Like many online experiences, buying small business insurance on the internet can be extremely different, depending on the insurer, the types of insurance they offer, their value propositions, and their online experiences. This article with reveal the 8 best business insurance online companies, what they’re known for, and the pros and cons of each.

- CoverWallet: Best marketplace to compare several quotes and buy policies online

- Simply Business: Best broker to compare and find low-cost coverage and buy online

- InsurePro: Best company to buy on-demand and short-term coverage at the most affordable rates online

- Progressive: Best company to buy commercial auto and commercial truck insurance online

- Hiscox: Best company to buy professional liability insurance online

- biBERK: Best company to buy workers comp insurance online

- Thimble: Best company for gig workers to buy short-term coverage online

- Next: Best company for contractors to buy general liability insurance online

Can you get general liability insurance for an HVAC contractor at NEXT; get a quote from CoverWallet for an accounting firm; and a project-based quote from InsurePro for commercial auto and workers comp insurance for a cleaning

CoverWallet: Best marketplace to compare several quotes and buy policies online

CoverWallet is an insurance marketplace that provides small-business insurance quotes from a wide variety of reputable companies in a range of industries.

PROS:

- The service allows small business owners to get quotes and manage all of their business insurance policies in a single place online.

- CoverWallet has a simple and streamlined insurance application process.

- You can purchase one or multiple coverages in a single session.

CONS:

- It can take a little while to generate quotes, especially for multiple coverage types.

- Coverage can be more expensive to secure through a marketplace rather than buying directly from an insurer.

- It can be more challenging to customize coverage through CoverWallet than buying from a traditional insurance company.

Bottom line: CoverWallet is an online insurance marketplace that specializes in insurance for small businesses. If you want to compare coverages and costs from several insurers, CoverWallet could be an excellent solution for you.

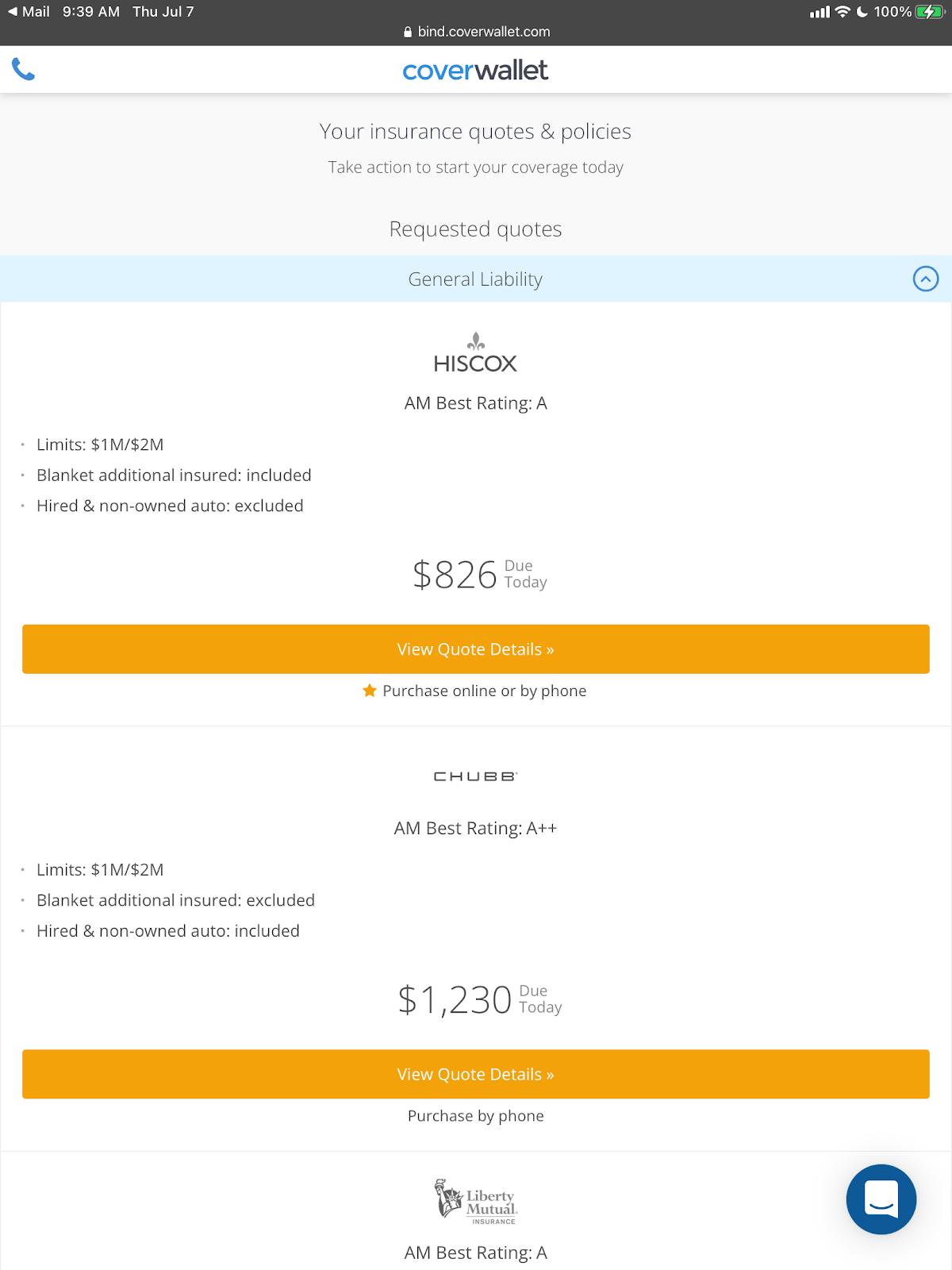

Here is a sample general liability insurance quote for a small accounting business from CoverWallet.

Simply Business: Best broker to compare and find low-cost coverage and buy online

Simply Business isn’t a direct insurance provider. Instead, it’s an insurance broker that connects small-business owners with business insurance through insurers on its approved roster.

PROS:

- Simply Business makes it easy to get quotes from multiple insurance companies through a single website.

- The company has a complete resource library to help you learn about coverage.

- Simply Business has a line-up of highly reputable insurance companies they’ve vetted on its platform.

CONS:

- Simply Business does the initial legwork to help you get quotes for the coverage you need. That’s where its services stop. Underwriting, claims, and customer service is handled by insurers recommended by Simply Business.

- Simply Business is based in the United Kingdom and owned by Travelers, a U.S.-based insurer. Simply Business offers a wide range of coverage in the U.K. However, the selection for U.S. businesses is more limited.

- You’ll have to make claims through your insurance provider, not Simply Business.

Bottom line: Simply Business will help you find the coverage you need at a fair price, all in one place.

InsurePro: Best company to buy on-demand short-term coverage online

Need general liability, commercial auto, and workers’ comp insurance fast? Only need coverage for a few days? Want to have the most affordable coverage? InsurePro could be an excellent solution for you.

PROS:

- Complete an online form, and InsurePro will get you quotes from three reputable insurers, including names like Hiscox, CAN, and Thimble.

- The entire application and insurance-buying experience usually takes less than 15 minutes end-to-end.

- Best for getting insurance coverage very quickly.

- Best place to find short-term coverage at the most affordable rates

CONS:

- InsurePro may not offer all coverages in all areas.

- You do not purchase coverage directly through InsurePro. Instead, you buy it from insurers recommended by InsurePro.

- You’ll have to make claims through the insurance company you get your policy from. This could be challenging and time-consuming.

Bottom line: InsurePro could be your best option if you need business insurance coverage fast.

Despite requesting a quote during company business hours, I was sent to this chat or and did not receive a quote.

Progressive: best company to buy commercial auto and commercial truck insurance online

Progressive is the largest provider of commercial vehicle coverage in the U. S. If you’re looking for business auto insurance, you should check out Progressive.

PROS:

- Progressive is a leading provider of commercial auto and truck insurance, with a long history of providing this coverage to businesses across the United States.

- Progressive commercial auto insurance covers a wide range of vehicles and uses, including dual personal and business use coverage.

- Progressive offers significant discounts when you bundle business and auto insurance.

CONS:

- Progressive provides commercial auto and truck coverage direct. It serves as an intermediary for other types of business insurance, which means you are getting it from other providers, not Progressive.

- You may be better off going directly to other insurers for non-vehicle insurance unless you plan to bundle other business insurance coverages with a Progressive car insurance policy.

- Except for commercial vehicle policies, you can’t file claims through Progressive. You have to do so through the insurer providing the coverage, which can be cumbersome.

Bottom line: Progressive could be your best option for commercial auto and truck insurance and other coverage if you bundle.

Hiscox: Best company to buy professional liability insurance online

Hiscox is a well-established business insurance company that sells basic coverage, such as general liability insurance, which can be packaged in a business owners policy. You can buy Hiscox policies online, from independent insurance agents, and through Geico.

PROS:

- Hiscox is an established small business insurer that is financially strong and stable.

- It’s possible to get a quote and purchase policies online through Hiscox.

- You may be able to get discounts if you purchase multiple business insurance coverages through Hiscox.

CONS:

- You may not be able to get all your business insurance coverage from Hiscox. For certain types of coverage, such as commercial vehicle and workers’ comp insurance, Hiscox will refer you to partner websites to get quotes from them. If you want to buy all your insurance policies from the same company, Hiscox may not be the best fit.

- Hiscox offers no coverage in Alaska and BOPs are unavailable in several states.

- Business owners policies are generally only available to businesses with a maximum of ten employees.

Bottom line: If you want to purchase professional liability insurance online through an established provider, Hiscox could be worth checking out.

biBERK: Best company to buy workers comp insurance online

biBERK is a subsidiary of Berkshire Hathaway, Geico’s parent company. Despite being a relatively newer player in the commercial insurance industry, biBERK has strong financial backing and a wealth of insurance knowledge and experience from the parent company.

biBERK specializes in developing and selling small business insurance online, bypassing the agents and brokers. As a result, they are able to cut costs and reduce prices for their customer benefits. They claim to save their customers 20% on premiums.

PROS:

- A completely digital experience from quoting, buying, and managing the policy online

- Great financial strength and industry experience from the parent company, Berkshire Hathaway

- Low cost coverage, save customers at least 20% premiums

- Their workers comp insurance available to a wide range of industries

CONS:

- Their policies, except workers comp insurance, may have lower coverage limits

Bottom line: If you want to have a low-cost workers comp insurance policy, getting it through biBERK could be a smart move.

Thimble: Best company for gig workers to buy short-term coverage online

Thimble is an online insurance provider that sells protection by the month, day, or hour to gig workers who need temporary coverage fast, typically to qualify to work on a project. Other insurers, not Thimble itself, underwrite policies purchased through its platform.

PROS:

- Thimble is an ideal option for freelancers, contractors, or businesses that need temporary or quick coverage.

- Monthly, daily, and hourly coverage is available.

- It’s also valuable for business owners who hire contractors; you can use Thimble to spell out insurance requirements for the people you’re hiring, and they can purchase it through Thimble.

CONS:

- Thimble doesn’t underwrite the policies it sells, so you’ll have to file claims with a different insurance company.

- Thimble customer support is only available online, not over the phone.

- Not a great option for people who need help and support purchasing insurance.

Bottom line: If you’re a gig worker who only needs insurance coverage every now and then to meet a client’s requirements, Thimble could be worth checking into.

Next: best company for contractors to buy general liability insurance online

Next Insurance is a business insurance provider that sells coverage online. It’s known for its general liability and other essential business coverages. You can purchase policies individually or in packages tailored to specific industries, like construction, health and fitness, and childcare. Next makes it easy to access and share certificates of insurance digitally and handle claims online or through its app.

PROS:

- Next is ideal for small-business owners who need coverage fast and want to manage their policies online.

- Next is a startup founded in 2016. But unlike similar insurance startups, Next handles its own claims and is independently rated by AM Best, a firm that ranks all types of insurers for their financial and business strength.

- Next has a fast and easy online application process. You can apply for — and get — general liability and other insurance in minutes.

CONS:

- If you need specialized coverage beyond general liability protection, Next may not be the right insurer for you.

- Traditional business owners who prefer paper insurance records may no like the digital buying and claims process offered by NEXT.

- You may find it challenging to get personal support during the buying process.

Bottom line: Next could be the right insurer if you need general liability protection and prefer to do business online.

Here is a sample general liability quote from Next for a small HVAC company.

Business insurance coverages

Small business owners need to get business insurance. The question is, what kind of insurance do you really need, and how much?

General liability insurance

General liability insurance covers you for:

- Third-party bodily injury

- Third party property damage

- Advertising injury

General liability insurance covers guests such as customers and vendors if they happen to injure themselves while on your property. It covers their medical bills and your legal costs if they should sue you.

Third-party property damage covers you if you or an employee damages a customer’s property. Anyone who goes to clients’ homes, such as plumbers, contractors, real estate agents need to protect themselves. One slip and you could accidentally damage that expensive coffee table your customer recently had shipped over from Greece.

Advertising injury means injuries committed by a business when it advertises its products or services. It included slander, libel, and copyright infringement. These injuries could be committed by you or your employees, or they could be committed by someone else and you are the injured party.

For example, if you own a clothing store and you use one of your customers in an ad, but you did not obtain his/her permission first, they could sue you for violating his/her privacy. This is considered an advertising injury.

Learn more at general liability insurance cost and the best general liability insurance companies

Commercial property insurance

Commercial property insurance protects your property and your equipment from losses. It covers losses due to:

- Theft

- Vandalism

- Weather

- Lightning strikes

- Fire

- Smoke

- Water damage

It should cover you for losses of business income, should one of the above factors damage your property. Oftentimes, landlords will require you to have commercial property insurance before they will rent or lease a space.

Learn more at commercial property insurance cost and the best commercial property insurance companies

Business Owners Policy (BOP)

A Business Owners Policy can save you money by combining several of the most common types of business coverage under one policy. It almost always combines general liability insurance and commercial property insurance. Usually, they also include at least one other type of coverage, depending on the policy. Some policies include:

- Business interruption insurance

- Cyber liability

- Crime

- Rented vehicles

- Equipment breakdown

- Employment practices liability insurance

Shop around for the policy that provides the types of coverage you need. Learn more at BOP insurance cost and the best BOP insurance companies

Professional liability insurance

If you provide services or advice in exchange for money, you probably need professional liability insurance. Sometimes this type of coverage is called malpractice insurance, especially when it refers to medical or legal professionals, and sometimes it’s called errors and omissions insurance, but it’s all the same thing.

PLI covers you if you make a mistake or neglect to do something that causes your customer financial harm. For example, you are a real estate agent and you show houses to a nice young couple. They find one they love and are very excited. Sadly, you missed the deadline to put in their offer and another family bought the house. They could sue you for this mistake.

Learn more at professional liability insurance cost and the best professional liability insurance companies

Workers comp insurance

Workers compensation coverage is required if you have even one employee, even if they are part-time, even if they are members of your own family. Only sole proprietors and LLCs do not have to cover themselves. Other exceptions are:

- Individuals having work done to their home

- Non-profits with no paid employees

- Corporate officers who own more than 25% of the business and have no other employees

Workers comp protects you, the employer, from having to pay medical costs and lost wages for injured employers who cannot work. It also protects the employees from having to pay for their own medical costs, and it helps by paying them for lost wages while they recover. Should the worst happen, workers comp will also pay death benefits to the family of the accident victim.

Workers comp is based on payroll. One way to save some money on workers compensation insurance is to by pay-as-you-go insurance, which is based on the exact amount of your payroll as opposed to sick employees, fired employees, or employees you haven’t gotten around to hiring yet.

Learn more at workers comp insurance cost and the best workers comp insurance companies

Commercial auto insurance

Commercial auto insurance covers you if you are in an accident while using your vehicle for work. Personal auto coverage will not cover you if you use your vehicle for work-related purposes (other than commuting back and forth to your job).

Different state laws require different minimum liability coverage. However, most states require to have at least 15/30/15, or $15,000 bodily injury liability, $30,000 per accident and $15,000 in property liability coverage. You also need $15,000 per person and $30,000 per accident for liability coverage in case you are hit by an uninsured or underinsured motorist.

If you want to cover damages to your own property and your own vehicle, you’ll need collision and comprehensive insurance.

Trucking companies need more insurance to comply with state and federal regulations.

These are the bare minimums. You would probably want more coverage, otherwise just one accident can easily bankrupt you.

Learn more at commercial auto insurance cost and the best commercial auto insurance companies

Cyber liability insurance

Most businesses these days store at least some customer information online. Cyber liability insurance will protect you in the event of a data breach, malware attack, or ransomware attack. If you store things like credit card information, financial information, or medical records, you need cyber liability insurance. The cost of cybercrime is predicted to $10.5 trillion dollars by 2025. In case you’ve forgotten, that’s only three years away.

Learn more at cyber liability insurance cost and the best cyber liability insurance companies

Business interruption insurance

If your business had to close due to an emergency, how would you pay your bills? Business interruption insurance provides protection against financial losses if your business needs to close temporarily due to a reason listed on the policy.

That last part is important. If your business interruption insurance does not cover pandemics, as many small business owners found out in 2020, then you will not be covered by business interruption insurance. Covered perils are usually things like:

- Fire

- Theft

- Wind

- Lightning

- Falling objects

If floods or earthquakes are common in your area, you’ll need to add those as an additional expense.

Learn more at business interruption insurance cost and the best business interruption insurance companies

Directors & Officers insurance (D&O)

Directors & Officers insurance is like E&O (errors & omissions, also known as professional liability insurance) but for officers and directors of a company. It protects them from personal losses in the event the company is sued for some decision they made. A D&O policy will pay for legal fees to defend the company against lawsuits, either civil lawsuits or criminal lawsuits (often these are filed simultaneously).

Learn more at D&O insurance cost and the best D&O insurance companies

Which business insurance coverage do I really need?

There are a lot of different types of business insurance available but not all of them are necessary. Most small businesses should get general liability insurance. If you use vehicles for business purposes, you’ll need commercial vehicle insurance. If you have employees, you need workers compensation insurance.

Is business insurance required?

The only two insurance coverages that are required in general are workers compensation and commercial vehicle insurance. Everything else is up to you, but like all insurance, you should weigh the risks of a lawsuit against the costs of insurance.

Who needs business insurance?

Most small businesses should get at least a general liability policy, workers comp (if you have employees), and commercial auto insurance (if you drive a vehicle for business purposes).

Below are the popular businesses that need business insurance:

How much does business insurance cost?

The average business pays about $42 a month for general liability insurance. If you have more policies, you’ll pay more. The best thing to do is get quotes from at least three different companies, so you won’t pay more than you have to.

| Business insurance coverages | Average costs |

| General liability insurance | $42 per month |

| Workers comp insurance | $93 per month |

| Commercial auto insurance | $86 per month |

| Professional liability | $57 per month |

| Cyber liability | $82 per month |

| Commercial property insurance | $102 per month |

These are just the averages. Your rates will be different. Be sure to shop around with a few companies or work with a top broker like Simply Business, InsurePro, or CoverWallet to compare several quotes to find the cheapest one for your business.

What factors affect business insurance costs?

There are a lot of things that affect how much business insurance costs. Just a few include:

- Location

- Number of employees

- Payroll

- Years of experience

- Industry (higher risk industries pay more)

- Claims history

- Coverage limits

It’s like buying auto insurance, in a way: insurance companies weigh the odds of how likely it is you’ll file a claim and then set your rates accordingly.

How to find cheap business insurance?

As mentioned above, the easiest way to save money on insurance is to shop around. There are so many factors that go into insurance rates, and some companies might weigh some factors more than others. For example, if you only have a year’s experience in your field, some companies might see that as more positive (no claims!) and others might see it as a negative (This kid has no idea what he’s doing and will make mistakes).

You can also bundle policies. Business Owners Policies (BOP) bundle several policies together, so you save money. Even if you only buy one type of business insurance, you can usually bundle it with your homeowners insurance or your auto insurance to get a discount.

Choose a higher deductible–make sure you have the funds to cover the deductible if you need to, but this can reduce your monthly payments.

Develop a safety plan. Stress the importance of working safer and smarter, not harder. Post the safety plan where everyone can see it.

How to buy business insurance online?

Figure out what business insurance you really need. Then, get some quotes.

Most companies will give you an online quote for at least general liability insurance. Take the time to gather quotes–it doesn’t take much time and it could save you hundreds of dollars.

You can save time by using an online insurance broker. They will present you with at least a few quotes and you’ll only have to fill out one form. Companies such as CoverWallet, Simply Business, and Commercialinsurance.net are good places to start.

Once you have your quotes, buy your policy. For many companies, you can do this online as well. Others require you to call to purchase insurance. Either way, it’s not that much time and it could save you money.