Contractors face more — and more serious — on-the-job risks than people in almost any other industry. Whether you own an electrical, excavation, plumbing, HVAC, or any other type of contracting business, you know that accidents and other incidents can happen to you, and the people who work for you, any place, any time. Things can be fine one second, and the next, you’re dealing with a crisis.

General liability insurance covers common business risks faced by contractors such as injuries to clients, damage to client property, and advertising and marketing errors. It also protects your contracting business from the high costs associated with lawsuits. All contractors will need general liability insurance coverage. Most of your clients will require it before signing the contract with you.

Here’s everything you need to know about contractors general liability insurance, its cost, coverage, and how to get it.

- Contractors general liability insurance: The basics

- Who needs contractors general liability insurance?

- Are contractors required to carry general liability insurance?

- What does general liability insurance for contractors cover?

- What other coverages contractors usually get?

- Why contractors should get general liability insurance

- How much does general liability insurance for contractors cost?

- How to find cheap general liability insurance for contractors

- How to get general liability insurance for contractors

Contractors general liability insurance: The basics

General liability insurance for contracting businesses helps protect against claims of damage to other people’s property, bodily injury and other issues. This coverage is sometimes referred to as business liability insurance or commercial general liability insurance.

Contractors of all types need this coverage because accidents, injuries, and other types of incidents often happen during the normal process of conducting business because of the nature of the work they do.

Some examples of covered incidents include:

- An employee at a landscaping company drives a tractor through a client’s privet hedge causing thousands of dollars worth of damage.

- An electrician unintentionally causes a power surge while fixing wiring at a client’s home, damaging thousands of dollars worth of computers, televisions, and other electronic equipment.

- An employee breaks a client’s valuable vase while laying a new floor in their home.

- A worker forgets to post a sign after washing a floor at a workshop. A client slips, falls, and injures her hip while visiting the workshop to check on a project. This results in tens of thousands of dollars in medical and recovery costs.

In all these cases, general liability insurance would pay replacement, repair, medical, and legal costs resulting from the incident.

Learn more at the best general liability insurance companies and the cheapest general liability insurance companies.

Who needs contractors general liability insurance?

The following kinds of contractors should consider carrying general liability coverage. Click on the links to learn more about all the types of insurance coverage they need and the best ways to get it.

Carpenters

Carpenters face significant risks because of the dangerous tools they use, high probability of causing client property damage, and risks related to climbing ladders and working in challenging situations.

Cleaners

Cleaners, more than any other type of contractor, constantly work around valuable client property, making the risk for damage and breakage high.

Construction workers

Construction work is perhaps the riskiest of all contracting business types. The projects are typically the largest and most complex and the working conditions most difficult. Construction work can’t commence until proper general liability and other types of insurance have been secured.

Electricians

Electrical work is dangerous. Errors can result in fires and damage to costly client electronic equipment.

Excavators

Excavators are generally the first people working on construction sites. They face unique risks associated with using heavy equipment in rough conditions.

Handymen

The general liability needs of handymen can vary. Some do light projects that might not require a lot of coverage. However, many are more like contractors, requiring a significant amount of insurance protection.

HVAC contractors

Heating and air conditioning installers and repair people work on many types of equipment of different ages made by many manufacturers. The likelihood of on the job mistakes and errors is high for them.

Landscapers

Landscapers often work at great heights, near electrical and cable lines, using dangerous equipment. While landscapers that focus on flower gardens may face fewer risks and may need little coverage, arborists often need to secure a great deal of insurance protection.

Painters

Paint spills and splatters can cause a lot of damage to client property. If paint gets on a valuable carpet, piece of art or furniture, it can result in significant repair or restoration costs. General liability insurance can help pay all or a portion of the costs.

Plumbers

Plumbing work can result in floods and costly water damage to client property. General liability insurance can help cover some of the unique water-related and other risks faced by plumbers.

Roofers

Roofing is challenging work and can result in unintentional property damage. Customers typically require roofers to show proof of coverage before they allow work to begin.

People who do contracting work face significant risks of accidents and other issues that could cost them a lot should something unfortunate occur. Even if your business is a relatively small one, you should speak with an insurance agent or company representative to find out if you should get general liability coverage. It’s likely that they will recommend it.

Are contractors required to carry general liability insurance?

Unlike workers’ compensation insurance, general liability coverage isn’t required by states or other government entities. However, contractors are generally required by clients to have it before they’re allowed to work on their property. Landlords typically make businesses get it before they agree to rent property to them.

In any case, it’s a good idea for contractors to have it. In the situations outlined in the previous section, general liability insurance would likely cover the expenses related to the incidents. If the business owner didn’t have coverage, he or she would have to pay for the damages out of pocket.

What does general liability insurance for contractors cover?

General liability insurance helps pay for property and other types of damage that occur as a part of doing business. It also helps cover injuries that happen on your business property. Typically, general liability insurance can help cover claims related to:

- Third party property damage caused by you or an employee while conducting business

- Medical costs if your customer or client gets hurt when visiting your business

- Reputational harm resulting from malicious slander, libel, violating a person’s privacy, and more

- Advertising issues, such as copyright infringement and mistakes on your website.

What does general liability insurance not cover?

General liability insurance provides very specific types of coverage. It doesn’t cover all aspects of your contracting business or the risks it could face.

Here are some examples of things that are definitely not covered:

- Worker injuries: Your general liability insurance covers injuries to clients, customers, and passers-by that happen on your business property. However, it doesn’t cover employees injured while on the job. You’ll need workers’ compensation insurance for that. Learn more about the best workers comp insurance companies and the cheapest workers comp insurance companies.

- Bad professional advice: If you or someone who works for you provides a client or customer with incorrect or incomplete advice, general liability won’t cover it. You’ll need to buy professional liability insurance to be protected. Learn more at the best professional liability insurance companies.

- Vehicle damage: If a business-owned truck, van, car, or other vehicle is damaged in an accident while being used for work related purposes, your personal auto policy wouldn’t cover it. You’ll have to buy commercial auto insurance for that protection. Learn more about the best commercial auto insurance companies and how to find cheap commercial auto insurance.

- Crime or theft: If an employee commits a crime against your business or steals from it, general liability will not make your business whole. You will have to purchase employee dishonesty insurance.

- Data theft or loss: If your business data is lost, compromised, or stolen, your business general liability coverage won’t pay for related costs. Cyber security insurance covers those losses. Learn more about the best data breach insurance companies and the best cyber insurance companies.

- Business property damage: General liability covers third party property damage, but it doesn’t cover damage to your business property, including buildings, equipment, or merchandise. You’ll need commercial property coverage for this. Learn more at the best commercial property insurance companies.

What other coverages do contractors typically buy?

There are additional types of insurance many contractors purchase. These include:

- Contractors errors and omissions: This covers businesses for mistakes, errors, forgetting to convey information, misrepresentations, and more.

- Umbrella liability: This provides additional coverage over your policy’s limits. This is protection contractors who face costly risks should consider.

- Contractors equipment. This coverage protects valuable contracting tools and equipment from damage that happens to them on the job. Examples of things that are often insured include compressors, pumps, power saws, and landscaping equipment.

- Employee dishonesty: Workers are often tempted to take tools and equipment from job sites. This coverage will help you recover losses from employee theft.

- Equipment leased from others: This coverage protects equipment that your business rents or leases if it’s damaged or stolen, including things like forklifts, backhoes, lighting systems, and generators.

- Additional insured: This offers an added layer of protection if two or more businesses working on a job site are sued.

- Expanded property damage: Provides an additional level of coverage for property losses caused by contractors working on a job site. It’s particularly useful for contractors that do projects on expensive properties.

- Pollution coverage: Offers protection if a contractor is held liable for polluting water, air, or land. This includes legal defense, medical care, pollution mitigation, and more. Single instance and long-term pollution problems are typically covered.

- Waiver of subrogation. This endorsement prohibits an insurance carrier from recovering money they pay on a claim from a negligent third party.

These additional coverages can seem complex and confusing and in some cases they are. An insurance agent experienced in working with contracting businesses — or a rep from your insurance company — will be able to help you out with them.

Why contractors should get general liability insurance

The federal and state governments don’t require businesses to carry general liability insurance, although, as we’ve already covered, most clients and landlords will make you get it. However, it’s a good idea for small businesses to have it.

Think about it: If a visitor slipped and fell at your business and was injured, could you afford to pay their medical bills? Would you be able to pay to repair damage to a valuable painting if it’s caused by you or an employee while working at a client’s house?

The answer for most contracting businesses is NO and NO. That’s why general liability is one of the most popular business coverages for contractors, after workers’ comp and commercial vehicle insurance.

How much does general liability insurance for contractors cost?

The average cost of general liability insurance for contractors is $65 a month.

The price of general liability coverage can vary more than almost any other type of business insurance. It’s dependent on many factors, including type of contracting business, size of the operation, condition of business property and the specific risks faced by the business. The cost of this coverage can range from several hundred to many thousands of dollars a year. A small painting business will spend less on coverage than a landscaper with multiple locations.

The best way to ensure you’re paying a fair price for your general liability coverage is to get quotes from multiple providers. That way, you can compare coverages and costs to find the best combination for you. If you have any doubts, speak with an experienced insurance agent.

Learn more about the cost of general liability insurance for different contractor types.

How to find cheap general liability insurance for contractors

Here are some tips to help you find the coverage you need at a fair price:

- Shop around for the best value. Get quotes from a few companies and compare prices and coverages.

- Don’t stop shopping around. Make sure you get new quotes before you renew your policy.

- Take advantage of discounts. If they’re not offered to you when getting a quote, ask about them, whether you’re buying online or through an agent.

Taking these steps will help ensure you’re not paying too much for your general liability coverage.

Learn more at the cheapest general liability insurance companies for contractors .

How to get general liability insurance for contractors

There are three ways you can get contractor’s general liability insurance. Here’s an overview of each, examples, and the pros and cons of them.

Getting contractor general liability insurance from digital brokers and marketplaces

If you prefer to do things online, a digital broker or marketplace could be ideal for you. Examples include:

- CoverWallet: A leading online insurer that can get you a quote in minutes.

- Policy Sweet: A business insurance broker with a lot of experience working with small businesses across the country.

- Insureon: Fast online business insurer that allows you to chat online with a business insurance expert.

- NetQuote: Provides quotes from local agencies so you can compare coverages and prices.

Pros of digital brokers and marketplaces:

- Relatively low coverage costs because of limited infrastructure.

- Easy way to see multiple quotes at once.

- Fastest way to get coverage. Can often get a certificate of insurance in minutes.

Cons of digital brokers and marketplaces:

- Can sometimes be difficult to customize coverage.

- May need to complete a transaction over the phone.

- Not all insurers are represented on every marketplace.

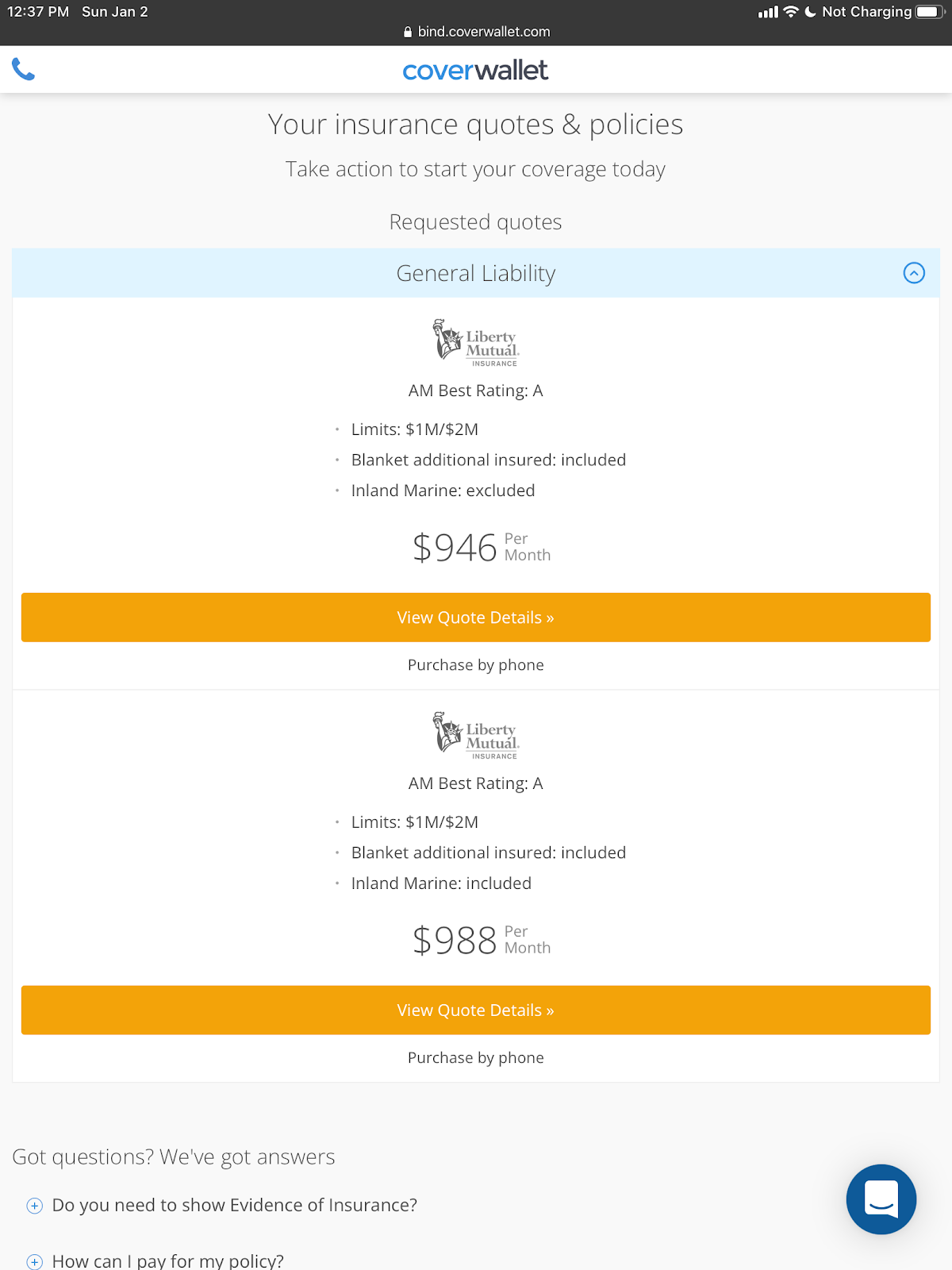

Here is a sample quote from CoverWallet.

Getting contractor general liability insurance from traditional insurers

If you have more complex business insurance needs, or don’t feel comfortable buying insurance online, it might make sense for you to get coverage from a traditional insurance company. Examples include:

- The Hartford: One of the oldest and most established business insurers in the United States.

- Travelers: Solid coverage from a leading business insurer you can purchase through an affiliated agent.

- Hiscox: A leading and respected multinational business insurer.

Pros of traditional insurers:

- Easy to get professional support when purchasing general liability and other contractors coverage.

- Generally committed to preventing work related risks.

- Relatively easy to customize coverages.

Cons of traditional insurers:

- More difficult to get multiple quotes and compare them than marketplaces and digital brokers.

- Typically more expensive to get coverage than from digital insurers.

- May take longer to get coverage than from online insurance companies.

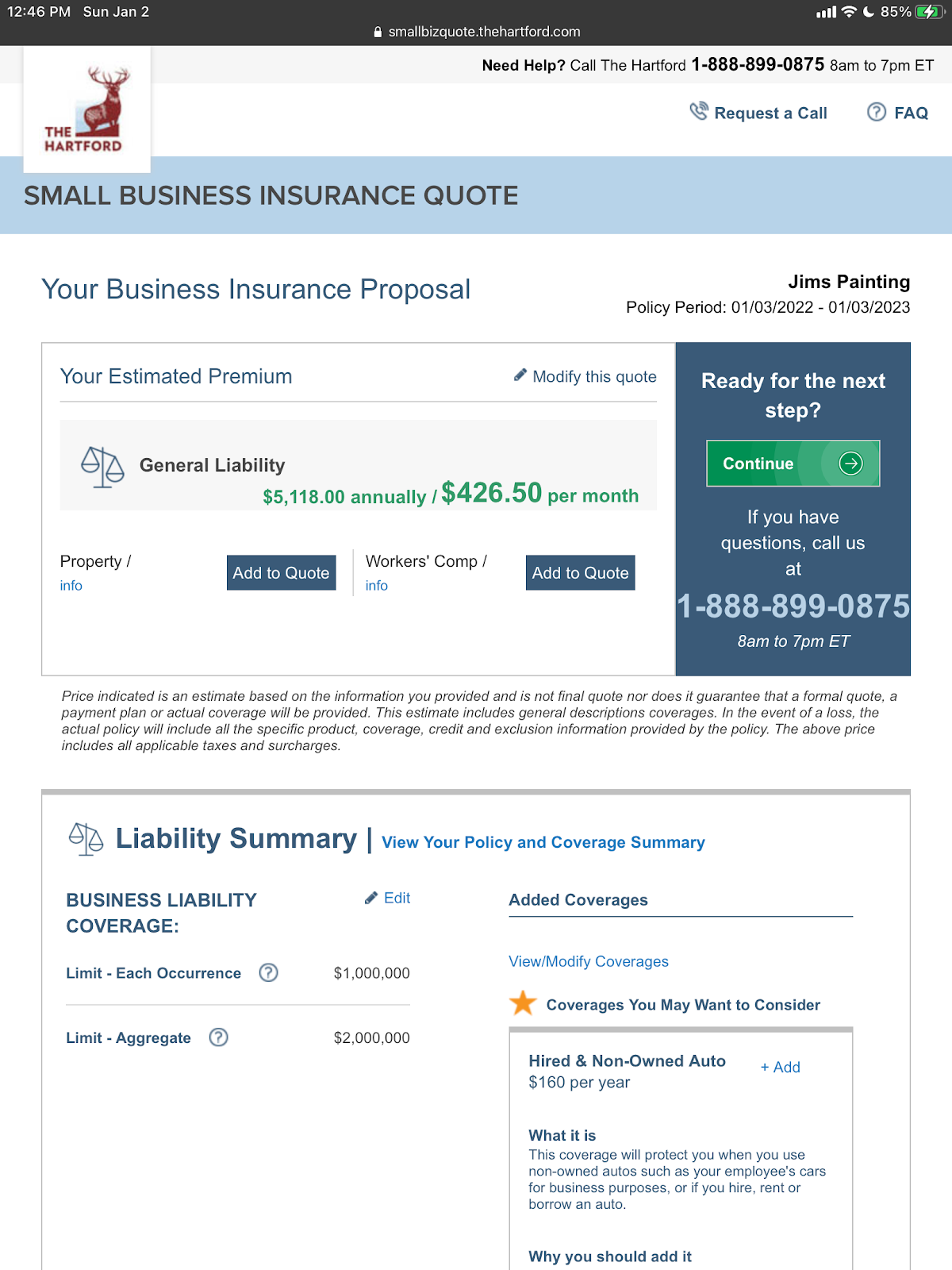

Here is a sample quote from The Hartford.

Getting contractor general liability insurance from insuretech startups

If you prefer working with cutting edge companies, an insuretech startup could be right for you. Some examples include:

- Next: An insuretech with solid ratings for financial soundness, backed by MunichRe, a leading insurer and reinsurer.

- Embroker: A company focused on using technology to lower insurance costs.

- Vouch: A tech based insurer focused on the needs of startups.

Pros of insuretech startups:

- Typically the lowest cost providers because of low overhead and dependence on technology.

- Usually offer the best online insurance buying experience because the technology backing up insuretechs is brand new.

- Can usually get insurance coverage in minutes, with no need to speak with a company representative.

Cons of insuretech startups:

- Small startup insurers may not provide 24 / 7 customer service.

- Coverages and customization options may not be as strong as more established insurers.

- Certain insuretechs may not be as financially sound as more established insurers.

Here is a sample quote from Next.