and lose income.

>>MORE: Best BOP Insurance Companies

Workers compensation insurance for handymen

If you have employees, workers’ compensation insurance is a must since it is required by law. This will cover the costs of employees work-related injuries or illnesses. If you are a self-employed handyman or self-employed independent contractor, you still need workers comp insurance coverage to protect yourself when you get injured at work.

Handyman is a risky job. It is one of the professions with the highest accident probability at work. Make sure to get workers comp insurance coverage to protect yourself and your employees.

>>MORE: Best Workers Comp Insurance Companies for Independent Contractors

Commercial auto insurance for handymen

If you use a vehicle for work, including going from one work site to another, or driving a van full of tools and materials to your work sites, you will need a commercial auto insurance policy.

Your personal auto insurance policy doesn’t cover you if you drive your vehicle for work. The personal auto insurance company will refuse your claims. Even worse, they might drop you off altogether when they find out. Commercial auto insurance is usually a bit more expensive than personal auto policy. However, it is not worth it skipping it.

>>MORE: Best Commercial Auto Insurance Companies

Contractor’s tools and equipment coverage for handymen

If you have a lot of tools and equipment and they are expensive to replace, you may want to have contractor’s tools and equipment coverage. You can get this as a standalone policy or you can add it to your general liability insurance policy.

If you already have a commercial property insurance policy, your tools and equipment are protected when they are in your property. However, if they are damaged, lost, or stolen when they are in transit, this coverage will cover it. This is a type of inland marine insurance.

>>MORE: Contractor Insurance: 7 Policies, Costs, and Best 6 Providers

How Much Does Handyman Insurance Cost?

Costs for handyman insurance can vary. Some factors that affect costs include:

- If you need to insure employees and how many.

- The scale of your business, such as if you have multiple work vehicles on the road.

- Details of your business can affect rates, such as the size of a work building, how many years you have been in business and whether you operate in a more densely populated area. All of these are factors that many insurance companies consider to increase your risk and expense of a claim, which may affect premiums.

- Which types of insurance you choose to carry and the benefits you select for them, like limits and deductibles.

For an idea of ballpark rates, Insureon outlined some of the most common rates based on the types of insurance that a handyman tends to carry:

- General liability: $65 per month / $800 per year

- Worker’s compensation insurance: $315 per month / $3,790 per year

- Commercial auto: $150 per month / $1,825 per year

- Contractor’s tools and equipment insurance (inland marine): $15 per month / $170 per year

As you can see, insurance for a handyman can range from being quite affordable to something you’ll significantly have to budget for in your monthly earnings.

>>MORE: The Best General Liability Insurance for Contractors

Finding a Handyman Insurance Quote Through a Comparison Site

To get an idea of what handyman insurance quotes look like on a comparison site, we chose CoverWallet because of the ease of the process. We selected general liability for a 3-year-old handyman sole proprietorship business in Wisconsin with $45,000 in annual revenue. We got two quotes:

As you can see, the two rates vary significantly in monthly premiums by over $200 per month. This goes to show how important it is to shop around. This is especially true if you plan on carrying multiple insurance types, and you need the best rates to keep costs down.

Other digital brokers or agencies that offer quote comparison are Simply Business, Policy Sweet, Commercialinsurance.net, ez.insure, etc. Be sure to shop around to find your best quote.

Final Thoughts

- Handyman insurance simply means the types of insurance a handyman should consider carrying. These most commonly include general liability, commercial auto, business owners policy, worker’s compensation and contractor’s tools and equipment coverage (inland marine).

- Costs can vary significantly based on many different factors. The most direct factor is which types of insurance you choose to carry as a handyman.

- You can find handyman insurance both from companies that specialize in general small business insurance or companies that only work with contractors.

FAQs about Handyman Insurance

Does handyman need general liability insurance and how much does it cost?

Yes. If you choose only one handyman insurance policy, it must be general liability insurance policy. This policy will protect you if you or your work causes injuries to someone who is not your employee or damages to property which is not yours. It will pay for medical expenses, property damages, legal fees and judgments, and business equipment that is lost or stolen.

General liability insurance for handyman isn’t too expensive. On average, it only costs $60 a month or $720 a year.

In some states, you might be required to have general liability insurance to apply for a handyman license.

Why is handyman insurance so expensive?

By nature, handyman does a wide variety of work inside and outside of the house. They can include repairs, maintenance, fixture of anything in the house. Here is a list of work handyman is usually hired to do: painting the walls, drywall repair, remodeling, minor plumbing work, minor electrical work, furniture assembly. Sometimes they can also be hired to do roofing work, tree trimming work, wall work, etc. which are more complex and dangerous. This makes it really difficult for insurance companies to assess and measure the risks that handymen are exposed to. And it varies tremendously from one handyman to another.

To cover their risks sufficiently, insurance companies, if they offer handyman insurance, assume that the handymen will do all types of work mentioned above and more. As a result, it is very expensive to cover someone who does all of these work: plumbing, electrical, painting, roofing, etc.

Many insurance companies decide not to offer insurance coverage to handymen at all. Less companies operating in this segment also tends to push the price up.

How to get the cheapest handyman insurance?

To get the cheapest handyman insurance, you can try to get the cheapest general liability insurance for handyman. The best way to get the cheapest general liability insurance is to compare quotes of a few providers. The good news is that general liability insurance is the most common business insurance type, so is offered by almost all business insurance companies. You can also work with digital commercial insurance brokers like CoverWallet or Simply Business or Commercialinsurance.net to compare quotes more conveniently. They are able to provide quotes of several leading companies after you submit your information in one place.

Does homeowners insurance cover handyman?

If you are a homeowner and you hire a handyman to do some work in your own. The damages you may cause to your property might not be covered by your homeowners insurance. You homeowners insurance provides you with personal coverage and may not include contractor coverage. In order to be 100% certain, you need to check with your homeowner insurance provider to see if there is any coverage for contractors in your policy.

The best way to protect your property is to hire handyman who has a proper handyman insurance policy or a general liability insurance policy for handyman.

Where can I get handyman insurance for one-day?

If you are a part-time handyman and you just get a project for one-day, but the person who hires you requires you to have handyman insurance before he allows you to do the work in his home. In such case, you should get a general liability insurance policy for handyman with a coverage of just one day. Your best option is InsurePro. They provide general liability insurance or other types of business insurance for short periods as little as just a day.

Self-employed handyman insurance

Most handymen are self-employed. If you work full-time as a self-employed handyman, you need to protect your hard-earned business with insurance protection. The two policies that you should seriously consider are general liability insurance and workers comp insurance.

Learn more at the best-employed handyman insurance companies

General liability insurance for self-employed handyman

It is not required by laws in any state that a self-employed handyman must have general liability insurance. However, as a handyman, your work mostly takes place in your clients’ houses. As you do your work, you may cause damages to your clients’ properties and/or bodily injury to someone there. That is the reason why your client might require you have general liability insurance before signing the contract with you. If you can only afford one insurance coverage as a self-employed handyman, that should be general liability insurance. Learn more at the best handyman general liability insurance companies.

Workers comp insurance for self-employed handyman

As a self-employed, you are not required in any state to have workers comp insurance. Self-employed or sole proprietors are often exempt from workers comp insurance in any state. However, as a handyman, you know your line of work is quite risky. The chance of you getting injured at work as a handyman is a lot higher than many other professionals. Protecting yourself with a workers comp insurance policy for sole proprietors or self-employed is highly encouraged. It will help cover for everything that you may need if you get injured at work. Learn more at the best workers comp insurance for sole proprietors.

Handyman insurance in some key states in the country:

Handyman insurance in Florida

If you are a handyman in Florida and you want to get a license for a general contractor in Florida, you are required to have a general liability insurance policy of minimum $300,000 coverage for bodily injuries and $50,000 for property damages.

You should shop around with 3-5 providers to find the best general liability insurance quotes for you. Working with a digital broker like CoverWallet or commercialinsurance.net is a good option to compare several quotes in one place conveniently.

On average, a general liability insurance policy for handymen costs around $60 a month only.

>>MORE: Best Handyman Insurance Companies in Florida

Handyman insurance in New Jersey

In order for you to start working as handyman in New Jersey, you need to obtain a home improvement contractor license. To apply for this license, you need to have general liability insurance.

Most business insurance companies offer general liability insurance, so it should be easy to find one. Make sure you shop around to find the best price for the coverage you are looking for. All companies we recommend above sells general liability insurance nationwide. Working with a digital broker like CoverWallet is another option. It is convenient to be able to compare several quotes in one place. Learn more at the best handyman insurance companies in New Jersey.

Handyman insurance in California

If you want to work as a handyman in California, you need to get licensed. Without a license, you can only take projects worth up to $500, including labor and materials. Commercial auto insurance is required in California. Workers comp insurance is also required if you have one employee. General liability insurance isn’t required by California law. However, that’s the important policy every handyman should have since your clients may require it before signing the contract. Learn more at the best handyman insurance companies in California